The European Union (EU) has a problem. For decades, member states enjoyed a tall glass of peace dividend lemonade under the shade of the U.S. security umbrella. Unfortunately, that era has ended. As a result, the EU’s defense spending is poised to rise, in our view, creating potential opportunities for investors—but not all opportunities are created equal. The challenge is to home in on companies that will be positioned to solve the region’s unique challenges.

A Changing Landscape

America insists that it can’t, or won’t, provide EU defense guarantees just as the Russian war machine threatens to make devastating progress against Ukraine. If Ukraine falls, the EU is likely to face a grim reality: Russia, with a fully mobilized combat force likely double that of the EU,1 would be in a position to forcibly reshape the politics of Europe to meet Putin’s vision. That vision is diametrically opposed to all that the EU stands for, but should Russia threaten war, the EU, without NATO allies, will have no credible response.

But problems like these require solutions, which bring change. In this case, the future of Europe hinges on the EU rapidly building up a defense deterrent to Russia. Most European leaders now believe militarization is the best way for the EU to continue its nearly one century of peace. As Antonio Costa, Portugal’s former prime minister and current president of the European Council, told Brussels “Peace without defense is an illusion.”

Problems bring change, and change brings opportunity for growth investors. The future of Europe hinges on the EU rapidly building up a defense deterrent.

We believe Europe’s private sector can play a critical role in the continent’s rearmament, and EU nations have already committed to rapidly increasing defense spending. However, we believe three major headwinds remain to the EU’s defense buildup.

First, militaries are understocked. Germany’s Parliamentary Commissioner for Armed Forces warned that Germany’s ammunition stocks would last only one to two days in the event of a conflict, and Poland, Bulgaria, and Romania are still partly reliant on Soviet-era weaponry. This is a consequence of the EU underspending on defense by $1 trillion since 2006, according to Goldman Sachs.2

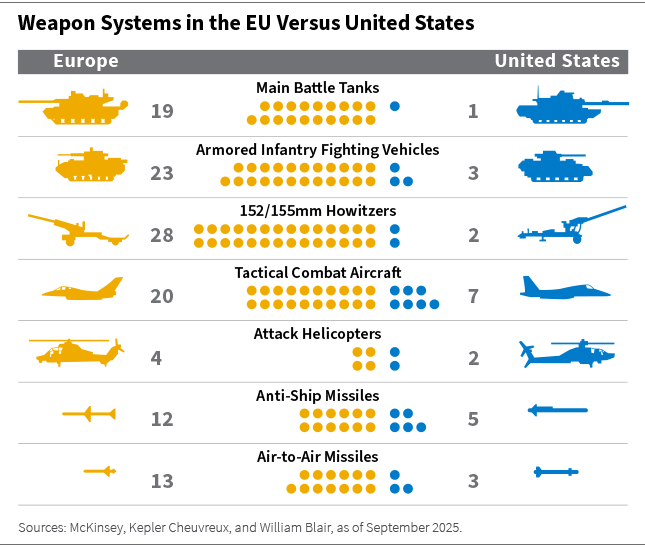

Second, there is a lack of interoperability. As in other situations, the bloc is stronger together, but being stronger together means forfeiting sovereignty. For example, America and Russia each have one tank family, but EU member countries operate 19 different tank models. That’s because tanks are bought with taxpayer dollars, and each country wants to maintain its own supply chain to keep jobs and profits local. However, 19 tanks with different operating and communication systems mean a unified battlefield force can quickly become a Tower of Babel. This approach also means research and development (R&D) spending is allocated to designing, for example, 19 different tank frames instead of spending more on accuracy systems or next-generation armor.

What’s true of tanks is similarly true of jets, air defense, ships and much other equipment. If the EU cannot centralize and standardize its defense equipment, it will likely be disadvantaged on the battlefield.

The third challenge to the EU’s defense buildup is innovation. Technology is changing warfare. As reported by the Atlantic Council, more than 70% of casualties in Ukraine have been inflicted by drones, a figure that would have been unfathomable a decade ago.3 Artificial intelligence (AI), robotics, space development, microelectronics, and other new technological frontiers are changing battlefields. Defense departments and ministries need to keep up.

Challenges Open the Door to Solutions

Change brings opportunities for growth, and by extension, for growth investors, and we think private-sector companies within our investment opportunity set are best-positioned to play a role in helping to solve the EU’s defense problems.

Governments do not generally manufacture weaponry. To restock, then, the EU will likely have to look to corporate partners, especially those with large economies of scale (for cost efficiency) and established credibility (given national security considerations).

