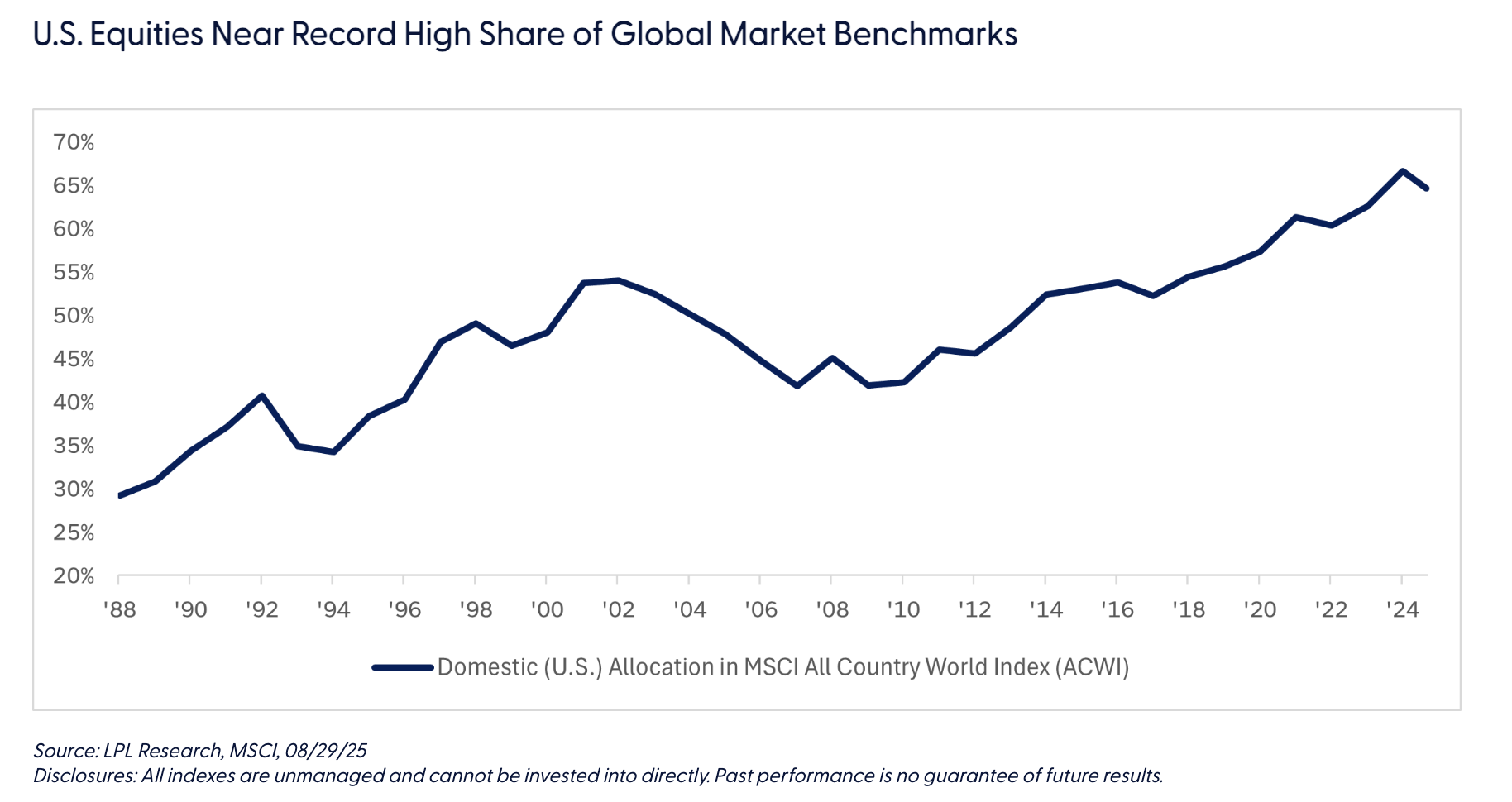

Recent data shows that even after strong international stock performance year-to-date U.S. stock markets continue to dominate global equity indexes, representing around two-thirds of the market capitalization of all global stocks, as represented by the MSCI All Country World Index (ACWI). This proportion still is close to record highs, reflecting not just the strong sustained outperformance of domestic equities, but a long-term shift in global market leadership. As a proportion of global equities, the U.S. accounted for under 30% in 1988, and just 42% as recently as 2010, so what caused this shift to where we stand today?

First, performance. Over the past few decades, and especially the 17 years since the U.S emerged from the Great Financial Crisis (GFC), U.S. stocks have outpaced international peers, driven by stronger earnings growth, better capital efficiency, and a more dynamic corporate ecosystem. The rise of mega-cap tech firms — many of which didn’t exist or were in their infancy in the late 90s — has been a major contributor.

