Parents are rarely prepared when their children have a growth spurt. Without warning, a child takes on new proportions, speaks with a new voice and expresses a whole new attitude. The transition is years in the making but feels like it happens in an instant.

The blossoming of stablecoins has caught us similarly off guard. Through 2024, they were obscure instruments used primarily to convert fiat currency into crypto assets. This past spring, following the election of a U.S. administration that promised to be “crypto-friendly,” we defined and offered thoughts on the future of stablecoins. Now, a regulatory framework for these vehicles is in place, and interest is growing rapidly.

In July, Congress approved the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act. The Act created a legal definition of payment stablecoins: digital assets on a blockchain used to settle payments. They are not bank deposits, nor are they government-backed currencies, securities or credit obligations. Stablecoin issuers will be nonbanks or bank subsidiaries permitted by their federal or state regulators. Issuers must hold safe, liquid collateral like cash, U.S. Treasury bills and repurchase agreements on a 1:1 value with their issued coins. To keep these payment vehicles distinct from banking products, stablecoins are not permitted to pay interest on balances.

Financial regulations have a reputation for being costly and onerous, but in this case, regulation will be beneficial. Cryptocurrencies have been the “Wild West” of finance, often the object of fraud and speculation. Legal boundaries will build institutional trust and promote greater adoption.

Passage of the GENIUS Act was only the first regulatory step. Now, agencies like the Treasury Department and prudential regulators like the Federal Reserve and the Office of the Comptroller of the Currency will start work on putting the GENIUS Act into force. Designing controls will be a challenging effort. The instant settlement of transactions will complicate fraud mitigation. The decentralized nature of these networks does not align with know-your-customer and anti-money laundering (KYC/AML) requirements of all financial institutions. The Act gives these agencies 18 months to enact the law; GENIUS-compliant stablecoins may then launch in 2027.

Issuers will be required to publicly share monthly summaries of their collateral positions, and larger issuers must post annual audited financial statements. This transparency is meant to simplify regulation and maintain trust.

An issuer cannot disburse interest to coin holders, but the issuer must carry interest-bearing assets as collateral. This arrangement sounds too good to be true. Already, loopholes are being identified. An issuer-affiliated party like an exchange platform can pay interest. Or, the incentive to holders can be relabeled a “reward.” Regulators may have difficulty preventing this behavior.

The use cases for stablecoins are becoming clearer. Their most immediate opportunities arise in the international context. Cross-border payments and remittances are often slow and costly due to the series of intermediaries involved; stablecoins can be exchanged directly. Residents of nations with weak and unstable currencies may be the most rapid adopters of future U.S. stablecoins. The easier international exposure to the dollar may also support global lending and facilitate exchange rate transactions.

Mainstream domestic adoption will require something new to compel a change; existing payment protocols are working well enough today. Stablecoins can underpin smart contracts, payments that are programmed to be contingent on an embedded rule. They may see adoption as a faster and more secure payment method than checks for business-to-business payments. Widespread consumer uptake could come from an organized push by merchants seeking to reduce their payment processing costs, but no such effort is yet underway.

