EM debt continued to deliver in the third quarter of 2025, supported by resilient fundamentals and steady investor demand. Equities and gold hit record highs, and U.S. Treasury yields fell on expectations that the U.S. Federal Reserve would begin cutting rates in September. Against this backdrop, the J.P. Morgan EMBI Global Diversified Index returned 4.75%, driven by spread tightening and carry, with high-yield debt once again outperforming investment grade debt.

While policy and geopolitical risks persist, we believe many countries are better positioned to absorb trade shocks and attract funding. And with spreads near historical lows but yields still elevated, we believe the asset class continues to offer compelling opportunities—particularly in high-yield and select frontier markets.

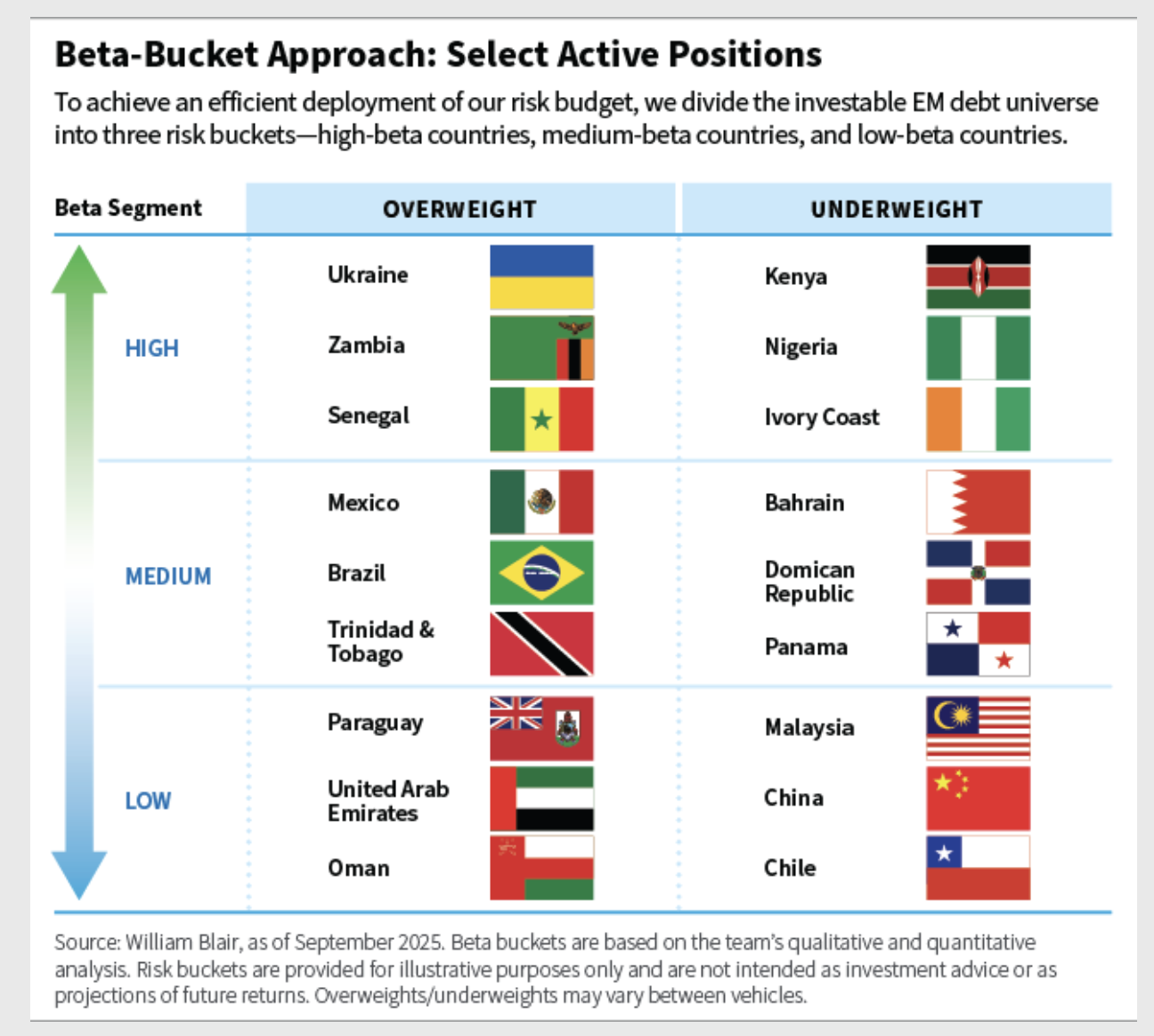

Below, we break down some of our largest active hard-currency positions by beta bucket, which is how we allocate our risk budget.

High-Beta Bucket

The largest overweight positions on a spread duration basis were in Ukraine, Zambia, and Senegal. Conversely, the largest underweight positions were in Kenya, Nigeria, and Ivory Coast.

Ukraine (overweight): We see potential for conflict negotiations, multilateral support, and a more optimistic growth outlook. We express this view through an overweight to warrants, but recently reduced our allocation to the A bonds based on valuations—that is, to raise the beta in case of misplaced pessimism in the conflict resolution.

Zambia (overweight): We are overweight after exchanging into two performing bonds following the country’s debt restructuring, including one with likely coupon step-ups within a year. As drought effects fade and copper mine investment rises, we believe Zambia’s fundamental outlook is good.

