While many lessons have evolved over time, one maxim has never changed for children: look both ways before crossing the street. I reinforced with my children to then look again. We might not see everything on a quick glance, and traffic can change quickly.

Leaders around the world are dealing with risks emerging from all directions. Many nations are finding domestic consumption is receding, with export prospects also limited by a difficult trade environment. Prospects for stimulus are constrained by stretched fiscal budgets. Central banks are increasingly finding their objectives in conflict, most recently in the U.S.; economic data can be parsed to make the case for both cutting and holding.

The key to pedestrian safety is patience. Don’t rush into the street, as a safe opportunity to cross will eventually appear. Policymakers are shifting toward a similar posture of patience. Tariff escalations from the U.S. have slowed, and central bank rate cuts have tapered. After many rapid movements created stress over the past year, a slower and more stable outlook is taking shape.

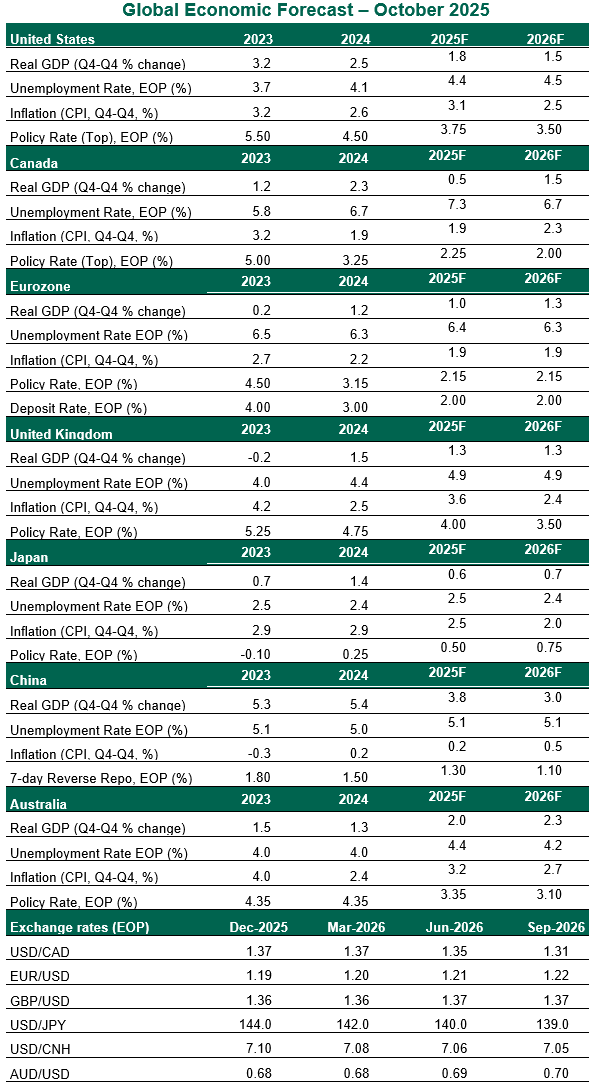

Following are our thoughts on how top markets are faring.

United States

- A prolonged government shutdown has compounded the complexity of assessing the state of the U.S. economy. Private data sources confirm the slowing labor market trend that official statistics had begun to reveal over the summer. The consumer price index (CPI) for September – compiled as a special effort to inform next year’s Social Security payments – showed inflation remained stuck at 3.0% year over year. Though the rate of inflation leaves room for improvement, markets were cheered that it has not accelerated as rapidly as feared.

- U.S. policy has become somewhat more stable. Tariff escalations are less frequent than they were earlier in the year, with the focus of new tariffs narrowing to specific products. The Federal Reserve is also on a more predictable path in the near term. A sluggish labor market clears the way for two more cuts in the remainder of the year, with more to follow in 2026 depending on the path of inflation.

Canada

- Canada’s economy has lingered on the precipice of recession in the year to date. Gross domestic product (GDP) contracted by 0.4% in the second quarter, dragged down by sluggish exports and business investment. Unemployment remains elevated at 7.1%, and while September saw a modest gain of 60,000 jobs, hiring intentions among businesses remain subdued. Calm inflation and a cool economy will allow the Bank of Canada to make one more rate cut this year. Absent reflation, one more reduction in 2026 will likely conclude the cycle.

- Trade uncertainty lingers, with tensions recently renewed and negotiations stalled; the nation’s vast trade relationship with the U.S. remains an exposure. However, Canada’s prospects are not entirely dependent on trade. New fiscal stimulus and lower interest rates should propel the economy through 2026. A federal budget to be released in November should include new fiscal spending that will keep a floor under the economy next year.