Emerging markets (EM) have arguably proved to be the biggest surprise of 2025 in financial markets, with local currency EM government bonds surging by some 16% and EM dollar-denominated debt up 12%, far outpacing gains of just 3% for global fixed income overall.1 The outperformance is particularly striking as it comes after a “lost decade” of disappointments, during which investors began to question whether emerging markets should even be considered a mainstream asset class.

The strong performance of EM debt stems from several fundamental trends. According to our research, returns from the asset class hinge on five key factors: the direction of interest rates, the strength of the US dollar, global trading conditions, commodities prices, and economic growth in China. Four of these factors are now positive – creating the most favourable conditions for EM bonds in two decades.

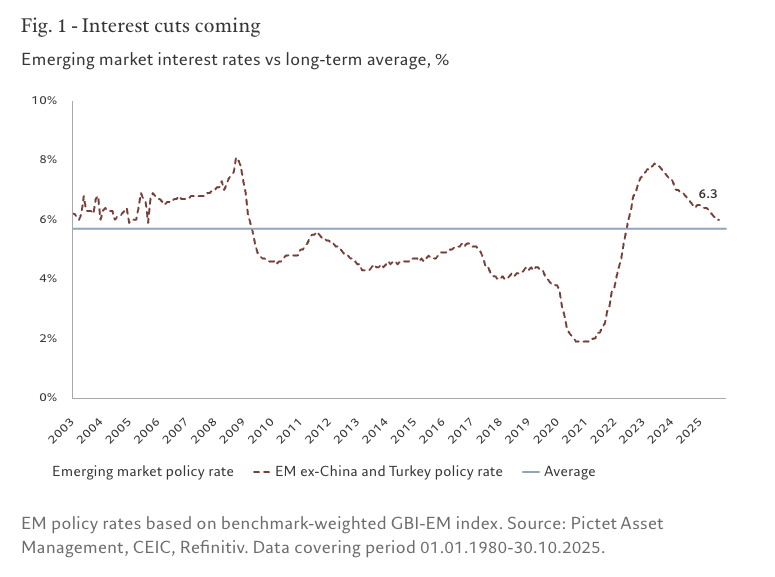

1. Monetary policy is easing

Central bank policy in the emerging world is restrictive but normalising – a generally favourable combination for EM bonds. Although the weighted-average central bank policy rate has dropped to 6.3% – the lowest since the 2003-2008 period – it is still well above our estimated neutral rate of around 5.5% (see Fig. 1). With economic growth running close to potential (at around 4%) and inflation returning to 3%, we expect a continued normalisation of monetary policy, which augurs well for bonds. What is more, average real interest rates (adjusted for inflation) are above 3%, a level historically associated with periods of strong EM performance.

2. Ongoing dollar weakness

The dollar is down 9% since the start of the year against a trade-weighted basket of currencies – weakness which we expect to continue in the face of both cyclical and structural pressures. US growth is slowing, the US Federal Reserve is cutting rates and risk premia are compressing. Structural trends are also weakening the dollar.

As we discussed in our Secular Outlook, the world is moving away from a US-dominated system to a multi-polar one, with the US dollar losing some of its dominance. Since 2014, the dollar’s share in global foreign exchange reserves has dropped to 58% from 66%, as the weaponisation of US assets has dented their appeal, prompting some countries – particularly those in the developing world – to look for alternatives. Economic sanctions and US threats to suspend economies from the SWIFT payment system have made dollar reserves much less safe than in the past. US President Donald Trump’s recent policies have only exacerbated this trend due to threats of taxes on foreign assets, wider US budget deficits, and his administrations openly hostile rhetoric toward the independence of domestic institutions (including the Fed).

