Multi-Sector Credit Asset Allocation Perspectives

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKEY TAKEAWAYS

- Q3 growth estimates are picking up and gross domestic product (GDP) is likely to accelerate in 2026; not all sectors will benefit equally, and asset allocation will be essential.

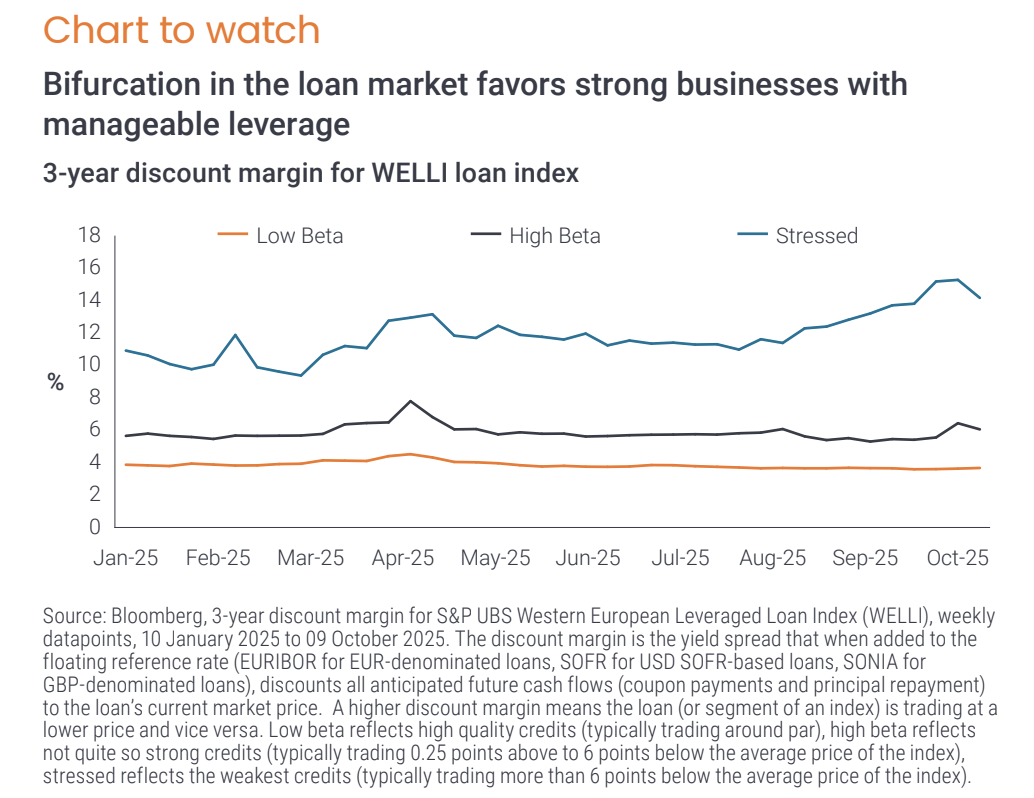

- Bifurcation is increasing – loan markets show a widening gap between stronger businesses with manageable leverage and weaker businesses with elevated leverage.

- The Fed is easing and has signalled a willingness to accelerate rate cuts if the labor market deteriorates further; this increases our confidence in the carry environment.

- The rapid expansion of AI infrastructure is creating compelling opportunities across fixed income sectors. We are investing around this theme to drive security selection in portfolios.

While valuations in most fixed income assets are toward the richer end of long-term ranges, Europe’s levered credit markets tell a different story with the WELLI (Western European Leveraged Loan Index) trading closer to its long-term average. Significant dispersion underlies the headline figures and we divide this market into three segments — low beta, high beta, and stressed — to demonstrate. Trading in the low and high beta segments has been orderly. Persistent demand and repricing activity have narrowed the margin of the low beta segment this year. The high beta segment trades with more volatility but has remained rangebound outside of a brief Liberation Day spike. The stressed segment has materially underperformed its counterparts. This segment has grown as a proportion of the overall index as vulnerable credits fall into it. Weak trading, often accompanied by challenged liquidity with few natural buyers, has exacerbated price declines which show up in higher discount margins. The larger and wider stressed segment is pushing out index-level spreads.

