Passive investing has dominated flows for years. But if market history teaches us anything, it’s that the pendulum never swings in one direction forever. So what clues might we miss about the next potential reversal?

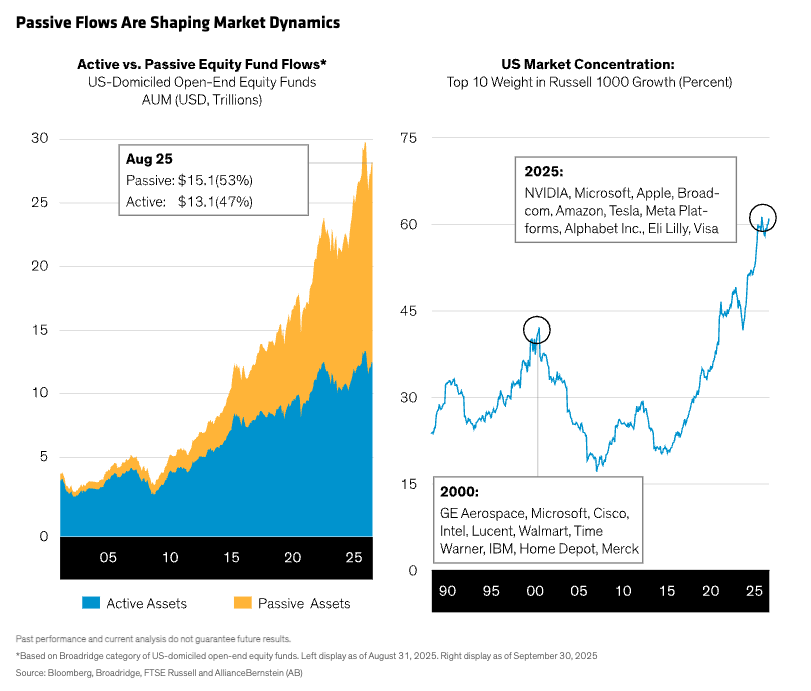

Current market conditions seem self-reinforcing. US stock markets continue to be driven by technology giants amid enthusiasm about artificial intelligence (AI). As passive funds grab more market share (Display), they’re forced to keep buying the mega-caps, which further inflates their share prices and fuels market concentration. By the end of September, the top 10 companies in the Russell 1000 Growth accounted for 61% of its market capitalization. Extreme concentration even prompted FTSE Russell to introduce new rules capping the largest weights of its US equity indices earlier this year.

High concentration makes it hard for diversified active portfolios to outperform. While the mega-caps include great businesses, active strategies may avoid or underweight popular stocks over concerns about valuations, business models and interrelated risks, or because of regulations on weighting individual holdings. To some, this looks like a perpetual loop that could constrain active portfolios indefinitely.

A Brief History of Passive Reversals

We don’t think so—with market history as our guide.

Consistent outperformance of the top stocks isn’t set in stone. Earlier this year, from January through early April, five of the Magnificent Seven mega-caps trailed the market, and throughout the year, their performance has diverged. Rewind to 2022, and we saw the US tech giants fall precipitously in a bear market.

