Market Resiliency Continued in September

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhile there's reason to be cautious in the near term as markets digest recent gains, the longer-term outlook is constructive.

Despite inflation remaining a concern, the Federal Reserve (Fed) cut interest rates in response to weakening jobs numbers. This allowed small-cap equity performance to lead a month that was generally positive across sectors, cap sizes and asset classes.

Small caps tend to be more reactive to short-term rate fluctuations, and the market is accounting for several rate cuts by the end of 2026, which might reflect exuberance beyond the Fed’s cautious approach and our view of two more rate cuts in 2025 and one in 2026.

The full effects of tariffs still loom. Front-loading tactics helped companies weather the uncertainty earlier in the year as they drew upon existing inventories and implemented mitigation measures, but those strategies can only delay the inevitable for so long. The long-term cost of tariffs may begin to show during Q3 earnings season.

“We’re cautious in the near term. Markets need to digest recent gains. However, our longer-term outlook is constructive,” says Raymond James Chief Investment Officer Larry Adam.

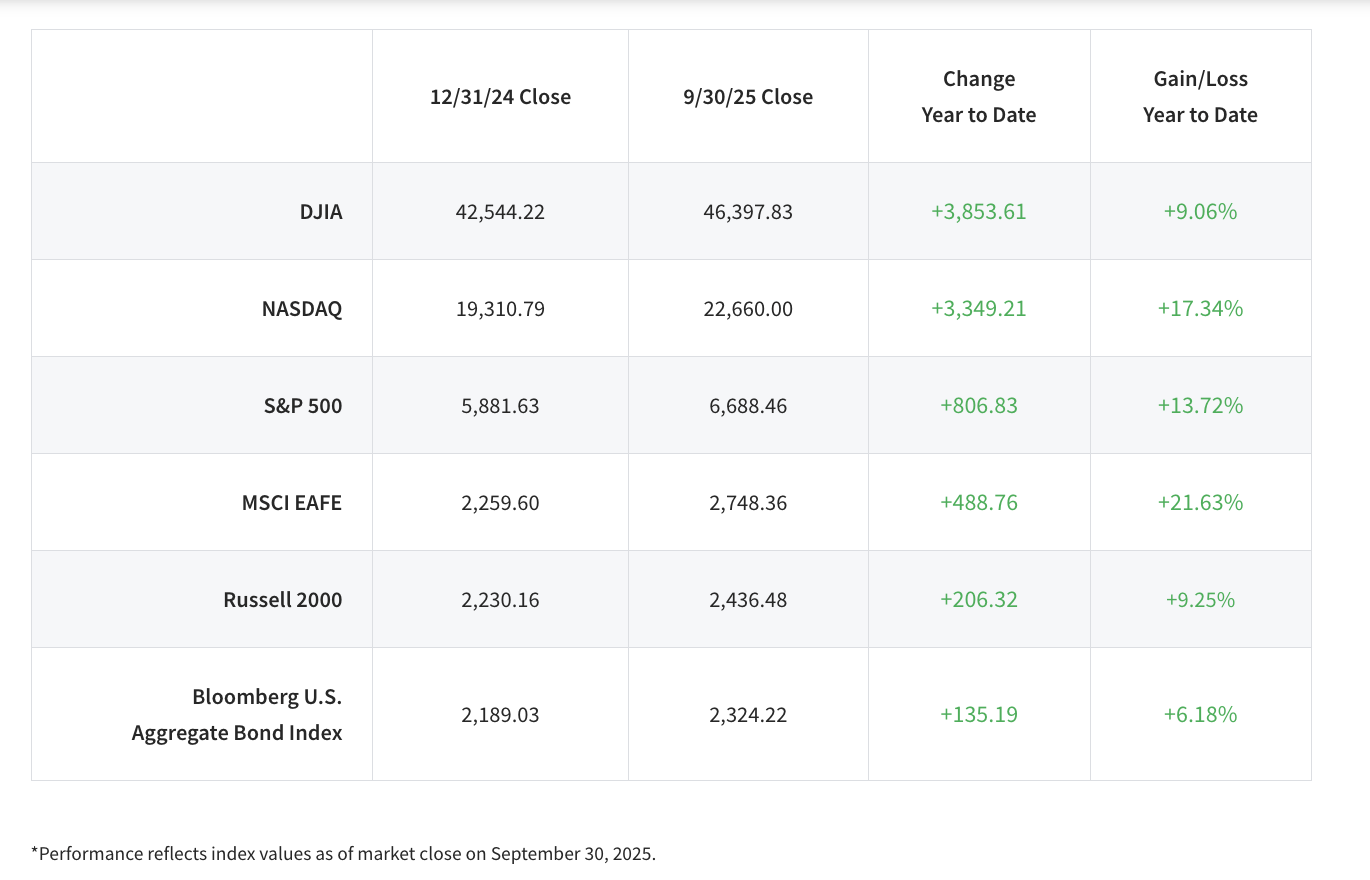

We’ll dive into the details shortly, but first: a look at the numbers year-to-date.