While the overall economy is in decent shape and many financial benchmarks are near highs, it can be easy to overlook pockets of fragility. Deep research and a disciplined portfolio construction process can help active managers identify risks early and avoid potential downside.

Amid solid growth and a more accommodative Fed, carry remains key

The US growth outlook is improving with third-quarter GDP estimates moving up toward 3%, bolstered by the capex budgets of hyperscalers. Immigration policy has reduced labor supply; while headline jobs data continues to soften, the payroll numbers required to hold a steady unemployment rate are now materially lower, with estimates in the 30,000 to 60,000 range. The government shutdown is delaying delivery of economic data, but we expect the situation to be resolved with little impact. Looking to the year ahead, easing monetary policy, tax cuts, a lapping of tariff impacts, and regulatory relief all paint a constructive picture for growth. We expect inflation to pick up, which could complicate the Fed’s path and this remains one of the largest risks.

Spreads in most fixed income assets remain relatively tight. With a solid economic backdrop and the ‘Fed put’ now in play, we believe we are positioned to capture carry through assets that still offer value. Investors should benefit from an overweight to asset exposure at the front end of the curve (i.e. among securities with shorter remaining terms to maturity), earning a high level of income, and maximizing yield per unit of duration/risk.

Dynamic allocation

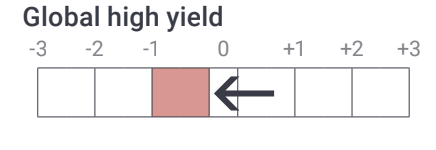

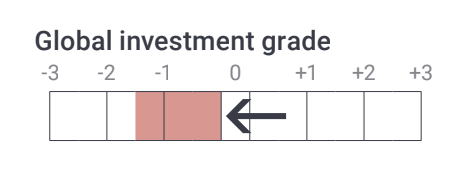

We use an internal qualitative and quantitative asset allocation model to evaluate the sectors within our multi-sector credit universe. Sectors are rated from -3 to +3 across fundamentals, technical (or market dynamics), and valuations. During our asset allocation meeting, the summary of these scores is used to rate sectors relative to each other. The result is reflected in portfolio sector allocation. The views and scores are those held at the end of Q3 2025.

