People of my generation were expected to have a basic familiarity with automobile maintenance. At my peak, I was able to change spark plugs, filters, headlights, hoses and batteries.

Many of those components came from the Autolight line, which later became part of the First Brands Group. First Brands filed for bankruptcy late last month, training investor headlights on the credit markets.

Rumors surrounding the company had been swirling for months. As a private firm, First Brands was not subject to the same kind of reporting standards that public firms are. An auditor had certified its financial statements last spring, but apparently had not understood the layers of debt the company had taken on. At the end, there was a $2 billion hole in the firm’s balance sheet.

First Brands had tapped a wide range of financing sources. Its long-term borrowing has been packaged into securities that were sold to investors in the form of collateralized loan obligations (CLOs). It made liberal use of leveraged loans, secured by cash flows. The company used its accounts receivable as security for short-term cash needs. In the spring, it received a loan from a private credit fund.

This diversity of debt is not at all unusual for private firms, but sustaining it relies on investors’ confidence in a company’s finances. While analysts have highlighted the idiosyncratic nature of the fall of First Brands, some investors have interpreted the event more broadly. Redemptions from funds containing the instruments employed by the company have accelerated in recent weeks.

We highlighted the issues surrounding private credit last year. The sector has grown rapidly over the past decade, thanks to attractive returns. Concerns center on light levels of regulation and reporting, which make it difficult to fully appreciate the risks involved. As often happens, questions are muted until adversity strikes. When it does, it provokes a powerful behavioral reaction, and contagion can ensue.

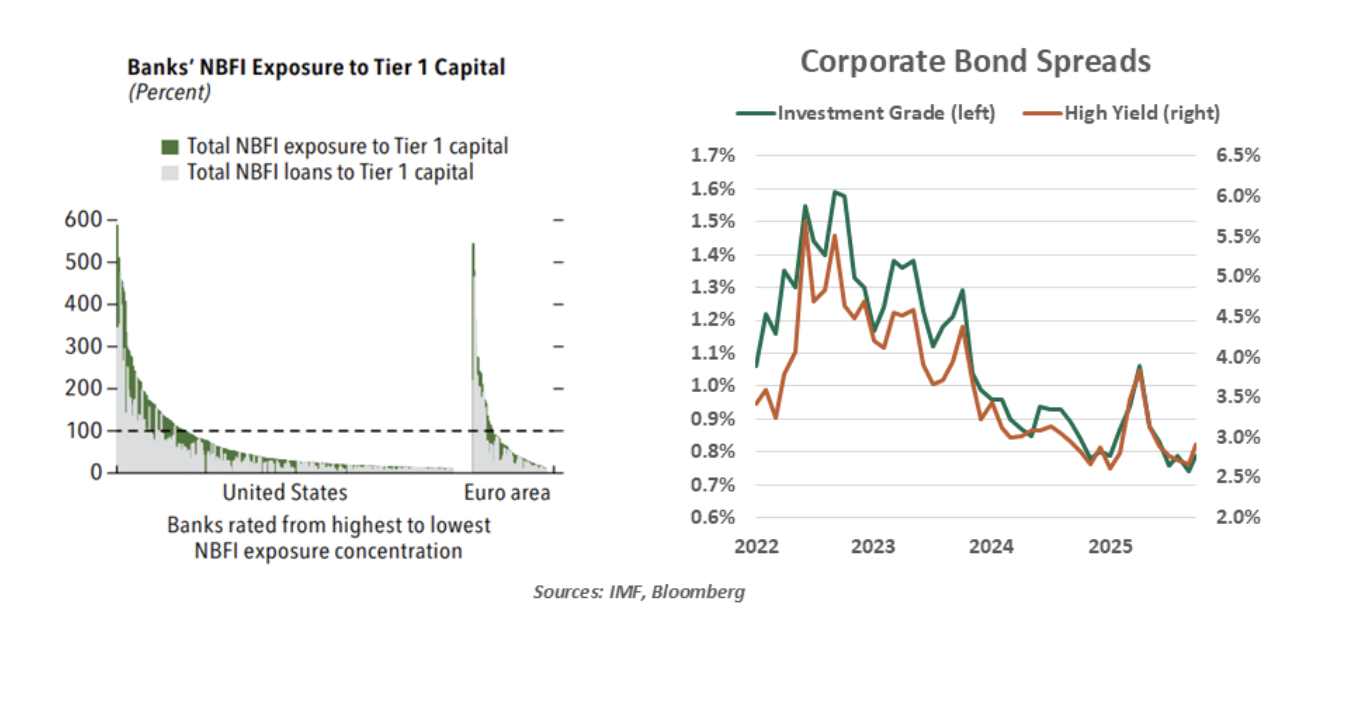

Credit extended directly by investors to corporations typically comes from funds or pools which are very well capitalized, and reasonably remote from the banking system. But in its October Financial Stability Report, the International Monetary Fund found that some banks have substantial exposure to non-bank financial institutions (NBFIs). It was these linkages that proved especially pernicious during the 2008 financial crisis, and which have been a focus of systemic concern ever since.