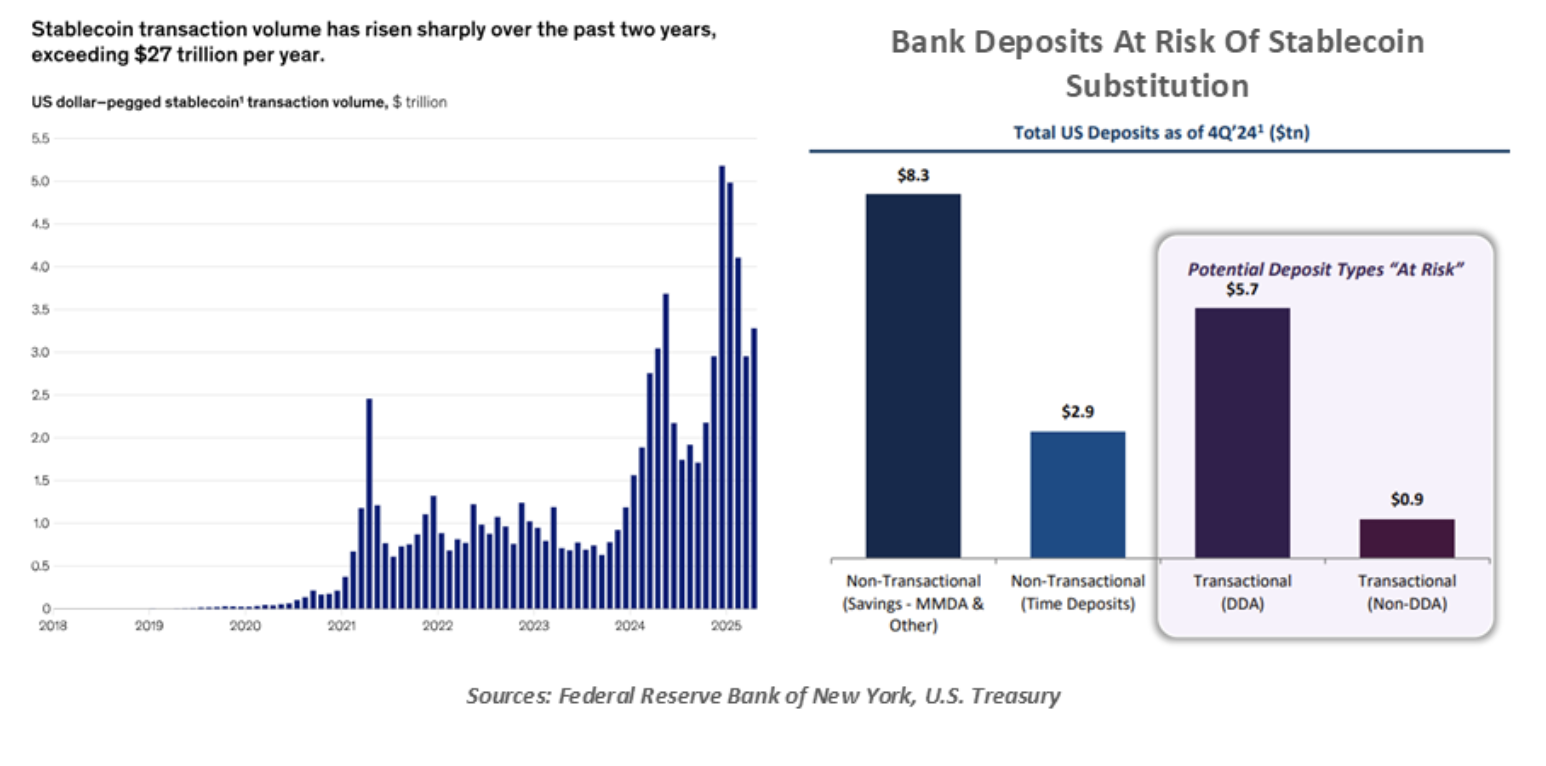

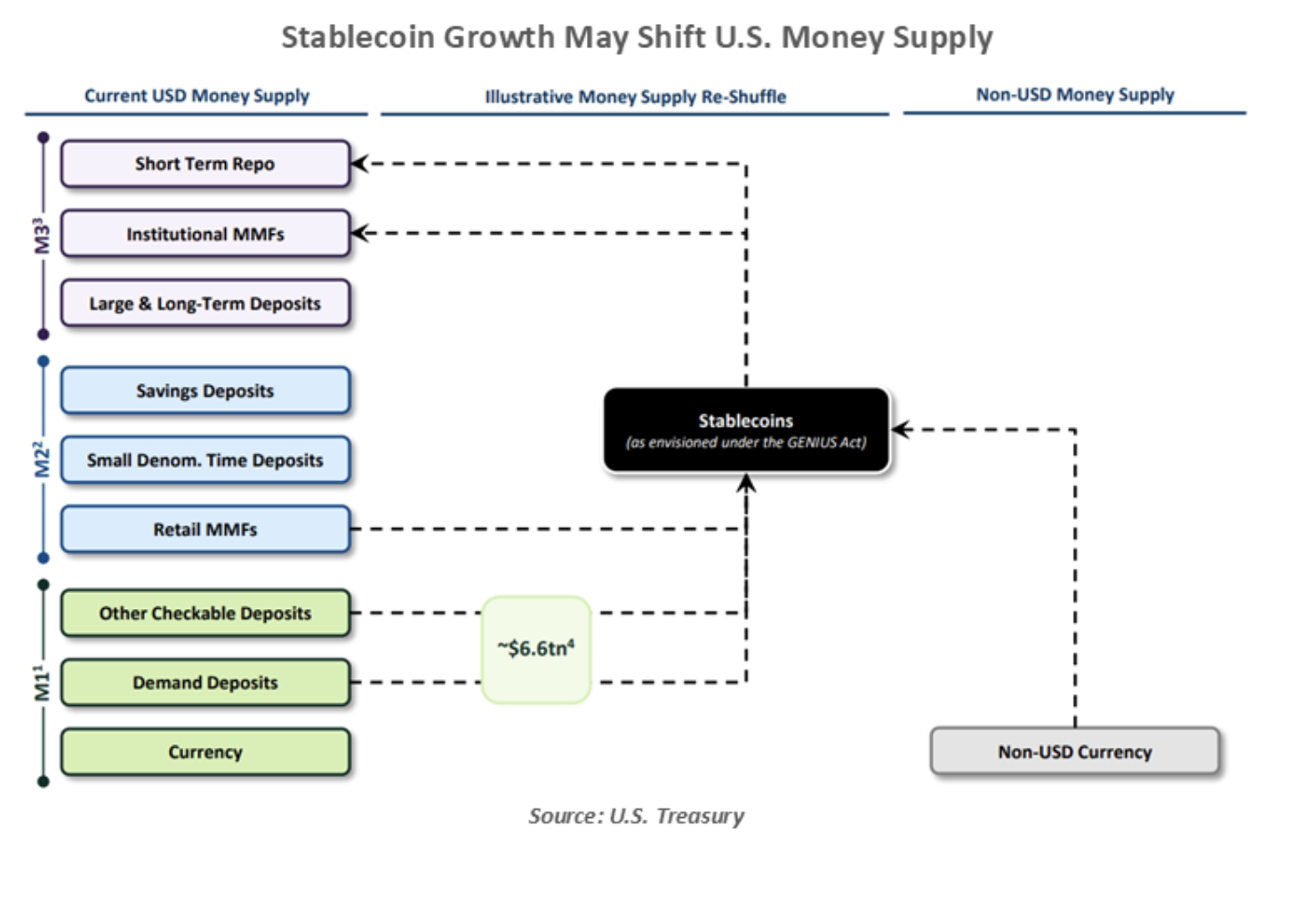

The financial sector will face disruption. Stablecoins could prove to be competition for bank deposits and money market fund shares. A loss of deposits will raise banks’ funding costs, impairing their capital and leading to higher interest rates for loans. The smaller the bank, the greater the pain of higher funding costs. As stablecoin volumes increase, their issuers will become a greater source of demand for Treasuries and money market shares; time will tell whether they represent net new demand or a reshuffling of existing demand.

Rulemaking is nascent today, with only the Treasury thus far issuing a request for comment. We encourage regulators to give thought to interoperability of stablecoins, facilitating flows across chains. Without this capability, the U.S. risks a reversion to its historic frictions of currencies issued by individual banks or states.

The GENIUS Act only applies to payment stablecoins. The crypto evolution will continue well beyond this application. Several major banks are working toward tokenized deposits, moving electronic funding into a blockchain structure. The “rails” of existing interbank payment networks are dated, and the investment may facilitate faster and easier transfers. Further efforts are underway to codify the blockchain to be used for investment transactions, legal contracts and more. The CLARITY Act has been drafted to offer a wider framework for the regulation of digital assets.

Stablecoins are in their growth spurt, a time that may be fractious and stressful for all involved. Maturing includes behavioral development, reflecting a greater understanding of one’s role in the world and duties to others. The GENIUS Act is an important milestone on this developmental journey, but we will be braced for further growing pains along the way.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Gain exposure to the evolving digital asset landscape. Learn about CoinShares ETFs.

© Northern Trust

Read more commentaries by Northern Trust