Views

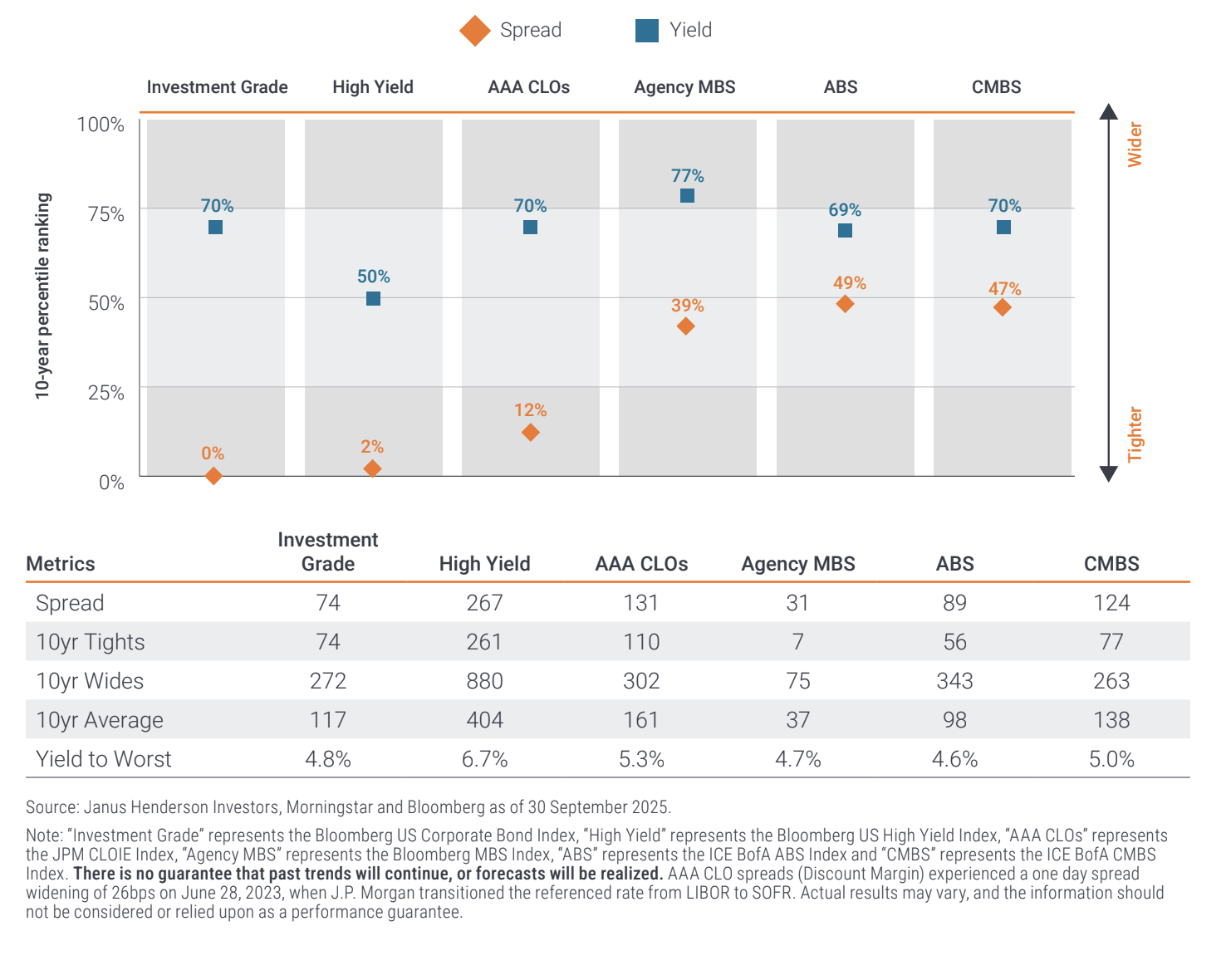

Spreads on the Global high yield (HY) Index have widened recently, though remain tight by historical standards. The average price on HY bonds is now in the mid-to-high 90s with yields in the high 6s%.1 September was one of the highest issuance months the US High Yield market has ever seen. Deals were initially taken down well and trading higher on the break, though we have seen some indigestion more recently alongside elevated dealer inventories. The asset class has enjoyed moderate inflows over the past few months. The default rate remains very low at 1.4%.2

Views

Global investment grade (IG) spreads have continued to grind over the past few months and remain near the tights. Corporate earnings and consumer spending are holding up. While we do not see a lot of downside given strong fundamentals, current spread levels point to an environment where return potential for IG is mostly limited to carry. Our aim is to take differentiated exposure to specific IG credits with clear catalysts for spread tightening. Overall, we prefer the higher carry of securitized assets.

Views

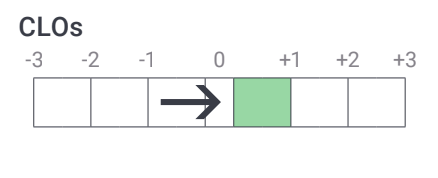

Collateralized loan obligations (CLOs) are tighter, with compression across ratings categories in secondary trading. AAA tranches of new 5nc2 deals (5-year maturity and 2-year non-call period) from Tier 1 US issuers are being talked at around 120bps (of spread), which is wide of the year-to-date tights set in February. CLO warehouse levels are near all-time highs in both the US and Europe. Managers are favoring resets and refinancings due to current market conditions and documentation changes. We continue to prefer AAA CLOs to IG credit due to higher carry and less credit risk. We also think BBB tranches look somewhat cheap versus high yield corporates. We score AAA +1.5 and BBB +0.5.

Views

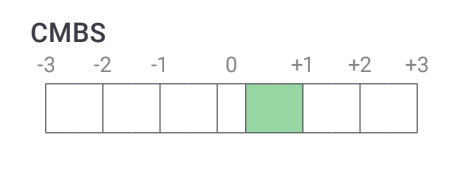

Commercial mortgage-backed securities (CMBS) technicals remain strong with robust demand, especially for high-quality office and benchmark deals, and spreads have tightened slightly. Office markets in San Francisco and New York City continue to show signs of recovery; we are focused on strong assets and sponsors, though there is limited opportunity to add given strong demand and few sellers. In our view, data centers are undervalued given their resilience from strong demand and long-term contracts with hyperscalers that reduce lease rollover risk. The market is expected to benefit from lower rates and increased refinancing activity with no major concerns about the maturity wall.

