What Gold Reveals About America’s Affordability Crisis

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsA generation ago, a single income could support a family, buy a house and pay for a vehicle or two in the driveway.

Today, even two high earners are struggling to purchase a new home.

According to a recent report from Bankrate, a household earning $80,000 a year is now priced out of 75% of all new homes on the market. A family now needs to earn at least $113,000, and in some major metros, it’s closer to $200,000.

Meanwhile, the homeownership rate has slipped to a six-year low, with further declines expected next year. Families are being squeezed from every angle.

The point I want to make here is that the so-called affordability crisis isn’t just about the cost of homes or other assets. It’s about the cost of money.

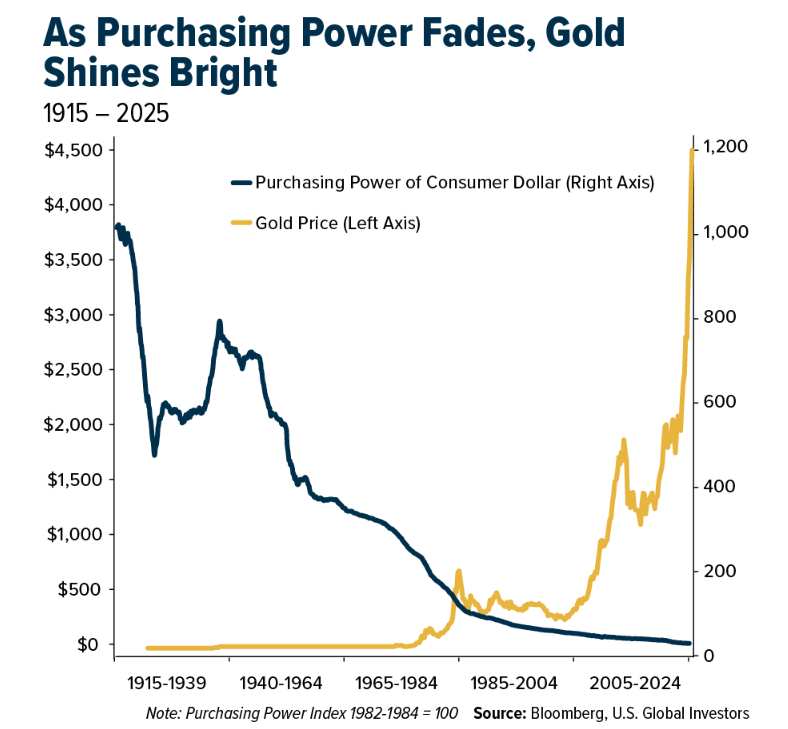

The Dollar Has Been in a Century-Long Bear Market

Take a look at the chart below. It compares the purchasing power of the U.S. dollar since 1915 to the price of gold over the same period.

What it shows is that the greenback has lost over 95% of its purchasing power. Gold, by contrast, has exploded, especially during periods of fiscal and economic strain.

Politicians and pundits may blame greedy corporations or inefficient supply chains, but here’s the truth: when a government runs endless deficits and finances them with fiat created out of thin air, the currency itself becomes the source of the problem.

