In this article, Russ Koesterich discusses gold’s recent positive correlation with stocks, particularly those names showing strong price momentum.

Key takeaways

- Despite a few challenging days, gold continues its upward climb, reflecting a correlation with momentum themes like early growth that have dominated the market in 2025.

- In light of this, Russ cautions that in the near-term, gold is likely to remain volatile given the momentum trade unwind but still likes the yellow metal as a portfolio diversifier.

For an asset often viewed as a safe-haven, gold has had a wild ride. Starting last fall, gold advanced more than 70% in less than a year as seen on Bloomberg. That stellar run was shattered in mid-October. While there was no obvious catalyst, gold plunged -10% in a matter of days before recovering half the losses by November 12th.

I last discussed gold in late August. At the time, I highlighted the potential for upcoming seasonal volatility and gold’s history of outperforming stocks when vol spikes. While gold did indeed surge 25% from the end of August through the October peak, it was not for the reasons I cited. In fact, it was exactly the opposite of the scenario I highlighted.

Except for one bad day in early October 2025, the seasonal surge in equity volatility, as measured by the VIX, never arrived. Instead, markets rallied in September and October, with a modest pullback not arriving until early November. And gold? Rather than providing any diversification benefit, gold tended to follow equities.

While there is no fundamental reason gold should trade with the stock market, increasingly there is a technical one: gold has become another manifestation of the momentum trade, i.e. investors chasing whatever has gone up the most.

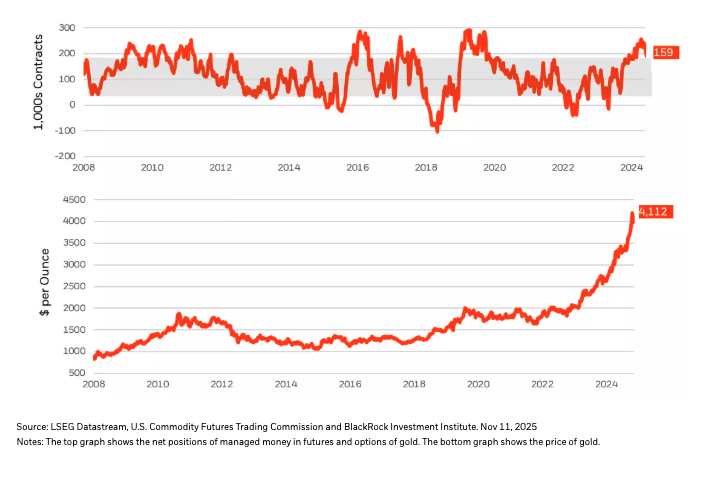

Most recently, when looking at correlation on Bloomberg year to date, gold has had a slight positive correlation with stocks as measured by the MSCI ACWI index. That correlation rises significantly when comparing gold to stocks with one specific characteristic: price momentum. In other words, gold has been swept up with early growth and other thematic trades that dominated markets through much of the fall. And as with many of these trades, gold benefited as investors indiscriminately piled into the trade (see Chart 1). But when the trade hit a wall back in October, gold sold off hard along with other momentum themes, such as early growth stocks.

Chart 1

Gold futures positioning

Long-term thesis has not changed

What to expect going forward? We believe near-term gold is likely to remain volatile as the momentum trade continues to unwind. That said, the long-term rationale for holding gold has not changed.

While gold has proved an unreliable equity hedge it is still a useful offset to a weakening dollar. During the past five years, gold’s correlation with the Dollar Index (DXY) has been consistently negative, at around -0.60 as seen on Bloomberg. To the extent dollar weakness remains a long-term risk, gold is a useful portfolio tool.

Related to the dollar are the concerns surrounding the U.S. fiscal picture, concerns that have not exactly been alleviated during the government shutdown. In the long-term, gold still tracks with government debt, which is still rising at a pace never seen outside of war or recession.1

Gold appears to have temporarily morphed into a momentum trade. While this is likely to create more short-term volatility, I would use weakness to modestly add to positions. Long term, nothing has changed as to why you hold gold in the first place.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month end, please click on the fund tile.

The Morningstar RatingTM for funds, or "star rating", is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure (excluding any applicable sales charges) that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

1BlackRock, Bloomberg. LSEG DataStream. As of November 12, 2025

Russ Koesterich, CFA, is a Portfolio Manager for BlackRock's Global Allocation Fund and Lead Portfolio Manager for BlackRock’s Global Allocation (GA) Selects Model Portfolios and is a regular contributor to Market Insights.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

Commodities' prices may be highly volatile. Prices may be affected by various economic, financial, social and political factors, which may be unpredictable and may have a significant impact on the prices of precious metals. Concentrated investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and the general securities market. A significant portion of the aggregate world gold holdings is owned by governments, central banks and related institutions. One or more of these institutions could sell in amounts large enough to cause a decline in world gold prices. Should there be an increase in the level of hedge activity of gold producing companies, it could cause a decline in world gold prices. Should the speculative community take a negative view towards gold, it could cause a decline in world gold prices.

Principal Risks: The fund is actively managed and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment grade debt securities (high yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities. Asset allocation strategies do not assure profit and do not protect against loss. Short selling entails special risks. If the fund makes short sales in securities that increase in value, the fund will lose value. Any loss on short positions may or may not be offset by investing short sale proceeds in other investments. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility.

There may be less information on the financial condition of municipal issuers than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. Some investors may be subject to federal or state income taxes or the Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of December 2025 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Funds that concentrate investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and the general securities market.

There can be no assurance that performance will be enhanced or risk will be reduced for funds that seek to provide exposure to certain quantitative investment characteristics ("factors"). Exposure to such investment factors may detract from performance in some market environments, perhaps for extended periods. In such circumstances, a fund may seek to maintain exposure to the targeted investment factors and not adjust to target different factors, which could result in losses.

Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2025 BlackRock, Inc or its affiliates. All Rights Reserved. BLACKROCK and iSHARES are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

© BlackRock

Read more commentaries by BlackRock