Views

Mortgages have benefited from lower volatility and a steepening yield curve, with technicals supported by inflows and passive ETF growth. Fundamentals are steady, with low prepayments and manageable net supply, while valuations have tightened. Non-Qualifying Mortgage issuance has been high but absorbed well due to strong demand from insurance companies. Fundamentals have shifted from a positive tailwind to a more neutral stance, as housing price appreciation has faded and supply has increased, but there is no sign of major deterioration. Our overall outlook is constructive, and we continue to see value in seasoned Credit Risk Transfer tranches and certain non-QM deals. We score Agency MBS +0.5, RMBS +1.

Views

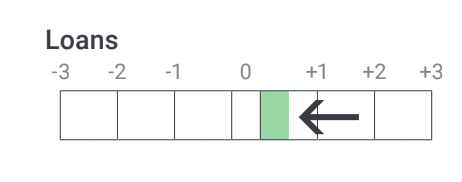

The loan market has traded off recently with significant bifurcation between low beta and high beta segments. Low beta loans are seeing persistent demand from CLO rampers, but there is little appetite for high beta loans, particularly in sectors experiencing downcycles. Heightened CLO reset activity is offering managers an opportunity to sell underperforming loans, which is driving some of the weakness. With more loans trading below par, near-term repricing activity will be subdued, and prospects for earning carry improve without margin reductions. 25bps extra margin in Euro tranches vs US tranches remains the norm. We score US loans at 0 and EU loans at +1.

Views

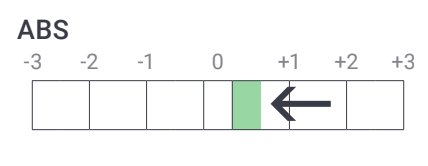

The tone in the asset-backed securities (ABS) market is cautious due to the recent issues with Tricolor, which have led to wider spreads at the lower end of the capital stack and more tiering among issuers. We believe that this situation was unique and not indicative of more widespread issues in auto/consumer ABS. However, it has further increased scrutiny on the health of the lower-end consumer. There is a bifurcation, with low end (poorer) consumers struggling while high end (wealthier) consumers benefit from better wage growth and equity and house price appreciation. We are seeing increased delinquency rates in subprime and are favoring the prime consumer. Investors benefit from structural protections in these securitizations and, historically, cumulative loss rates have stayed meaningfully below attachment points for IG-rated tranches. ABS has continued to offer attractive spread pickup versus similarly rated corporate bonds.

Views

Emerging Market (EM) high yield has outperformed corporate high yield recently and is trading somewhat rich relative to history. While both EM BBs and Bs have rallied, it is the single-B category that is driving this relationship, with BBs remaining closer to median levels on a relative basis. Issuance has picked back up, but technicals remain favorable with new deals oversubscribed. We are still constructive on the growth prospects of many emerging market economies and EM debt has behaved with less volatility than corporate high yield. In geopolitics, Israel and Hamas agreed to a U.S.-brokered ceasefire, ending the two-year war.

Theme in focus: AI Infrastructure

The expansion of digital infrastructure required by increased artificial intelligence (AI) workloads is creating compelling investment opportunities across fixed income. Data centers have become a prominent subsector in securitized credit where issuers are increasingly using both CMBS and ABS structures to finance these assets. There are also growing numbers of corporate issuers operating in various parts of this ecosystem. CoreWeave leases and fills data centers with Nvidia graphics processing unit (GPU) clusters as well as the requisite networking and cooling equipment required to optimize them for high performance computing. It offers this product to a growing list of hyperscalers and AI labs that use it to run their AI workloads. Level 3 Communications’ fiber network links AI data centers to the broader internet

and cloud ecosystems. This allows AI workloads – like training large models or running real-time inference – to communicate across regions and with end users. Independent power producers (IPPs) are well-positioned to capitalize on the increase in power demand and prices driven by the electricity needs of these data centers. Some IPPs are signing power purchase agreements with hyperscalers, which we believe can offer stable, long-term contracted revenues. Companies involved in cloud computing, data centers and power infrastructure are all issuers of bonds in the high yield market.

