After years of researching equities, my research has started trending toward alternatives — including crypto, commodities, and private markets. It is not that equities have gone out of favor. But it is increasingly becoming more important to diversify portfolios. Diversification doesn’t just potentially enhance returns, but can do so on a risk-adjusted basis.

Part of that diversification story has been about expanding into private equity and private credit. And these strategies have become increasingly desired by retail investors who crave institutional level strategies. For financial advisors, one of the primary concerns is navigating the rapid growth of ETFs that are attempting to package these historically illiquid assets and integrate them into modern portfolios for a broad range of investors.

These are my takeaways (based on my own personal views) inspired by the panels at ALTSTX — an alternatives conference hosted by CAIA Association and the CFA Society Dallas/Fort Worth that is primarily attended by asset allocators and managers.

The 60/40 portfolio isn’t dead; it just goes beyond traditional stocks and bonds

In an opening segment by Ryan Chapman of Grove Lane Partners | GCM Grosvenor, he addressed the 60/40 portfolio. Over the past few years, there has been some controversy around the 60/40 portfolio. Many allocators have modified the traditional 60/40 portfolio to layer in private equity and private debt. This captures distinct drivers of return, including an illiquidity premium and different default/recovery dynamics. For retail advisors, this can mean using vehicles like interval or tender-offer funds, BDCs, listed alternative-asset managers, or ETFs to easily package these strategies alongside public equities and debt. The goal isn’t to replace the 60/40, but to modernize it by broadening sources of risk and income in client portfolios.

The cockroaches vs. termites imagery won’t leave our minds

The cockroach versus termites discussion wasn’t missing from ALTSTX. It was first touched on during a fireside chat with Mitch Julis of Canyon Partners LLC. For context, Jamie Dimon recently said, “When you see one cockroach, there are probably more.” He was referring to a single credit blowup that often isn’t isolated. As many of us can probably relate from our first dorms or college apartments, cockroaches usually multiply fast (and you may not even see them until it’s too late).

Mohamed El-Erian responded to Dimon’s comments and pointed out that cockroaches aren’t termites. Termites cause deep hidden damage that would threaten the whole financial house. But cockroaches are just scattered pests you can manage. Julis and other speakers at ALTSTX shared a similar sentiment as El-Erian. For advisors, that means not to completely shy away from these strategies, but plan careful due diligence and remember the basic principles like diversification and risk budgeting. In other words, expect a few roaches, but don’t assume the foundation is crumbling.

Retail investors and private markets?

There was some debate at ALTSTX on whether retail investors should be able to access private markets. On top of that, there is the question of whether an ETF is the best vehicle for a retail investor to access private markets (see more in my note here). Regardless of the answers, ETFs accomplish what they set out to do. And that is expanding access to retail advisors and self-directed retail investors in a familiar structure.

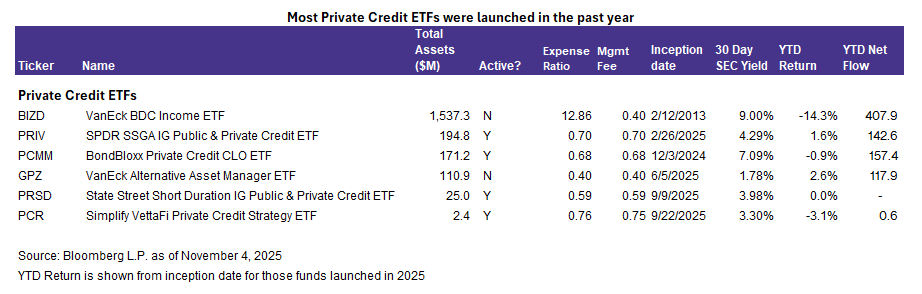

The amount of private market ETFs has surged over the past few years as many investors look for new ways to access the strategy. Several strategies exist, including: 1) accessing through a funds-of-funds structure with closed-end funds and BDCs; 2) accessing through investing in publicly listed private managers; and 3) using specialized strategies. Note this list isn’t entirely comprehensive since there are several other ETFs that follow the first strategy of holding BDCs and CEFs that aren’t included in my list.

Bottom Line:

With the attention that private markets — particularly private credit — is receiving in the allocator space, it makes sense that more retail clients are asking their advisors for ways to access the market. ETFs can help provide simple access in a familiar way, but it is important to differentiate among the different private credit ETF strategies and find the one that best suits your needs.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

VettaFi LLC (“VettaFi”) is the index provider for PCR, for which it receives an index licensing fee. However, PCR is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of PCR.

Read more commentaries by VettaFi