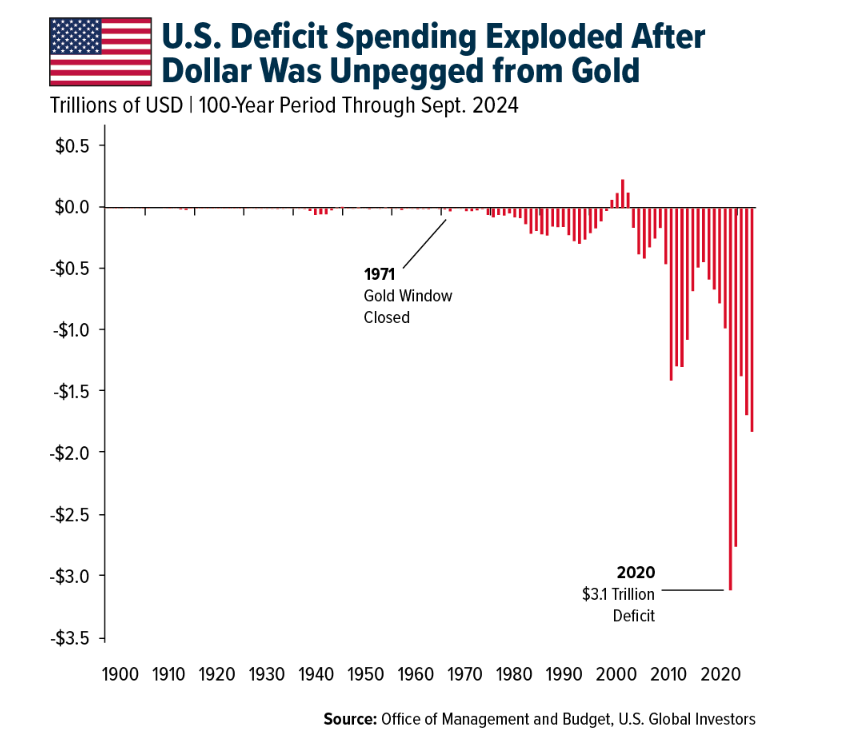

We can trace it all back to 1971 when President Nixon suspended the dollar’s convertibility into gold. As I shared with you before, that was the day the U.S. traded fiscal discipline for a floating exchange rate.

Once the tether to gold was severed, spending exploded. Government debt soared from less than 40% of GDP to well over 120% today.

In short, when money becomes untethered from reality, everything priced in dollars becomes harder to afford.

That takes us back to housing.

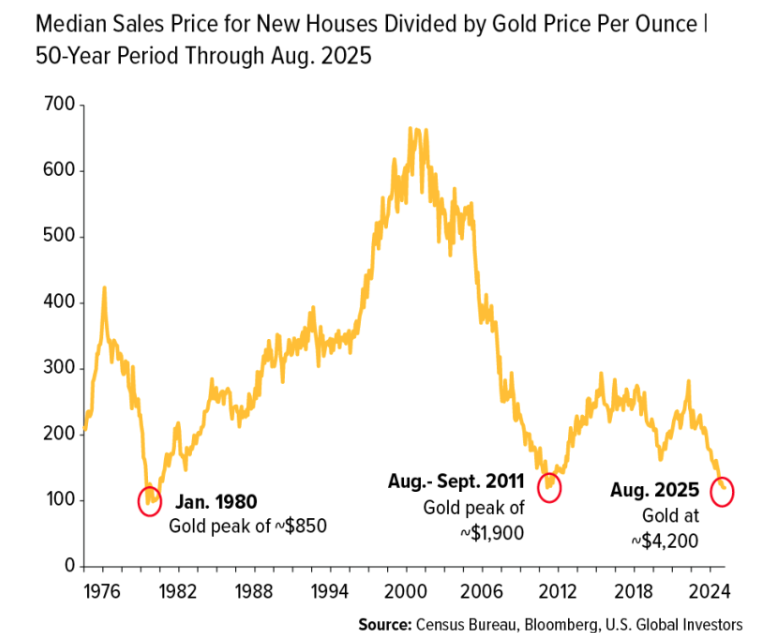

U.S. Housing Looks Historically Cheap… When Priced in Gold

The next chart might surprise you. It shows the ratio of the price of a median new home divided by the price gold. Essentially, it tells you how many ounces of the precious metal it takes to buy a typical American home.

We all know that, in dollar terms, housing is expensive right now. According to the Census Bureau, the median price for a new home in August was $413,500, a nearly 5% jump from the price in July. Remember, that’s the median price, meaning half of all available homes for sale are even more expensive.

But the chart shows housing priced not in dollars but in gold, and you’ll notice three instance when the median home cost roughly 100 ounces: 1980, 2011 and 2025.

This tells me the affordability crisis isn’t necessarily being driven by runaway home prices, but by the continued weakening of the dollar as well as the cost of borrowing.

Examining housing through a gold lens exposes what the consumer price index (CPI) and political messaging hide—namely, the real culprit is the currency.

That’s why I, along with many others, consider gold to be real money. It doesn’t lie, and it doesn’t get revised by government bureaucrats. It doesn’t depend on congressional budget committees or Federal Reserve projections.

Think about that next time you hear about a housing bubble. The real bubble may be the debt-fueled system we’re using to measure value.