The role of duration

Duration can act as insurance in times of economic uncertainty. Our duration is primarily being utilized for this role as a hedge against spread risk. It is concentrated toward the front end, where it can help dampen volatility in our front-end assets and would benefit if we see a slower economy or accelerated Fed rate cuts. We are less constructive on the back end of the yield curve given our constructive view on US growth and concerns around inflation and large government deficits. Rate-spread correlations remain negative, supporting the effectiveness of duration as a volatility dampener. We seek to source the best opportunities across fixed income sectors while achieving an optimal balance between spread and duration. A multi-sector credit approach can maximise the diversification benefits that fixed income has to offer.

John Lloyd, Janus Henderson’s Global Head of Multi-Sector Credit & Portfolio Manager.

1 Source: ICE BofA Global High Yield Index, as of 30 September 2025

2 Source: JPMorgan, as of 30 September 2025.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Glossary

Above par: When a bond trades above par, it means that the bond’s current market price is higher than its face value (also known as its par value). This typically occurs when the interest rate environment has changed since the bond was issued, specifically when market interest rates have declined below the bond’s coupon rate.

Agency Mortgage-backed Securities (Agency MBS): A type of asset-backed security that is specifically secured by a collection of mortgages. These securities are issued by one of the three government-sponsored enterprises (GSEs): Fannie Mae (Federal National Mortgage Association), Freddie Mac (Federal Home Loan Mortgage Corporation), or Ginnie Mae (Government National Mortgage Association).

Asset-backed Securities (ABS): These are financial instruments that are backed by a pool of assets—typically those that generate a cash flow from debt, such as loans, leases, credit card balances, or receivables.

Attachment points: This is the level of losses in the underlying assets that a specific tranche begins to absorb losses. Essentially, it is the point at which the protection for a tranche runs out, and it starts to “attach” to the losses. Beta: A measure of the volatility of a security or portfolio relative to an index. Less than one means lower volatility than the index, more than one means greater volatility.

Carry: Return earned from a security assuming its price remains unchanged. For a bond, carry is essentially the income generated by the bond less the cost of financing.

CLO rampers: These are entities or individuals involved in the ramp-up phase of CLO, where the CLO manager is actively working on building and optimizing the loan portfolio for a CLO.

CLO warehouses: A CLO warehouse refers to a portfolio of leveraged loans that is assembled and managed by a CLO manager. This “warehouse” acts as a temporary holding place for these loans until they can be packaged into a CLO. Collateral: In a securitisation, collateral refers to the pool of financial assets that are bundled together to form the basis of a security. Commercial Mortgage-backed Securities: A type of mortgage-backed security that is secured by the loan on commercial real estate properties rather than residential real estate.

Convexity: In the context of bonds, convexity measures how a bond’s price sensitivity to interest rate changes (duration) changes as interest rates fluctuate. Convexity quantifies how much more the bond’s price will increase when interest rates fall, or how much more the price will decrease when interest rates rise, compared to what duration alone would predict. Credit Risk Transfer: CRT in mortgages is an investment opportunity where investors take on some or all of the credit risk associated with a portfolio of mortgages, typically from a bank or government-sponsored enterprise (GSE) Duration: Duration can measure how long it takes, in years, for an investor to be repaid a bond’s price by the bond’s total cash flows. Duration can also measure the sensitivity of a bond’s or fixed income portfolio’s price to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Fundamentals: In the context of corporate debt, “fundamentals” refer to the essential financial health indicators and characteristics of a company that suggest its ability to meet debt obligations.

GPU cluster: This is a network of interconnected computers, each with multiple Graphics Processing Units (GPUs), that work together to perform large-scale, parallel computations.

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate.

Hyperscalers: These are companies that provide cloud, networking, and internet services at a massive scale, typically involving expansive data centers and infrastructure.

Investment grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Multi-Sector Credit Asset Allocation Perspectives

Loans: Also called “Leveraged loans”. Loans to companies that tend to be rated below investment grade. On the break: This refers to when a new issue first starts trading i.e. if it prices at par ($100) and then when it starts trading, it immediately trades up to $101, it is trading higher on the break.

Quantitative Easing (QE): A government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market.

