Multi-Asset Income Outlook: Three Key Questions for 2026

After a turbulent start to 2025 defined by US policy shocks, attention shifted to AI optimism and corporate fundamentals, with earnings and capex intentions often eclipsing traditional data releases. Despite these twists, returns were solid across asset classes. As we look toward 2026, we think the macro backdrop is supportive, though uncertainty remains, with Europe’s fiscal-policy dynamics and US labor trends likely to shape the range of possible outcomes.

We think investors should think about three key questions as the year unfolds:

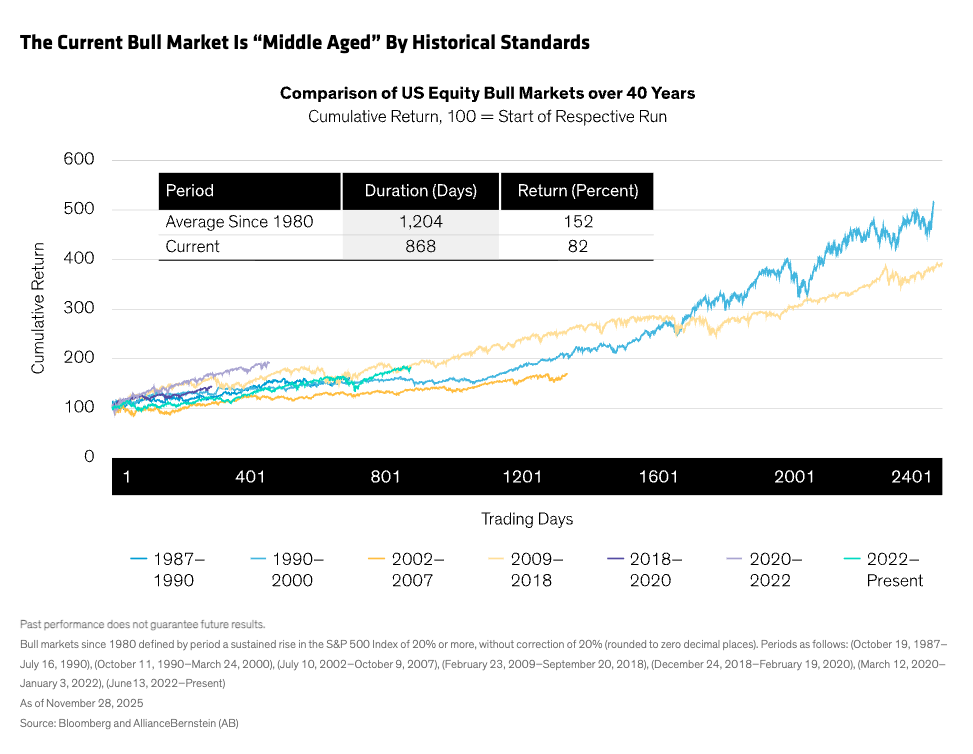

Is the bull market for global stocks nearing its end?

The global equity rally that began after the late-2022 downturn has delivered strong gains, raising the question of whether this bull market is nearing its end. History suggests otherwise: bull markets rarely die of “old age”—they end due to shocks or excesses. By historical standards, we think today’s rally is “middle-aged,” not extreme (Display).

We view the macro backdrop as generally supportive for equity markets, with growth expected to be near-trend next year and the Fed with ample dry powder to ease rates should that come into question. Therefore, we think that there could be some opportunity cost to moving out of equities too soon, but a focus on selectivity to discern between winners and losers is prudent.

Are we in an AI bubble?

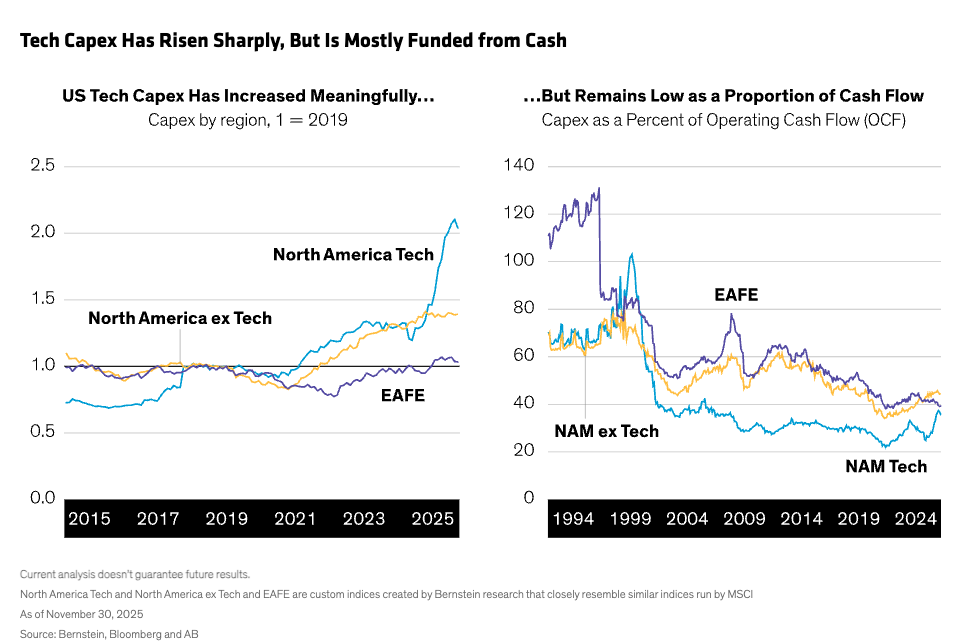

This bull market’s defining feature is its narrow leadership. AI-driven tech stocks have powered extraordinary gains, creating a K-shaped market: a few big winners while many lag. That concentration fuels index returns but introduces fragility. The U.S. economy is asymmetrically exposed: the wealthiest households own most equities and drive consumption—so an AI correction could hit spending and even tip the economy into recession.

