The equity market has shown remarkable resilience over the past two weeks despite rising U.S.-China trade tensions, a spike in equity market volatility, and growing credit concerns tied to business development company (BDC) and regional bank lending losses. While these factors have pulled the S&P 500 back from record highs, technical damage at the index level has been rather minimal. The more notable developments have arguably occurred in the money markets.

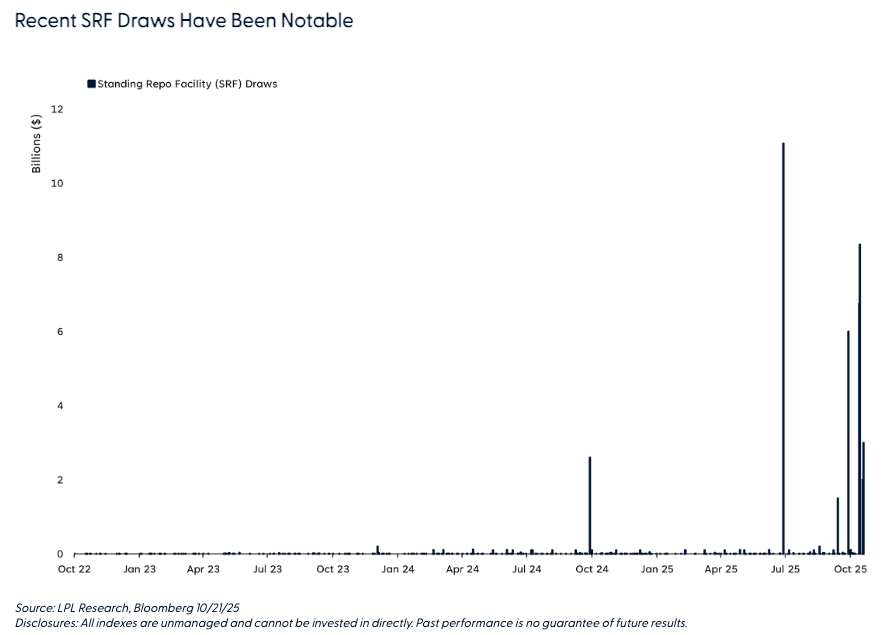

Last Thursday, for instance, the Federal Reserve’s (Fed) Standing Repo Facility (SRF) was tapped for $8 billion. It was then tapped again for $2 billion on Monday. The SRF is a permanent tool the Fed uses to keep short-term interest rates stable and ensure the smooth functioning of money markets. It operates by offering overnight loans to banks and eligible institutions in exchange for high-quality collateral such as U.S. Treasuries, with the collateral repurchased the following day at a modest interest cost. The SRF is really meant to serve as a safety valve of sorts — if banks can’t easily borrow cash in the market, they can always turn to the Fed at a set interest rate. Through this mechanism, the Fed can prevent sudden spikes in borrowing costs and help alleviate short-term run-of-the-mill funding pressures.

While the SRF is offered daily, usage outside of typical quarter-end liquidity crunches is unusual and may signal that system-wide liquidity is beginning to tighten more meaningfully. This matters for equities because abundant liquidity is inherently supportive of risk assets. Conversely, when liquidity conditions become tighter, investors tend to become more selective, creating a potential headwind for risk assets such as equities.

All that said, sporadic draws on the SRF do not constitute a trend. However, if usage of the SRF becomes more persistent, it could be a clear indication that liquidity is starting to meaningfully tighten and present a dynamic that equity markets would likely find difficult to ignore. In short, these early signs of tightening liquidity warrant close monitoring as signs of more persistent stress in the funding markets could easily shift the risk backdrop for equities.

LPL Research’s Strategic and Tactical Asset Allocation Committee (STAAC) remains neutral on global equities, with benchmark allocation recommendations across domestic, developed international, and emerging markets. Within the U.S., we prefer large caps over small caps, and growth over value.

Kristian Kerr drives the broad, house investment strategy for LPL Financial Research. His career includes over 25 years of industry experience.

A message from Advisor Perspectives and VettaFi: Stay ahead of market changes with our daily updates on key market and economic indicators. Visit the AP Charts and Analysis site for our expert insights.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #814631

Read more commentaries by LPL Financial