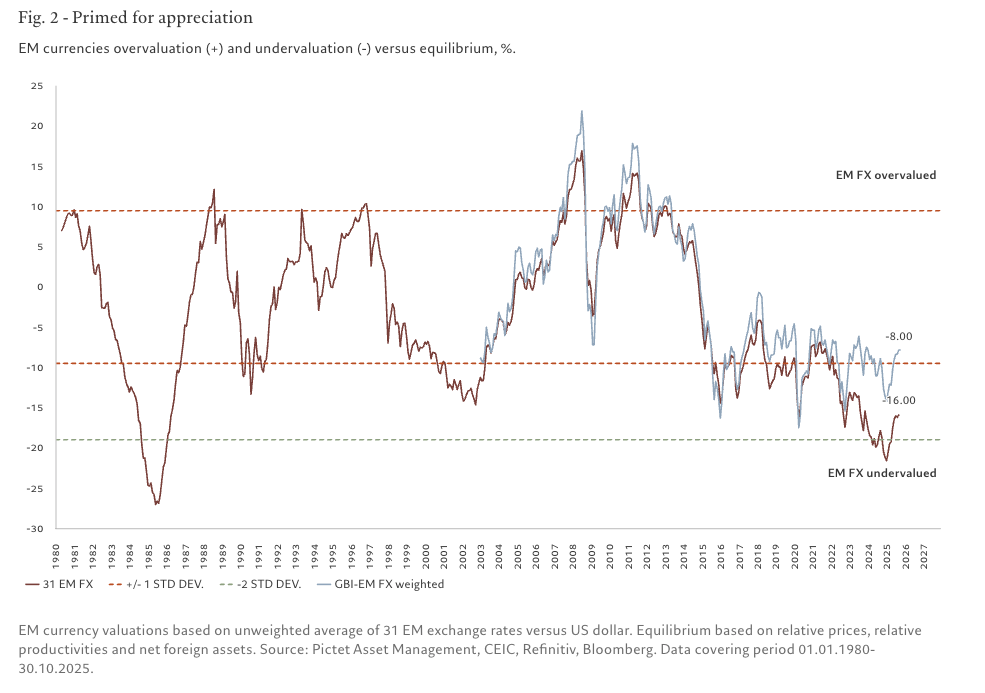

Against this backdrop of economic populism and institutional instability, the dollar’s valuation is arguably still too high: according to our analysis it trades nearly two standard deviations above its fundamental value, while emerging market currencies remain undervalued by 8% to 11% (see Fig. 2). Further depreciation, therefore, seems likely – to the benefit of EM assets.

3. Global trade holds up in the face of US tariffs

Tariffs and geopolitical sabre-rattling have cast a shadow over the prospects for international trade. But, so far, those concerns have proved unfounded, with global exports exceeding pre-pandemic levels. That is in part because US imports account for only 13% of global trade – not enough to dictate the overall trend. With average US tariffs having increased to 18%, we would expect US import volumes to drop by just 2 percentage points.

That drop is even less significant in the face of increasing trade between emerging markets – some 46% of EM exports now go to fellow developing countries, up from 23% in 2000. Just as encouraging is the fact that the number of free trade agreements continues to rise, led by the European Union, which recently signed agreements with Indonesia and currently negotiating pacts with India, South America’s Mercosur trade bloc, and several Southeast Asian countries. Global trade is, therefore, reshaping rather than retreating.

4. Commodities recovering

Commodity prices are rebounding, up about 5% year-on-year, driven by precious and industrial metals. This trend is supported by a weaker dollar, the recovery of the global manufacturing sector, and the energy transition (with copper, for example, in high demand for everything from solar panels to electric vehicles). Extensive investment in energy- and metal-intensive infrastructure to support the boom in artificial intelligence further reinforces this trend.

For commodity exporters, many of which in the emerging world, the environment is doubly favourable: rising prices improve terms of trade, while economic diversification efforts in the Gulf (Saudi Arabia, UAE) reduce dependence on oil and the macroeconomic volatility inherent in less diversified economies.

5. China – the one fly in the ointment

China is the only one of our five factors which is neutral rather than positive for EM bonds, although here too there are some grounds for optimism. The Chinese economy is normalising after a strong first half of the year. Industrial investment is slowing, but this deceleration is intentional, with so-called "anti-involution" policies aiming to reduce overcapacity and restore corporate profitability.

While the immediate impact is slower growth, the medium-term benefits are tangible: an economy which is less dependent on subsidies, as well as one which potentially commands higher wages – and thus high prices.

This change, however modest, would provide relief to the margins of South Korean manufacturers and other Asian economies exposed to Chinese competition, with a positive ripple effect on global markets. Moreover, China’s economy should benefit from fiscal support for households, with some measures already announced and others hinted at by the latest Five Year Plan.

Emerging markets are thus coming out of a long purgatory. Their recent outperformance is not a technical rebound but a reflection of a deeper dynamic shift. This may mark the beginning of a new regime, where emerging markets cease to be a mere reflection of the developed world and once again become its driving force.

1. JP Morgan Global Bond Index-Emerging Markets (GBI-EM), Emerging Markets Bond Index (EMBI), Global Bond Index (GBI) As of 30.10.2025.

2. Calculated as nominal policy rate minus CPI inflation, GBI-EM benchmark weighted.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services. The information used in the preparation of this document is based upon sources believed to be reliable, but no representation or warranty is given as to the accuracy or completeness of those sources. Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management. Pictet Asset Management has not ensured the suitability of the securities mentioned in this document for any specific investor, and it should not be relied upon as a substitute for independent judgment; investors are advised to determine the suitability of the investment based on their financial knowledge, experience, goals and situation, or to seek specific advice from an industry professional before making any investment decisions. Investors should read the prospectus or offering memorandum before investing in any Pictet managed funds. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Past performance is not a guide to future performance. The value of investments and the income from them can fall as well as rise and is not guaranteed. Investors may not get back the amount originally invested.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Pictet Asset Management

Read more commentaries by Pictet Asset Management