For now, though, fundamentals are reassuring, as earnings growth—not just multiple expansions—has driven returns. What’s more, rising capital investment among US tech firms—though eye-wateringly high—is largely funded by strong cash flows rather than debt, but we are closely watching for signs of rising leverage and debt issuance (Display).

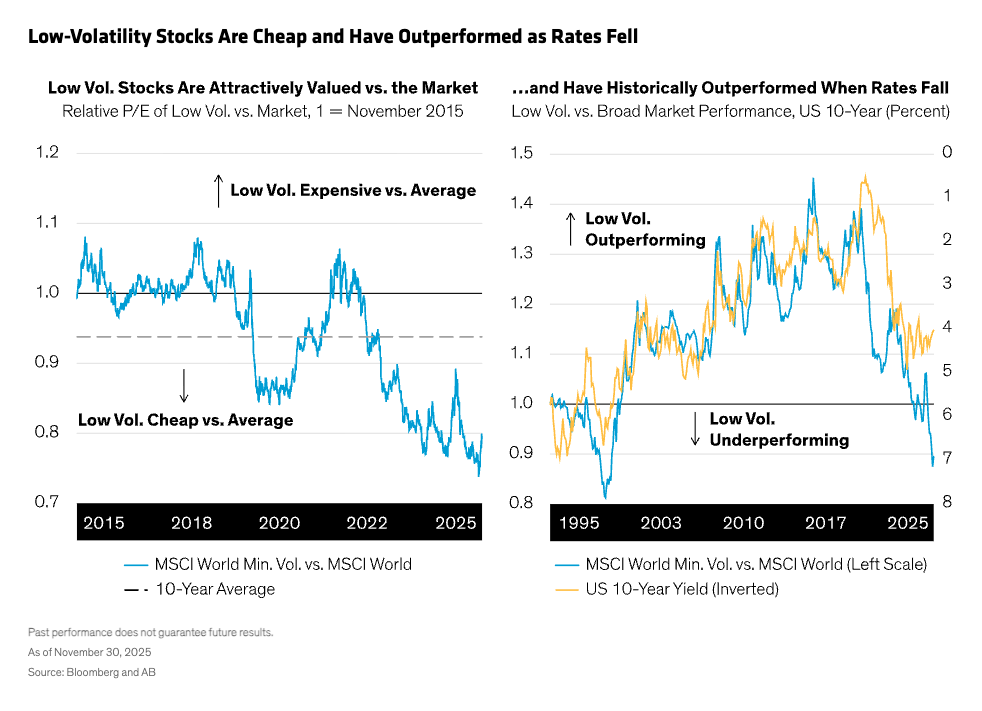

Rich valuations don’t necessarily predicate poor near-term returns, but they do amplify downside risk. We think the narrow market leadership argues for diversification and low-volatility stocks can offer defensive exposure and attractive valuations, with a potential tailwind if yields fall. (Display).

Do recent ‘cracks’ in credit suggest bigger problems?

Recent negative headlines around a handful of issuers have sparked concerns about credit health, but we believe these stresses remain isolated rather than systemic. Broadly speaking, corporate fundamentals seem solid, liquidity conditions look stable and refinancing activity seems manageable. Credit spreads—high yield especially—have been remarkably steady, another positive sign.

Looking ahead to 2026, we believe the backdrop for credit remains supportive, but valuations leave little room for error. Default rates may drift modestly higher from historic lows but should stay relatively contained because most issuers entered this cycle with strong balance sheets. Given where spreads are, high yield offers limited price upside next year, but elevated yields can still drive attractive total returns.

We think the combination of tighter spreads and slower growth means selectivity matters more than ever in the credit space.

The Big Picture: Positioning a Multi-Asset Income Strategy

Within equities, we favor the US for its strong profitability and balance sheet resilience, but diversification is key. Emerging markets remain attractive, trading at a discount to developed peers and supported by lower local rates, improving earnings and a softer dollar. EM also offers alternative exposure to AI, but at more reasonable valuations, particularly in China, Taiwan and South Korea. We also see merit in complementing tech-heavy allocations with defensive strategies such as low-volatility equities, which can provide stability in a risk-off environment.

On the fixed-income side, we’ve been moving up in quality. Investment-grade corporates and BB-rated bonds remain preferred sources of yield, while a more moderate growth backdrop should drive caution on reaching into a lower-quality part of the market. We also like government bonds: they’ve regained their negative correlation with risk assets, offering a potential buffer against equity volatility. We think it makes sense to look to shorter and intermediate maturities, which should benefit from the Fed’s rate-cutting cycle, while leaning away from long-term issues, whose returns could feel the weight of fiscal concerns.

From our perspective, a multi-asset income approach remains well-suited to the current environment, which is supportive but certainly not risk-free. Economic growth should hover near long-term averages, inflation is sticky but down from its peaks and monetary policy is still easing in most regions.

These dynamics support risk assets, yet valuations across equities and credit are undeniably rich, and the range of macro outcomes remains wide. This is precisely the backdrop where multi-asset income solutions can add value: capturing yield and upside while maintaining a disciplined, risk-aware approach.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.