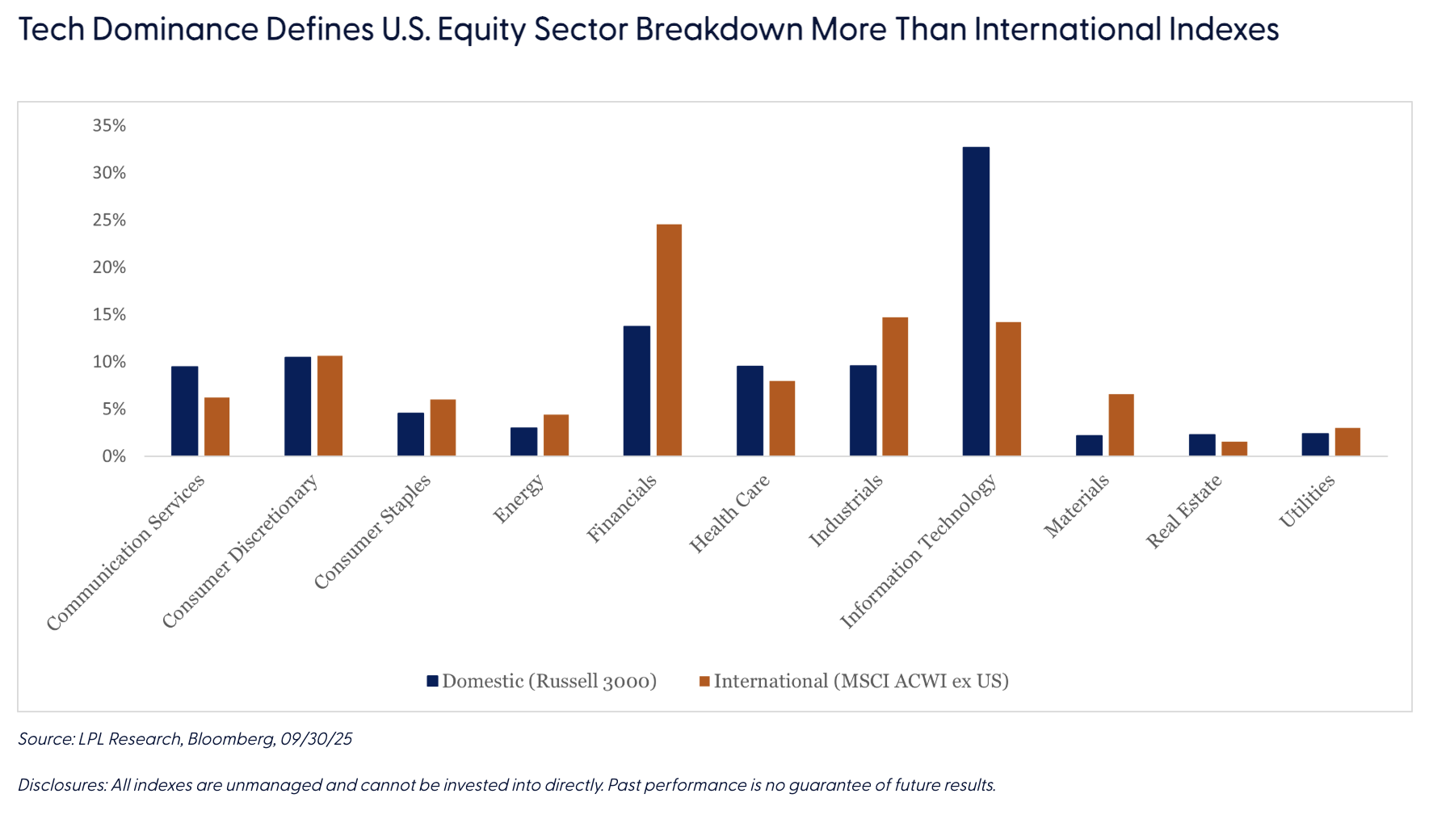

Second, sector composition. U.S. indexes are heavily tilted toward technology, with the Russell 3000, for example, exhibiting over 33% (a record high) in tech versus 14% in the rest of the world’s equity markets (developed international markets alone have even less, as European markets especially lack significant tech exposure). This tech advantage — especially in Artificial Intelligence (AI), cloud, and semiconductors — has translated into higher margins and faster growth for domestic equities. S&P 500 operating margins are expected to reach 18.9% next year, compared to 15.8% for developed international equities for example.

Third, domestic macroeconomic resilience. The U.S. economy has consistently outgrown major developed markets such as Europe and Japan, supported by technological innovation, willingness of government to engage in fiscal stimulus (like the recent One Big Beautiful Bill Act), and robust domestic consumer demand. Political uncertainty, aging demographics, and limited exposure to high-growth sectors have weighed on many developed international markets. Over a longer-term time frames, emerging markets have also struggled to convert economic growth into shareholder value with a strong U.S. dollar, political instability, and weaker corporate governance weighing on performance.

Conclusion

Despite the increasing dominance of U.S. equities in global market cap indexes – driven by nearly two decades of consistent outperformance - LPL Research continues to believe in the long-term benefits of international diversification. While the LPL Research Diversified Benchmarks, we use as our baseline for constructing multi-asset model portfolios and for measuring our relative performance, are tilted towards the U.S. they maintain allocations to both developed and emerging market equities. These benchmark allocations reflect our ongoing conviction that international equities play a vital role in managing risk through portfolio diversification, capturing opportunities across a broad and diverse set of global markets. While U.S. leadership may persist, shifts in currency dynamics, sector innovation abroad, or geopolitical developments - both domestic and international, could reshape global equity leadership over time.

George Smith chairs the Tactical Model Portfolio Committee, which manages LPL Financial’s multi-asset models across multiple managed account platforms.

A message from Advisor Perspectives and VettaFi: Looking for a way to gain exposure to the evolving digital asset landscape? Learn about CoinShares ETFs.