Financial Planning vs. Wealth Planning: When Your Plan Must Evolve

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhy Financial Planning Works, Until It Doesn’t

Financial planning helps families organize, save, and invest intentionally. It turns goals into a roadmap, budgeting for major purchases, setting aside for retirement, and aligning investments with life milestones. But at some point, the question shifts from how to grow wealth to how to protect and structure it.

That’s where wealth planning begins. As assets expand, so do the complexities – multiple income streams, family entities, tax exposure, and intergenerational goals. What worked at $1 million in assets rarely works at $10 million. Without structure, opportunity turns to inefficiency.

At Defiant Capital Group, we help high-net-worth families and business owners bridge that transition. We integrate investment management, estate planning, and tax strategy into one cohesive plan that protects and amplifies what you’ve built.

What Is Financial Planning?

Financial planning is the foundation of wealth creation. It helps individuals and families budget effectively, save systematically, invest strategically, and prepare for retirement.

Most households start here. The focus is on accumulation – maximizing contributions, balancing growth and safety, and keeping spending aligned with goals. Key areas include:

- Budgeting and cash-flow management

- Investment selection and asset allocation

- Retirement savings (401(k), IRA, Roth strategies)

- Insurance coverage and debt management

- Education funding and goal-based investing

Financial planning is typically ideal for households building wealth. It emphasizes progress toward milestones rather than preservation across generations. Advisors in this space help clients manage income, reduce expenses, and stay disciplined through market cycles.

However, as wealth compounds and family dynamics evolve, purely goal-based planning starts to break down. Once a family’s financial ecosystem includes multiple entities, real estate holdings, trusts, or business interests, a broader strategy becomes essential.

What Is Wealth Planning?

Wealth planning is the next phase – a more integrated, strategic discipline that unites all aspects of a family’s financial life. It’s not about budgeting; it’s about coordination, structure, and legacy.

A wealth plan connects:

- Investment portfolios with entity structures

- Tax optimization with estate and trust design

- Business ownership with succession strategy

- Family goals with governance and education

In short, wealth planning is comprehensive financial planning for families who already have wealth, not those still building it. The emphasis shifts from earning more to keeping more, from short-term goals to multi-generational outcomes.

For most affluent families, this evolution happens naturally as complexity grows. What starts as a simple portfolio review eventually requires coordination among advisors, CPAs, and attorneys, each working toward one cohesive outcome.

Key Areas Where Wealth Planning Diverges

While both financial planning and wealth planning aim to align money with purpose, their methods differ dramatically once wealth reaches a certain level of sophistication. Below are six areas where the approach fundamentally changes.

1. Time Horizon and Liquidity Buckets

In wealth planning, we segment cash flow into distinct “buckets”: short, medium, and long-term. This allows us to manage liquidity across generations. The strategy accounts for current spending, investment liquidity, philanthropic intent, and future estate needs.

This allows families to maintain stability even when markets fluctuate or liquidity events are delayed.

2. Tax and Entity Structuring

A cornerstone of advanced wealth management is tax optimization through structure. High-net-worth families often use entities such as family LLCs, irrevocable trusts, and grantor retained annuity trusts (GRATs) to minimize tax exposure and control distributions. And for those families with family businesses this also entails tax liability optimization – QSBS stacking, succession planning, and optimizing business ownership for transfer to the next generation.

For example:

- A Spousal Lifetime Access Trust (SLAT) allows one spouse to transfer assets while maintaining indirect access to them.

- An Intentionally Defective Grantor Trust (IDGT) separates income and estate taxation for long-term efficiency.

- A Crummey trust enables annual exclusion gifting while preserving control over timing and use of funds.

Each tool serves a purpose, tax reduction, asset protection, or intergenerational transfer, and must be designed cohesively, not in isolation.

3. Asset Protection and Risk Mitigation

As wealth increases, so does exposure to lawsuits, creditors, and even family disputes.

A robust wealth plan implements asset protection strategies that shield personal and business assets through layered ownership, trust design, and insurance.

Common examples include:

- Separating operating companies from holding entities

- Using limited partnerships to restrict liability

- Structuring personal residences under protective vehicles

- Maintaining umbrella and key-person insurance coverage

Protection is not about secrecy; it’s about resilience. The goal is to ensure wealth survives uncertainty.

