(Wednesday market open) Major indexes tried to mount a recovery early today after a private employment measure showed better-than-expected October jobs growth. The data came after stocks struggled Tuesday without help from the chip sector, which plunged and continued to edge down this morning as investors expressed disappointment with results from Advanced Micro Devices (AMD).

Private sector jobs growth last month totaled 42,000, the ADP employment report said, above Briefing.com's consensus of 26,000 and a 29,000 drop in September. ADP doesn't typically correlate with official government data due this Friday, which likely won't be released due to the shutdown. Jobs growth was bifurcated. "Small businesses continue to feel pain as companies with 1–19 employees saw a net-loss of 15,000," said Kevin Gordon, Schwab's head of macro research and strategy. "The largest companies were on top with a 74,000 gain." Yields rose after the news.

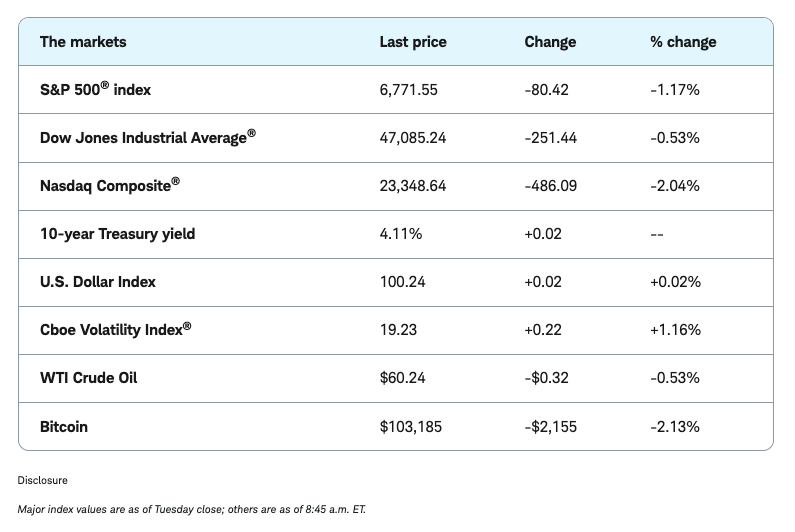

Major indexes suffered their worst session in nearly a month Tuesday as tech shares dove on worries about AI valuations. Dip buying failed to emerge. "Markets have been moving higher on the same good news, including trade agreements, a dovish Fed, a strong economy, and the AI secular growth story for months now, and perhaps some mean reversion is needed," said Nathan Peterson, director of derivatives analysis at the Schwab Center for Financial Research. He noted that Palantir (PLTR) easily beat earnings expectations but fell 8% anyway. "Market psychology comes into play here, because if these types of AI growth stocks are going to sell off on good news, how much are they going to go down on bad news?" Peterson said.

Three things to watch

-

Tell it to the judge—Supreme Court reviews tariffs: Today the Supreme Court begins hearing arguments challenging President Trump's import tariffs. Treasury Secretary Scott Bessent, who believes the tariffs are critical for U.S. trade policy, will attend. Though it's unclear when the court might rule and the initial market impact is unclear, investors might want to follow the news for hints of how the justices lean. Signs that they're willing to consider overturning the tariffs as an unconstitutional expansion of presidential power might be positive for Wall Street and interest rates. Just last week, Federal Reserve Chairman Jerome Powell said tariffs likely contributed to inflation. And numerous groups from both sides of the political spectrum encouraged the Supreme Court to rule against the administration, arguing that Congress, not the president, is responsible for tariff policy. Though the tariffs—which act as a tax on imports—pose a headwind for U.S. companies and consumers, there are signs some firms are growing used to them, so any shift might raise uncertainty.

-

Volatility up after weathering storm: The market sailed pretty much unscathed through a gauntlet last week of five mega cap earnings, a Fed meeting, and China trade talks. Despite all that, the Cboe Volatility Index (VIX), had a narrower weekly move than in the prior week. That changed Tuesday in a big way as spot VIX climbed double digits to above 19 and stayed there this morning. More choppiness could be ahead. Starting next month and stretching all the way out to mid-2026, VIX futures trade in contango, mainly between 21 and 22. Those aren't near historic highs but imply that the market faces unsettled times. One possible concern is relatively high stock valuations even after yesterday's tech pullback, as well as the increasing concentration of the long rally. By the end of last week, only 15% of S&P 500 stocks had outperformed the overall index over the last few months, and breadth has been thinning. As a reminder, the market can have narrow breadth without a pullback, but with no catalyst there's less news to support a big move, and any bad news for the few mega-cap stocks leading the charge could have a more widespread impact.

-

Bitcoin slide accelerates: Bitcoin faced a number of headwinds as it's tumbled more than 20% from a record high above $126,000 a month ago to below $100,000 on Tuesday, slicing through its 200-day simple moving average. First, a historic "flash crash" on October 10 reset leverage. Then the Fed's unexpectedly hawkish stance sapped some risk-on sentiment. Broader market conditions have also played a role, said Jim Ferraioli, director of digital currencies research at the Schwab Center for Financial Research. Higher yields in the wake of the Fed meeting and waning liquidity—due to the government shutdown and the Fed's quantitative tightening (QT)—have weighed on the coin, he said, but the coming end to QT and the government reopening could provide some relief. In all, bitcoin exchange-traded funds (ETF) have seen outflows of about $1.5 billion since that "flash crash."