Senegal (overweight): Despite volatility after revelations of higher-than-expected debt, we remain overweight given expected International Monetary Fund support and the government’s strong commitment to fiscal consolidation.

Kenya (underweight): We hold a small underweight due to skepticism over the fiscal outlook despite new UAE funding. Efforts to reduce borrowing have met resistance, and further tax hikes or spending cuts appear politically difficult. Further cuts in expenditure are also likely to prove challenging, drawing into question the current macroeconomic plan that is in place under an IMF reform package. The credibility of this administration depends on narrowing the deficit and improving revenue collection as public discontent rises ahead of the 2027 elections.

Nigeria (underweight): Though we are neutral sovereign credit, we maintain a small cash underweight amid tight valuations. While exchange rate and monetary reforms and the launch of the Dangote refinery mark progress, structural challenges persist. Recent oil price volatility also poses risks to government revenues.

Ivory Coast (underweight): With presidential elections at the end of October, we remain cautious. While the incumbent is favored to win, polls have been a poor indicator of election results in recent years, and past post-election tensions and already tight spreads keep us cautious.

Medium-Beta Bucket

The largest overweight positions on a spread duration basis were in Mexico, Brazil, and Trinidad and Tobago. Conversely, the largest underweight positions were in Bahrain, Dominican Republic, and Panama.

Mexico (overweight): We remain overweight Pemex, supported by strong sovereign backing and attractive relative valuations. We are also overweight the sovereign itself on valuation grounds and maintain select corporate positions.

Brazil (overweight): We recently added corporate exposure, seeing better value after strong sovereign performance earlier in the year. Positions include oil and gas names—both independent producers and issuers linked to Petrobras—as well as an environmental services company.

Trinidad and Tobago (overweight): We find valuations attractive relative to peers. While fundamentals are softening, the country’s strong starting position and sizable Heritage and Stabilization Fund provide solid support.

Bahrain (underweight): Concerns include growing volatility in regional geopolitics, the country’s relatively weak fiscal-reform efforts, lower oil prices, and tight valuations. The new issue in September also contributed to increasing supply in the region.

Dominican Republic (underweight): Fundamentals remain strong for the region, but we see little value versus peers.

Panama (underweight): We reduced our exposure following an impressive rally in August. We believe the country’s risk/reward profile is less attractive, as we think there remains a reasonably high probability of a downgrade.

Low-Beta Bucket

The largest overweight positions on a spread duration basis were in Paraguay, United Arab Emirates, and Oman. Conversely, the largest underweight positions were in Malaysia, China, and Chile.

Paraguay (overweight): Valuations appear attractive versus low-beta peers and fundamentals seem solid. The country’s ratio of debt to gross domestic product remains low, and it has a strong history of low fiscal deficits.

United Arab Emirates (overweight): Our overweight position is driven predominantly by a combination of corporates and the smaller emirates, where we believe valuations are attractive relative to Abu Dhabi.

Oman (overweight): We believe the country’s fundamental credit improvement story remains firmly intact. As oil prices have fallen, Oman stands out as a defensive play in the region to further energy price volatility given its firm commitment to fiscal discipline and debt reduction.

Malaysia (underweight): We are underweight sovereign bonds as a result of tight valuations. We hold selective overweight exposure in quasi-sovereign bonds on more attractive valuations relative to the sovereign bonds in the index.

China (underweight): Valuations are tight and regulatory risks are unpredictable for Chinese state-owned entities. Based on a bottom-up analysis, we hold selective corporate bonds at what we believe are attractive valuations and positive credit trajectories.

Chile (underweight): We find better value in other low-beta credits. Although we do not expect the November elections to be impactful in terms of credit spreads, we believe there is the tail risk of a negative surprise.

Marco Ruijer, CFA, is a portfolio manager on William Blair’s emerging markets debt team.

A message from Advisor Perspectives and VettaFi: Ready for your next career move?Explore our articles on financial advisor transitions.

This content is for informational and educational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented.

Investing involves risks, including the possible loss of principal. Equity securities may decline in value due to both real and perceived general market, economic, and industry conditions. The securities of smaller companies may be more volatile and less liquid than securities of larger companies. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets and frontier markets. Different investment styles may shift in and out of favor depending on market conditions. Individual securities may not perform as expected or a strategy used by the Adviser may fail to produce its intended result.

Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit, and inflation risk. Rising interest rates generally cause bond prices to fall. High-yield, lower-rated, securities involve greater risk than higher-rated securities. Sovereign debt securities are subject to the risk that an entity may delay or refuse to pay interest or principal on its sovereign debt because of cash flow problems, insufficient foreign reserves, or political or other considerations. Derivatives may involve certain risks such as counterparty, liquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Diversification does not ensure against loss. The inclusion of Environmental, Social and Governance (ESG) factors beyond traditional financial information in the selection of securities could result in a strategy's performance deviating from other strategies or benchmarks, depending on whether such factors are in or out of favor. ESG analysis may rely on certain values based criteria to eliminate exposures found in similar strategies or benchmarks, which could result in performance deviating.

Collective Investment Trusts (CITs) are available to qualified retirement plans. For non-U.S. citizens or residents, William Blair offers a series of Luxembourg-domiciled SICAV products.

There can be no assurance that investment objectives will be met. Any investment or strategy mentioned herein may not be appropriate for every investor. References to specific companies are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future returns.

| | | |

Read more commentaries by William Blair