4. Family Governance and Legacy Planning

Financial capital only endures when paired with human and intellectual capital. Wealth planning incorporates family governance, which includes the policies, education, and communication structures that guide how wealth is managed, shared, and passed down.

This may include:

- Family meetings or mission statements

- Investment and philanthropy committees

- Education for heirs on stewardship and responsibility

Without clear governance, even well-structured estates can erode through poor communication or lack of shared purpose.

5. Business and Succession Coordination

For entrepreneurs, the business is often the largest single asset and the most emotionally charged. Wealth planning integrates succession planning, ensuring leadership, liquidity, and tax strategy align with both business and family goals.

Key considerations include:

- Valuation and buy-sell agreements

- Gifting or sale of ownership interests

- Management training and leadership continuity

- Liquidity for taxes and estate equalization

By designing succession and wealth planning together, families can control the pace and structure of a transition while preserving enterprise value. For more information see our post about what business owners get wrong about succession planning.

6. Tax Liability Optimization

True wealth planning looks forward and is about managing not just current taxes, but future exposure at both personal and estate levels.

Strategies may involve:

- Coordinating charitable giving through donor-advised funds or charitable remainder trusts

- Harvesting gains and losses strategically

- Using trusts and entities to shift appreciation out of the estate

- Balancing federal, state, and future estate tax implications

This proactive approach transforms taxes from a year-end event into an ongoing design process, and is a defining difference between financial and wealth planning.

When to Transition to Wealth Planning

Many clients realize the need for wealth planning only after a major change such as a liquidity event, inheritance, or business sale. But ideally, the transition should start earlier, once complexity increases and multiple advisors are involved.

You may be ready for wealth planning if:

- Your net worth exceeds $5 million

- You own multiple entities or real estate holdings

- You expect a liquidity event in the next 3–5 years

- You’ve established trusts or charitable vehicles

- You’re preparing to transfer wealth to the next generation

- You own and operate a family business

The earlier this shift happens, the more opportunities exist to align taxes, investments, and estate design before problems emerge.

At Defiant Capital Group, we often begin with a comprehensive wealth audit (i.e. an evaluation of current structures, tax exposure, investment allocations, and governance gaps) to identify where coordination can create efficiency.

Common Pitfalls of Staying in Financial Planning Mode

Remaining in traditional financial planning once complexity rises can lead to missed opportunities and unnecessary risk.

1. Fragmented Advice

Different advisors working independently can create overlap or conflicting strategies. Your CPA may focus on minimizing taxes, while your investment advisor prioritizes short-term returns, and your attorney designs trusts without considering liquidity.

2. Generic Investment Portfolios

Model portfolios built for accumulation rarely account for tax efficiency, estate exposure, or entity ownership. For affluent families, this disconnect can quietly erode after-tax performance over time.

In addition, with significant wealth comes the ability to invest into alternative investments like private real estate funds, private equity, etc. While these funds do bring additional complexity (i.e. you will need to get K-1s for tax returns), they also provide the ability for greater investment tax control, income blocking, depreciation pass-thru, etc.

3. Liquidity Mismanagement

Without a coordinated plan, families may find themselves asset-rich but cash-poor. Wealth is only helpful if it can be used, and without planning families may be unable to access capital for taxes, philanthropy, or investment opportunities.

4. Outdated Estate Documents

Many families rely on estate plans drafted years ago under older tax laws. As exemptions, valuations, and family circumstances change, these documents can become liabilities rather than safeguards. Staying ahead of changes to estate laws can be the difference between paying millions in estate tax and passing on assets tax-free.

5. Neglecting Family Education

Wealth transitions often fail not from taxes or markets, but from unprepared heirs. Ignoring education and communication creates avoidable friction and risk.

In short, staying in financial planning mode too long can cost far more than upgrading to a wealth plan.

How Defiant Capital Group Bridges the Gap

At Defiant Capital Group, we design and execute integrated wealth plans that connect your personal, business, and generational goals under one cohesive framework.

Our approach brings together:

- Investment management built around after-tax outcomes and liquidity goals

- Estate and trust planning that preserves control and minimizes future taxes

- Business advisory and succession strategy for owners planning transitions

- Family governance and education to ensure continuity across generations

We collaborate directly with your CPA, attorney, and other professionals to align every moving piece from tax elections to investment implementation. The result is a unified wealth architecture that evolves with your family and your assets.