On the move

-

Advanced Micro Devices became the latest AI-related stock to fall despite earnings and revenue exceeding consensus. Shares fell 3% in early trading, but were off overnight lows. Guidance topped Wall Street's estimates, but investors appeared to want more than the $9.6 billion revenue AMD forecast for the current quarter. Shares had more than doubled this year prior to yesterday's results, but several analysts raised their price targets after AMD reported.

-

Nvidia (NVDA), Broadcom (AVGO), Taiwan Semiconductor Manufacturing (TSM), and Intel (INTC) were among semiconductor stocks with heavy losses today that narrowed overnight. None were off sharply before the open despite a Reuters report that China banned foreign AI chips from data centers using state funds.

-

Tesla (TSLA) rose 1% in pre-market trading ahead of its annual shareholder meeting tomorrow. The looming question is whether a majority of TSLA shareholders vote for CEO Elon Musk's pay package.

-

Pinterest (PINS) fell almost 19% early Wednesday. The company topped analysts' expectations for global monthly active user growth but missed the average estimate on earnings per share. Guidance for the current quarter also came in slightly below the average estimate.

-

Arista Networks (ANET) became the latest tech firm to see shares dive double digits early Wednesday despite an earnings beat. Investors appeared disappointed by guidance, which was in line with expectations but failed to beat expectations. Shares fell 10% before the open.

-

Super Micro Computer (SMCI) joined Arista in the penalty box early today, down 7%, as quarterly revenue fell short of consensus and earnings per share missed the average estimate. The company also guided for second-quarter EPS below consensus.

-

Cava (CAVA) fell 4% in pre-market trading after the casual dining restaurant company cut its full-year forecast for the second straight quarter, CNBC reported. The company cited falling demand from younger consumers facing economic challenges.

-

Humana (HUM) dropped 4% despite reporting better-than-expected earnings. Shares slumped as Humana lowered its full-year guidance, Barron's reported.

-

McDonald's (MCD) edged up less than 1% after reporting quarterly revenue in line with analysts' expectations, up 3% year over year. Earnings per share came in slightly below consensus, possibly on increased spending, Yahoo Finance noted. Same-store sales, or sales at locations open at least a year, rose 3.6%, a bit better than Wall Street's 3.5% forecast.

-

Bitcoin (/BTC) bounced 2% early Wednesday after a 6% collapse Tuesday that took it below $100,000 at one point for the first time since late June. Shares of stocks linked to crypto, including Coinbase (COIN) and Strategy (MSTR) both rose 1.4% this morning.

-

Technically, the bullish uptrend remains intact on an intermediate-term basis, my colleague Peterson said, but the near term could see some consolidation or mean reversion. The S&P 500 index has now spent 143 days without touching its 50-day moving average, the third longest streak since 1990. The 50-day is now at 6,654, but the 20-day moving average is another important support point at 6,747, just below Tuesday's close.

- Despite yesterday's sell-off, the S&P 500 index starts today just 2% below its all-time high.

- For tomorrow's October Challenger job cuts report due before the open, analysts expect a rise to 73,000 after highly publicized layoffs by Amazon (AMZN), United Parcel Service (UPS), IBM (IBM) and Target (TGT). September's total was 54,000.

Purchased money market funds and margin loans: Because a money market fund can seem much like cash in a checking account, it's commonly assumed that purchased money market funds (PMMF) in a brokerage account get treated the same as cash in terms of margin loans. But they don't. Assuming that PMMFs in a brokerage account are treated the same as cash can lead to an unexpected margin loan and interest payments on that loan, not to mention surprise margin calls.

Bitcoin futures (/BTC—candlesticks) accelerated through previous support and the 200-day simple moving average (green) on Tuesday, reaching a cumulative decline of more than 20% over the past month, a common definition of a bear market. The Average Directional Index (ADX) has turned up, but remains just slightly below 20, a level commonly interpreted as confirming a trend is in place. In other words, it's not quite a downtrend yet but it's gathering steam.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This material is intended for general informational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results.

For illustrative purpose(s) only.

Investing involves risk, including loss of principal, and for some products and strategies, loss of more than your initial investment.

Diversification and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets.

"Indexes are unmanaged, do not incur management fees, costs, and expenses (and/or "transaction fees or other related expenses"), and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions and/or Schwab.com/IndexDefinitions. For additional information about the indices and terms shown, please visit www.schwabassetmanagement.com/resources/glossary.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

Digital currencies [such as bitcoin] are highly volatile and not backed by any central bank or government. Digital currencies lack many of the regulations and consumer protections that legal-tender currencies and regulated securities have. Due to the high level of risk, investors should view digital currencies as a purely speculative instrument.

Cryptocurrency-related products carry a substantial level of risk and are not suitable for all investors. Investments in cryptocurrencies are relatively new, highly speculative, and may be subject to extreme price volatility, illiquidity, and increased risk of loss, including your entire investment in the fund. Spot markets on which cryptocurrencies trade are relatively new and largely unregulated, and therefore, may be more exposed to fraud and security breaches than established, regulated exchanges for other financial assets or instruments. Some cryptocurrency-related products use futures contracts to attempt to duplicate the performance of an investment in cryptocurrency, which may result in unpredictable pricing, higher transaction costs, and performance that fails to track the price of the reference cryptocurrency as intended. Please read more about risks of trading cryptocurrency futures here.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

© Charles Schwab

Read more commentaries by Charles Schwab