Jobs, manufacturing and construction took a hit

Throughout the month of August, manufacturing continued to contract with the exception of the New Orders Index. Private construction spending continued its downward trend, down 0.2% last month for a total of 4.6% this year. Job openings in July fell close to pre-pandemic levels, resulting in lower-than-expected employment overall, which followed downward revisions for another consecutive month in June.

Corporations absorbed tariff effects, but runway is dwindling

Throughout the past several months, corporations have relied on existing inventories and capitalized on tariff delays to mitigate price effects. But as those inventories dwindle, we may begin to see a sharp escalation in the effects tariffs will ultimately have. Until now, the markets have surged to record highs in spite of tariff headlines, partly because those effects weren’t reflected in actual earnings, but that could change in the coming months.

The Federal Reserve makes its new stance official

Equity markets, especially small-cap stocks, continued to climb following the Federal Open Market Committee’s decision to cut rates by 0.25%, marking the first official action of the Fed’s revised stance on the balancing of risks between fighting inflation and protecting jobs. We could see two more rate cuts of 0.25% each in October and December.

Gold hit another high, but overall mining is down

All-time record gold prices have persisted, with other precious metals like silver and platinum also seeing record values. However, prices for a broad range of industrial metals – including iron, nickel, lithium and silicon – are flat or down this year, amid sluggish demand from China. Mergers and acquisitions have emerged as one of the few pathways for mining companies to boost earnings.

International outlook

August saw a pickup of diplomacy surrounding the war in Ukraine, but major sticking points remain between the two sides. Most prominent is Russia’s insistence on territorial gains resulting from the war, which are extremely politically unpopular for Ukraine. Although a peace deal could open the door for international mining companies to begin operating in the region, progress is expected to be slow.

Multiple court cases pending with major economic implications

Last month, the US Court of Appeals delivered a landmark ruling against President Donald Trump’s use of the International Emergency Economic Powers Act (IEEPA), limiting his ability to unilaterally levy country-level tariffs. The Supreme Court is set to hear the case on November 5, with a ruling expected early next year. A second case involving the president’s firing of Fed Governor Lisa Cook, citing a threat to the independence of the Fed from overreach by the executive branch, will likely be heard by the Supreme Court as well.

The bottom line

With interest rates on the decline and more cuts expected on the horizon to combat labor stresses, potential for continued economic growth hangs on. The economy and consumer spending remains resilient despite uncertainty, leading to a positive outlook for equities over the next year.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Raymond James Chief Investment Officer and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. Diversification does not guarantee a profit nor protect against loss. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australasia and Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small-cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges, which would reduce an investor’s returns. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification. A credit rating of a security is not a recommendation to buy, sell or hold the security and may be subject to review, revision, suspension, reduction or withdrawal at any time by the assigning Rating Agency. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Income from municipal bonds is not subject to federal income taxation; however, it may be subject to state and local taxes and, for certain investors, to the alternative minimum tax. Income from taxable municipal bonds is subject to federal income taxation, and it may be subject to state and local taxes. Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. Investing in small-cap stocks generally involves greater risks, and therefore, may not be appropriate for every investor. The prices of small company stocks may be subject to more volatility than those of large company stocks.

Material created by Raymond James for use by its advisors.

J.D. Power 2025 U.S. Investor Satisfaction Study, which measures overall investor satisfaction with investment firms, was released 3/20/25, based on investors surveyed 1/24-12/24, who may be working with a financial advisor. Based on 7,876 responses from Advised Investors, 1 company out of 24 was chosen as the winner. The award is not representative of any one client’s experience, is not an endorsement, and is not indicative of an advisor’s future performance. The study is independently conducted, and the participating firms do not pay to participate. Use of study results in promotional materials is subject to a license fee. J.D. Power is not affiliated with Raymond James. For J.D. Power 2025 award information, visit jdpower.com/awards.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

© 2025 Raymond James Financial, Inc. All rights reserved.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition - March 2025 (PDF)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All