The private sector has also financially engineered a solution to interoperability—joint ventures. Italy and Germany are good examples. Leading defense firms from each country have created a joint venture to locally produce defense vehicles. The vehicles will be built in Italy by an Italian entity, so taxpayer dollars will stay local, but they will use the same operating system as German vehicles, so will be interoperable. We have counted over 30 such joint ventures by EU defense companies since 2022, and more are announced each month. For example, two companies in Norway and France have formed a 50/50 joint venture in Norway to consolidate secure radio and encryption businesses. And three companies in the United Kingdom, Italy, and Japan have formed a joint venture to lead the next-generation fighter program, which received EU clearance in June 2025.

Both trends—scaled industrial producers and cross-border joint ventures—point to a broader theme in our coverage of emerging national defense champions. Historically, Europe has lacked large, broadly diversified defense companies, the so-called “primes” in the United States (meaning prime contractors). We believe that is changing. Governments increasingly need private-sector leaders to help marshal resources and coordinate with foreign entities. Here we look to identify those defense companies that are transforming from narrowly focused specialists into multi-faceted national champions.

That leaves innovation as the third challenge for EU defense for solve. NATO has identified a list of capability gaps that highlight vulnerabilities in its current fighting force. Among these gaps are drone and anti-drone systems, quantum-safe cryptography systems, autonomous fighting machines, improved satellite surveillance, and upgraded electronic systems. Here we think agile small-cap companies, or defense innovators, can play a part. We look for niche companies specialized in specific technological areas, such as drone software or communication equipment.

Our approach to investing in EU defense is therefore focused on identifying emerging national champions and small-cap defense innovators.

Policy Supportive

European defense departments and ministries acknowledge that to incentivize innovation and mobilize private sector resources, governments will have to allow companies to earn more, so we believe companies that can solve the EU’s defense problems will be rewarded for doing so.

In February 2024, Germany’s finance minister told Reuters that “[Defense companies] need private investments and financing. That’s why a second turning point is necessary that improves framework conditions for the industry.” (Framework conditions determine how much profit companies can make).4

Not all defense stocks will outperform, but for emerging national champions and defense innovators, we think the best is yet to come

Another example of supportive policy is lawmakers’ attitude toward consolidation. Emerging national champions are consolidating European defense through both the aforementioned joint ventures but also directly through mergers and acquisitions (M&A). At the European Council special meeting in March 2025, the German chancellor told reporters, “We need a major merger process in the European arms industry, and we also need the opportunity for these companies to work together actively, by themselves and without being hindered by European competition rules.”

A pan-European council concluding that the private sector needs less regulation, less competition, and wider profit margins? These are truly exceptional times. What all this means is that we expect, and are already seeing, significant and sustained earnings growth for European defense stocks.

Opportunities for Investors

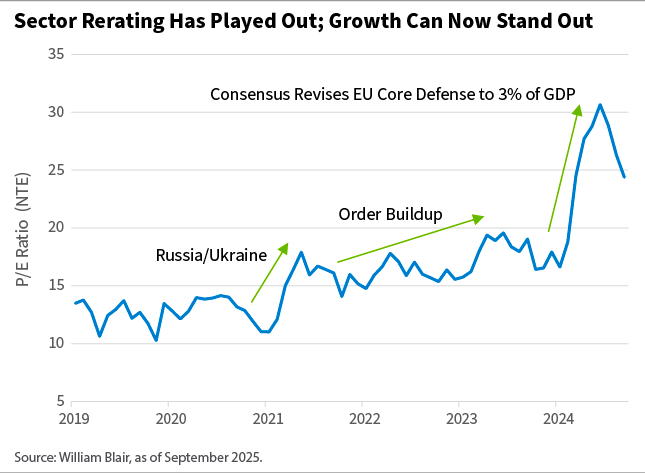

We don’t think this earnings power is fully priced into stocks. It’s true that Russia’s 2022 invasion of Ukraine was the catalyst for change, and defense stocks have performed well since then. We also concede that the sector-wide rerating has likely played out. The chart below shows that European defense stocks have rerated alongside defense budget growth. With North Atlantic Treaty Organization (NATO) members now committed to spending 5% of gross domestic product (GDP) on defense, there is limited fiscal headroom for more upside surprises.