The Fiat Era Has Failed to Deliver Price Stability

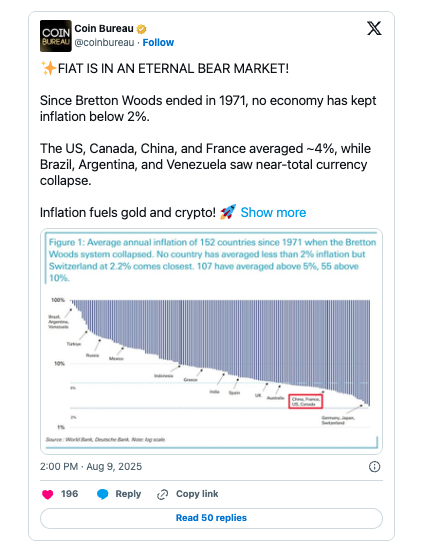

This isn’t just an American problem, of course.

The chart below, taken from a Deutsche Bank report, shows average annual inflation for 152 countries since 1971. Not one major economy has kept inflation below 2% over the past half-century. Most countries have averaged between 4% and 10%, but some—Argentina, Brazil, Turkey—have suffered a “near-total currency collapse,” according to Coin Bureau.

This is what happens when the world shifts from gold-backed money to political money.

What Gold Is Telling Us Right Now

Once again, gold is real money, whereas fiat is temporary. In an era of record national debt, rising inflation and geopolitical uncertainty, I believe it’s prudent and rational to follow the Golden Rule: a 10% weighting in gold—half in bullion, half in high-quality gold mining stocks—rebalanced annually.

This simple strategy has helped preserve wealth across every monetary regime in history, from the Roman Empire to Bretton Woods.

President Donald Trump calls the affordability crisis a hoax. In truth, the lack of affordability is real for many families right now, but the cause isn’t homebuilders or landlords or banks. The cause is the steady erosion of fiat’s purchasing power. Gold is simply the mirror reflecting the truth.

Airlines and Shipping

Strengths

- China’s trade surplus has surged past $1 trillion in 2025. Exports are shifting away from the tariff-hit U.S. market toward booming demand in Europe, Latin America, the Middle East, Africa, and South Asia. Rather than weakening, China’s export engine is being rewired, with container flows rerouted to longer, fast-growing lanes that are reshaping global shipping patterns.

- American Airlines reports that bookings have rebounded strongly after the government shutdown ended, indicating a solid first quarter ahead, even though the carrier took a “substantial” hit during the disruption due to its heavy reliance on domestic travel.

- The best performing airline stock for the week was Grupo Aeroportuario del Pacifico. Shares rose 13.1% after shareholders approved a strategic transaction involving Cross Border Xpress, which improved growth visibility and boosted investor confidence.

Weaknesses

- Ryanair plans to cut 1 million seats, remove five based aircraft, and drop 20 routes from Brussels and Charleroi next winter after Belgium moved to double its aviation tax to €10 per departing passenger, reports Reuters. The airline says the higher taxes and rising airport access costs make Belgium uncompetitive and has urged government officials to reverse the increases.

- Saudi ports handled 649,000 TEUs in November, a 3% year-over-year decline, as both import and export containers fell despite an 8% rise in transshipment activity. Overall cargo volumes and vessel traffic inched higher, but vehicle handling dropped sharply, even as passenger numbers surged 70%.

- The weakest airline stock for the week was Sabre Corp. It declined 7.36% after cutting its full-year financial outlook and flagging ongoing margin and execution pressures, prompting investors to reassess the company’s near-term earnings visibility.

Opportunities

- China COSCO Shipping placed a historic order worth more than RMB 50 billion with China State Shipbuilding Corporation (CSSC) for 87 new vessels covering container ships, bulk carriers, tankers, and specialized transport, reports Maritimes.gr. It is the largest domestic shipbuilding contract ever between Chinese maritime companies and will accelerate COSCO’s fleet renewal across major segments while boosting activity at multiple CSSC yards.

- The IATA expects record airline profits next year despite ongoing supply‑chain delays that forced Airbus to cut 2025 delivery targets and slowed the rollout of new fuel‑efficient jets from both Airbus and Boeing. Confidence is shifting toward Boeing as Airbus faces more setbacks, but the industry will still receive fewer new aircraft than planned.

- Austin is preparing to offer Southwest Airlines a performance‑based incentive package to encourage the carrier to expand at AUS, hire locally, and participate in the city’s new infrastructure academy. The plan could create 2,000 high‑paying jobs and generate nearly $20 million a year in new tax revenue, while Southwest considers competing sites for its growth.

Threats

- The FAA has intensified scrutiny of Boeing’s 777X program over new compliance issues, raising the risk of further certification delays. Any additional slippage would constrain wide-body capacity for airlines already struggling to secure long-haul aircraft.