Real-time inference: The process of using a trained AI model to make predictions or decisions based on new, live data as it is received, with minimal latency.

Residential Mortgage-backed Securities (RMBS): A type of mortgage-backed security that is secured by the interest in residential real estate loans.

Seasoned vintages: In the context of credit risk transfer, particularly in the mortgage industry, “seasoned” vintages refer to mortgage loans that have been outstanding for a significant period, typically at least several years. These loans have a track record that provides data on payment history, default rates, and other performance indicators.

Spread: The credit spread is the difference in yield between securities with similar maturity but different credit quality, often used to describe the difference in yield between corporate bonds and government bonds.

Spread risk: This refers to the potential for financial loss that arises from the widening of the credit spread between two debt securities.

Yield curve: This curve plots the yields (interest rate) of bonds with equal credit quality but differing maturity dates. Typically bonds with longer maturities have higher yields.

Yield-to-worst: The lowest yield a bond with a special feature (such as a call option) can achieve provided the issuer does not default.

Bank loans often involve borrowers with low credit ratings whose financial conditions are troubled or uncertain, including companies that are highly leveraged or in bankruptcy proceedings.

Collateralized Loan Obligations (CLOs) are debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Fixed income securities are subject to interest rate, inflation, credit and default risk. As interest rates rise, bond prices usually fall, and vice versa. High-yield bonds, or “junk” bonds, involve a greater risk of default and price volatility and can experience sudden and sharp price swings. Foreign securities, including sovereign debt, are subject to currency fluctuations, political and economic uncertainty and increased volatility and lower liquidity, all of which are magnified in emerging markets. Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

Index definitions

Bloomberg Euro Aggregate Index measures the investment grade, euro-denominated, fixed rate bond market, including treasuries, government-related, corporate and securitized issuers.

Bloomberg Global Aggregate Corporate Index is a measure of global investment grade, fixed rate corporate debt. The multi-currency benchmark includes bonds form developed and emerging market issuers within the industrial, utility and financial sectors.

Bloomberg Global Aggregate Index is a measure of global investment grade debt. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed rate bonds from both developed and emerging market issuers. Bloomberg Global High Yield Index is a multi-currency measure of the global high yield debt market. Bloomberg US Aggregate Index measures the investment grade, US dollar-denominated, fixed rate taxable bond market. It includes treasuries, government-related and corporate securities, MBS (agency fixed rate pass-throughs), ABS and CMBS (agency and non-agency).

Bloomberg US Corporate Bond Index measures the investment grade, fixed rate, taxable corporate bond market. Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed rate corporate bond market.

Bloomberg US Mortgage Backed Securities (MBS) Index tracks fixed rate agency mortgage backed pass-through securities guaranteed by Ginnie Mae, Fannie Mae and Freddie Mac.

Bloomberg US Treasury Index measures US dollar-denominated, fixed rate, nominal debt issues by the US Treasury.

Multi-Sector Credit Asset Allocation Perspectives

ICE BofA AAA US Fixed Rate CMBS Index tracks the performance of US dollar denominated investment grade AAA rated fixed rate commercial mortgage backed securities publicly issued in the US domestic market.

ICE BofA US Fixed Rate Asset Backed Securities Index tracks the performance of US dollar-denominated investment grade fixed rate asset backed securities publicly issued in the US domestic market.

J.P. Morgan Collateralised Loan Obligation AAA Index (CLOIE AAA) tracks the performance of AAA-rated debt tranches of broadly syndicated, arbitrage US dollar-denominated debt.

J.P. Morgan EMBI Global Diversified Index tracks liquid, US dollar-denominated emerging market fixed and floating rate debt instruments issued by sovereign and quasi-sovereign entities.

S&P UBS Western European Leveraged Loan Index (WELLI) measures the performance of the investible universe of EUR, GBP and USD leveraged loans issued by companies domiciled within eligible countries.

FOR MORE INFORMATION, PLEASE VISIT JANUSHENDERSON.COM

Important information

References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson, its affiliated advisor, or its employees, may have a position in the securities mentioned. The opinions and views expressed are as of the date published and are subject to change. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Janus Henderson® and any other trademarks used herein are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.

W-25-1701802-10-31-2026 400-10-1701802

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All