Therefore, we are confident that not all defense stocks will outperform. Defense stocks that have rerated in anticipation of growing budgets may falter if the underlying earnings performance doesn’t come through. Yet for the companies we are focus on—emerging national champions and defense innovators—we think the best is yet to come. In our view, it is these companies that stand to capture the economics of increasing European defense spend.

Geography matters, too. Countries that are closer to Russia face a more imminent threat and have acted accordingly. The Nordics, Poland, and Germany have accelerated their defense programs much faster than their western neighbors. We are often surprised at conferences when U.S.-based investors seem to misunderstand the political will for defense in these countries. From our investment trips, we know the voting public in these countries see Russia as an existential threat and have afforded their governments what is effectively a wartime political mandate.

Will demand dry up for the companies in which we invest without an active war? We don’t think so.

Fiscal capacity is another important factor. Much of the EU simply does not have the funds to reach NATO spending targets. Spain, for example, has already requested an exemption. Spending risk is also much higher in France, where spending on defense would mostly likely be at the expense of public benefits. On the other hand, Poland’s spending on defense is already above 4% of GDP, and Germany’s coalition government has removed the debt brake, freeing up budget for defense.

Where could we be wrong? Execution, for one. The companies in which we invest have taken on significant orders, committing to delivering more defense products than ever before. That involves building new production plants, finding new suppliers, hiring new employees, and keeping to tight timelines. We pay close attention to these companies’ progress.

Another risk that is often flagged is that of a Russia-Ukraine ceasefire. Will demand dry up for the companies in which we invest without an active war? We don’t think so. As laid out in this piece, Europe is likely to re-arm regardless of the outcome in Ukraine.

From our perspective, Ukraine is less than 5% of the long-term earnings forecasts for the companies in which we invest (because we don’t need to believe in a never-ending war to invest in European defense; we see the investment opportunity more broadly, as NATO European defense).

Our base case is peace sustained through deterrence. If Russia believes the EU can defend itself, it will have no choice but to reduce aggression. Still, political situations can change rapidly, so we stay abreast of the latest developments.

The core of our investment case remains the initial point of this article: Europe has a problem. Problems bring change, and change brings opportunity for growth investors. Over the next five years, we believe select European defense stocks will be problem solvers, creating value for both their shareholders and EU stakeholders. The result, we hope, is a more peaceful and prosperous Europe.

Michael Patchen, CFA, is a research analyst on William Blair’s global equity team.

Want more insights on the economy and investment landscape? Subscribe to our blog.

1 Sources: Council on Foreign Relations for Russia (600,000 fully mobilized troops) and Gavekal (login required) for Ukraine (300,000 to 400,000 fully mobilized troops). Both militaries are roughly the same size in terms of active-duty personnel, but Russia has more fully mobilized combat troops. A fully mobilized troop is an armed force that has been fully assembled and prepared for active military service during a national emergency, a major conflict, or a declared war.

2 Source: Goldman Sachs.

3 Source: The Atlantic.

4 Source: Reuters.

A message from Advisor Perspectives and VettaFi: Looking for a way to gain exposure to the evolving digital asset landscape? Learn about CoinShares ETFs.

This content is for informational and educational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented.

Investing involves risks, including the possible loss of principal. Equity securities may decline in value due to both real and perceived general market, economic, and industry conditions. The securities of smaller companies may be more volatile and less liquid than securities of larger companies. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets and frontier markets. Different investment styles may shift in and out of favor depending on market conditions. Individual securities may not perform as expected or a strategy used by the Adviser may fail to produce its intended result.

Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit, and inflation risk. Rising interest rates generally cause bond prices to fall. High-yield, lower-rated, securities involve greater risk than higher-rated securities. Sovereign debt securities are subject to the risk that an entity may delay or refuse to pay interest or principal on its sovereign debt because of cash flow problems, insufficient foreign reserves, or political or other considerations. Derivatives may involve certain risks such as counterparty, liquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Diversification does not ensure against loss. The inclusion of Environmental, Social and Governance (ESG) factors beyond traditional financial information in the selection of securities could result in a strategy's performance deviating from other strategies or benchmarks, depending on whether such factors are in or out of favor. ESG analysis may rely on certain values based criteria to eliminate exposures found in similar strategies or benchmarks, which could result in performance deviating.

Collective Investment Trusts (CITs) are available to qualified retirement plans. For non-U.S. citizens or residents, William Blair offers a series of Luxembourg-domiciled SICAV products.

There can be no assurance that investment objectives will be met. Any investment or strategy mentioned herein may not be appropriate for every investor. References to specific companies are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future returns.

| | | |

Read more commentaries by William Blair