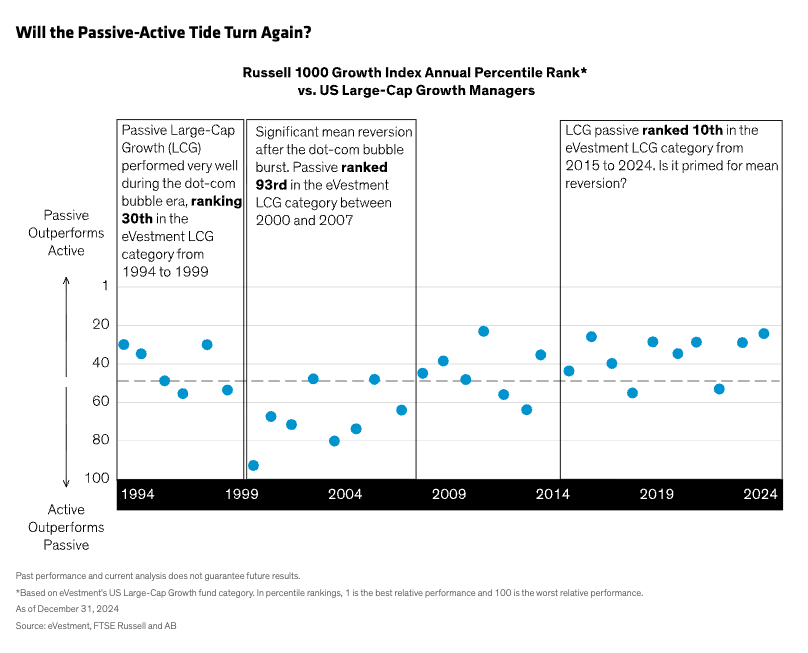

Further back, long periods of passive outperformance eventually reversed. From 1994 to 1999, as the dot-com bubble inflated, passive US large-cap growth portfolios performed especially well, at times outperforming 70% of active peers (Display). This occurred even though passive investments represented a much smaller piece of the market than today. When the dot-com bubble burst, active portfolios outpaced passive performance for most of the next eight years.

The trigger for that reversal was a fundamental mismatch between valuations and earnings. Investors paid up for both highly profitable technology companies and for those with dubious business models that had little to no revenue or profit potential, until a sober focus on fundamentals reversed many of the enthusiastic gains.

Those lessons are still relevant despite some differences to today’s AI-driven market dynamics. For example, in the dot-com bubble, the early internet infrastructure boom was fueled by debt financing for vast fiber-optic networks, which remained largely unused at the time. Today, AI infrastructure is being built to satisfy real, immediate demand.

Yet there are similarities, too. Today’s hyperscalers—tech giants that operate massive data centers and cloud platforms—have doubled capital spending versus current revenue, echoing the capex intensity of the late 1990s’ internet boom. Meanwhile, several zero-revenue energy companies have multibillion dollar market caps—driven by anticipated AI energy demand. Capex cycles tend to peak—along with associated company valuations—no matter how sharp or benign the subsequent fall in spending.

Questioning the AI Spending Boom

For now, the market is rewarding AI infrastructure providers for spending on the data center build-out. It’s not just hype, because the narrow market performance is partially explained by the capex cycle’s contribution to GDP. But we must ask whether these trends can be sustained.

Continued parabolic spending intention rests on two critical assumptions: 1) AI training will continue to scale with increased compute to achieve artificial general intelligence. 2) AI inference will generate sufficient revenues to support the capital build-out in years to come. A challenge to either assumption that even just slows capital spending could “burst the bubble” and drag down stocks. Given the fragility of market concentration that has coalesced around the AI narrative, the potential for a cascading correction is real.

In other words, if assumptions supporting the spending levels or even its frenetic pace prove too rosy, the resulting disappointment could undermine the dominance of the US mega-caps, which now constitute a historically large percentage of passive portfolios. If that happens, we expect passive outperformance to wane as we’ve seen in previous unwinds of concentrated markets, where top index constituents reprice lower and performance broadens to other previously neglected corners of the market. Mean reversion often follows momentum moves.

What Can Active Investors Do?

Since it’s nearly impossible to time market inflection points—and staying invested is paramount to long-term success—we think active portfolio managers have a strategic role to play.

Regarding the mega-caps, we think active managers should own prudent weights in select companies with valuations that are justified by their long-term earnings potential. Not owning market weights might cost some relative performance in the short term. But chasing huge benchmark weights is a risky strategy, in our view. If the mega-caps are punished in a correction, thoughtful positioning away from the crowding will help cushion portfolios.

Disciplined investors should also look beyond the current “picks and shovels” phase of the AI boom, which eventually will end, just as in the dot-com era. Many of today’s technology leaders didn’t directly challenge the early internet leaders back in 2000; they only became major players years later. Similarly, we think that the true, long-term AI market leaders have not yet emerged. The promising task at hand is to identify AI adopters that will apply the technology to generate sustainable productivity and profitability gains. Companies like these offer long-term alpha potential, regardless of how the infrastructure build-out evolves.

Amid the AI exuberance, don’t lose sight of high-quality companies across the market that aren’t being rewarded today. In sectors ranging from healthcare to consumer discretionary to financials, we’re finding stocks with strong fundamentals, resilient business models and attractive long-term return potential waiting to be unlocked when the market broadens. Ultimately, investors who look beyond the obvious, question prevailing narratives and actively prepare for a long investment journey will be well placed to be rewarded when the market pendulum shifts direction.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein