Monthly Market Update

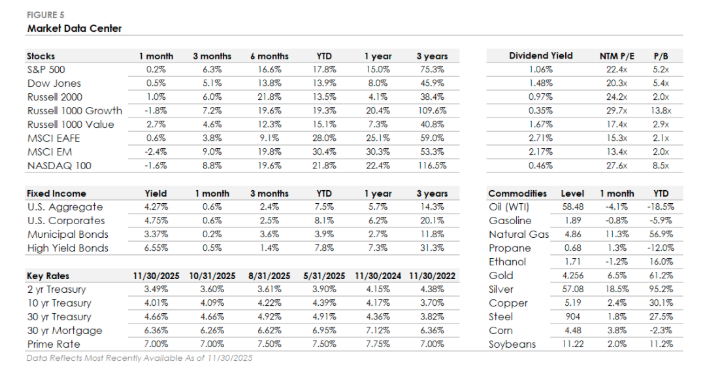

- Stocks: The S&P 500 increased 0.2% in November, marking a seventh straight monthly gain, but headline strength masked notable underperformance from mega cap growth.

- Leadership Change: Large cap value gained 2.7 % while large cap growth declined 1.8%, and small caps and the Dow outperformed as markets rotated away from the most crowded tech and AI trades.

- Sectors: Healthcare led all S&P 500 sectors with a gain of more than 9%. Eight of eleven sectors beat the index, while technology, consumer discretionary, and industrials traded lower as investors questioned rich AI valuations

- International Stocks: Developed markets stocks gained about 0.6 percent and modestly outpaced the S&P 500, while emerging markets fell roughly 2.4 percent, though both regions still lead the S&P by more than 10 percent year to date.

- Bonds: Core bonds advanced as Treasury yields moved lower into month end. The U.S. Aggregate Bond Index returning 0.6% in November, lifting its year-to-date gain to 7.5%.

The Fed, December Odds, and a Choppy November

November’s volatility was driven less by earnings and more by the market’s tug of war with the Federal Reserve. After the late October meeting, Chair Powell pushed back on the idea that another December rate cut was a foregone conclusion, even as the Fed delivered a second consecutive 0.25% cut and announced it would end balance sheet runoff effective December 1st. Market implied odds for a third cut slid from near certainty in late October to roughly 40% by mid November as multiple Fed officials questioned the need to move again so soon.

That shift in expectations weighed on risk assets, with the S&P 500 pulling back and ultimately bottoming on November 20th. However, markets rebounded before month-end as softer labor data and cooler inflation prints pushed December cut odds back above 80%. Beneath the surface, leadership rotated toward Health Care, value, and small caps while earlier AI heavy winners lagged.

For now, investors are treating a potential December cut as a key signal for soft-landing momentum and a more durable easing cycle. Policymakers continue to emphasize that future moves will depend on the data, not on market pricing. In our view, this is a time to use rate volatility to improve portfolio quality, duration, and tax positioning rather than making binary bets on a single Fed meeting.

AI Momentum Slows as Selectivity Increases

AI remains one of the most powerful theme driving markets, but November showed even the AI trade has limits. The largest S&P 500 names, many tied directly to AI infrastructure and data center buildouts, have dominated returns throughout 2025. That leadership weakened as investors questioned valuations, profitability timelines, and capital intensity. Some widely held AI names saw meaningful pullbacks during the month, and the shift toward value and Healthcare underscored the growing dispersion.

In our view this is not a reversal of the AI trend, but instead a reflection of a more mature stage. Investors are beginning to distinguish between companies with visible cash flow leverage from AI, and those priced on narratives alone. The market is rewarding businesses with durable demand and penalizing those relying on aggressive spending or debt supported expansion without clear returns.

We expect the next phase of the AI cycle will require greater selectivity. Portfolios benefit from exposure to innovation, but they should not rely on a narrow set of winners. Headed into ’26 concentration risk remains one of the most important issues to manage and control.

A Cautious Setup Into Year End

The backdrop heading into year-end is mixed. Falling yields and easing inflation support a constructive environment, and seasonal strength historically benefits both stocks and bonds in November and December. At the same time, leadership remains narrow and valuations elevated. The Fed path after December is still uncertain, there are early (and growing) signs of private credit stress, and continued softening in labor data.

Volatility will likely remain contained into December (especially around Mag7 and large-cap growth names), but the margin for error is shrinking. Markets are priced for a near perfect combination of slower inflation, steady growth, and continued earnings resilience. That outcome is possible, but not guaranteed.

Before year-end this is a good time to revisit asset allocation, ensure liquidity is appropriate, raise capital for next year, and take advantage of today’s higher yields to reinforce long-term cash flow positioning.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosures

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

A word on risk

All investments carry a certain degree of risk, including possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. This report should not be regarded by the recipients as a substitute for the exercise of their own judgment. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Case Studies

Case studies and examples are hypothetical and do not involve any actual Defiant Capital Group clients.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group