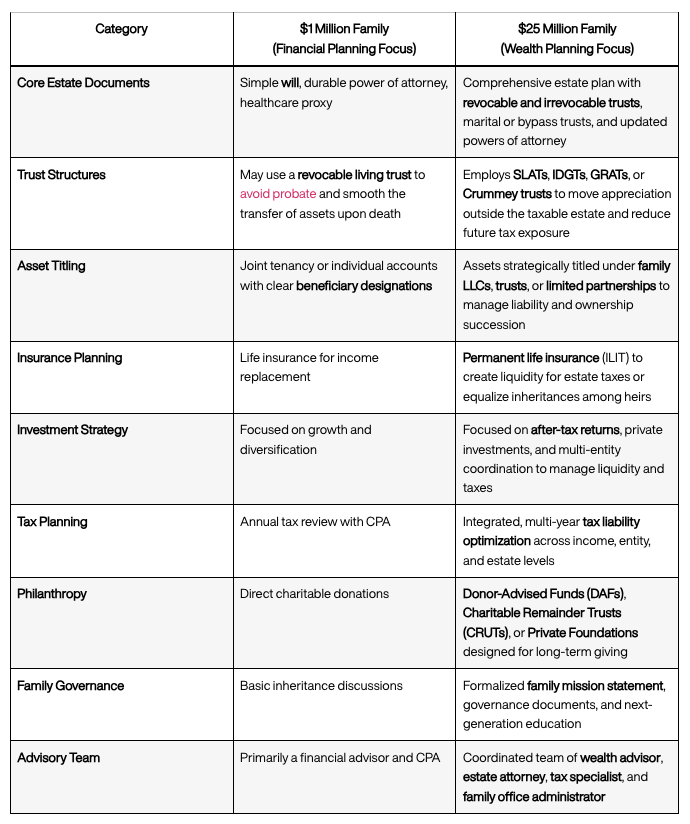

Example: How Estate Planning Evolves with Wealth

Not every family’s financial plan eventually grows into a wealth plan. However, for those families that are growing their wealth the shift starts to occur as the compounding of wealth over $1mn accelerates.

In the example below, we highlight how to recognize when that shift should happen by comparing what’s appropriate for a family with around $1 million in net worth versus one with $25 million or more.

The takeaway:

As wealth grows, so does the need for structure. The $1 million family focuses on protection and accumulation. The $25 million family focuses on preservation, transfer, and coordination. The planning tools evolve, but the purpose stays the same – to ensure wealth supports life, family, and legacy goals for decades to come.

Conclusion: Building and Preserving Wealth with Purpose

The evolution from financial planning to wealth planning isn’t just about scale – it’s about sophistication. It’s the shift from managing money to managing impact, structure, and legacy.

At Defiant Capital Group, we help clients move beyond spreadsheets to strategy to connecting investments, entities, taxes, and estate design under one plan that endures.

If you’re ready to evolve your financial strategy into a cohesive wealth plan, Request an Introduction with our team to help you map the path forward.

Frequently Asked Questions

What’s the biggest difference between financial planning and wealth planning?

Financial planning focuses on personal budgeting, savings, and retirement goals. Wealth planning manages a complex ecosystem of assets, taxes, and entities to sustain and transfer wealth across generations.

At what net worth does wealth planning make sense?

While every situation differs, most families begin wealth planning once their net worth reaches $5–10 million, or when tax liabilities, business ownership, multiple entities, or trusts introduce complexity.

Do I need a separate advisor for wealth planning?

Not necessarily. What matters is whether your advisor integrates investment management with tax, estate, and entity design. Defiant Capital Group provides all three within a single fiduciary framework.

What’s the role of trusts in wealth planning?

Trusts such as SLATs, IDGTs, and GRATs are central to managing estate taxes, protecting assets, and defining distribution control. They allow assets to grow outside your taxable estate while maintaining flexibility for beneficiaries.

When should I start transitioning to wealth planning?

Ideally before major events such as business sales, liquidity events, or intergenerational transfers. Early planning ensures your structure, tax strategy, and governance evolve in sync.

How often should a wealth plan be updated?

A wealth plan is a living document that should be updated regularly. At a minimum you should review it annually or after any major life or financial event. Regular updates keep documents, entities, and tax strategies aligned with new laws and goals.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Please read important disclosures here.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All