- Heavy snowfall and limited ground-handling capacity at London Heathrow caused more than 240 flight cancellations and widespread delays over a 48-hour period. The disruption exposed operational vulnerabilities at Europe’s busiest hub and created ripple effects across transatlantic passenger and cargo networks.

- Two attempted drone attacks on tankers transiting the Strait of Hormuz pushed war-risk insurance premiums up by 12–15% this week. Rising security threats in this critical chokepoint increase costs and routing risks for global energy and cargo shipping.

Luxury Goods and International Markets

Strengths

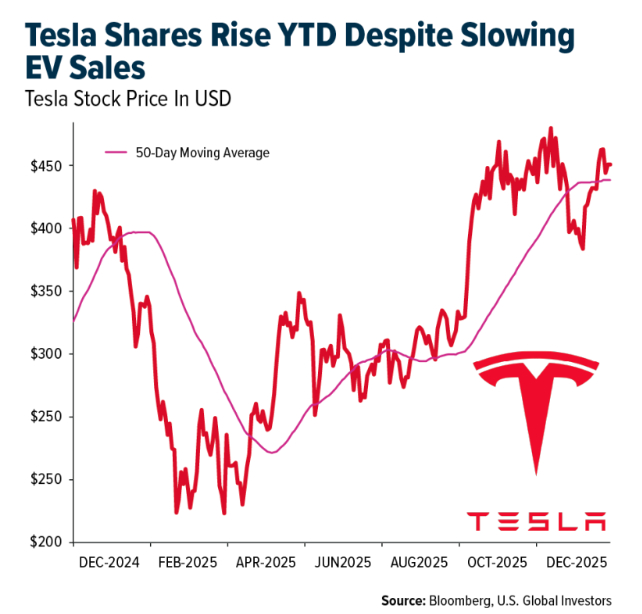

- Tesla shares are up year-to-date despite weaker EV sales. The stock is benefiting from optimism around the company’s robotaxi plans and progress in humanoid robotics. Elon Musk has emphasized that Tesla should be viewed as an AI and robotics company.

- Global stocks gained this week after the Federal Reserve delivered a 25-basis-point rate cut, boosting investor confidence and improving overall risk sentiment. Lower borrowing costs support economic activity and strengthen the outlook for corporate earnings, which helped equity markets rally across the U.S., Europe, and Asia.

- Citychamp Watch & Jewellery, a watch manufacturer and distributor, was the best-performing stock in the luxury index this week, rising 13.2%. The shares recently rebounded after hitting a year-to-date low on November 21, following a decline of more than 70% earlier in the year.

Weaknesses

- Ferrari shares fell 4.1% on Wednesday, hitting their lowest level since January 2024, after Oddo BHF downgraded the stock. The broker cited weakening momentum and structural concerns following Ferrari’s decision to cut deliveries of the F80. This decline came after another downgrade from Morgan Stanley just two days earlier.

- There is ongoing labor unrest at LVMH’s wine and spirits division, where workers have been on strike since early December over canceled year-end bonuses. The continued walkouts at brands such as Moët & Chandon and Veuve Clicquot are causing operational disruptions and highlighting rising cost and employee-relations pressures within the sector. This prolonged unrest risks delaying production, straining supply chains, and weighing on margins for luxury companies already facing softer demand.

- Melco Resorts & Entertainment was the worst-performing stock in the luxury index this week, falling 8%. The decline occurred despite the absence of any significant new company-specific news, suggesting the move was driven by broader market sentiment and investor caution rather than a specific announcement.

Opportunities

- The IMF upgraded China’s GDP growth forecast to 5%, signaling that the country’s economy is performing better than expected. The revision reflects stronger consumer spending, steady manufacturing activity, and continued government support aimed at stabilizing growth. This improved outlook boosts investor confidence and suggests China may play a more supportive role in global economic momentum this year.

- China’s CPI rising by 0.7% presents an opportunity for businesses and investors, as it signals strengthening consumer demand after a long period of soft inflation. This moderate pickup indicates improving confidence and spending power, which can support sales, pricing, and overall economic momentum. If the trend continues, companies with strong exposure to China could benefit from a more stable and recovering market environment.

- According to Bloomberg Intelligence, tourism will help drive luxury goods sales in 2026. International travel, which accounts for about one-third of luxury spending, is expected to grow by 5 to 6% next year. Early signs point to a global pickup in Chinese tourists. Additionally, Hermès, a super-luxury company headquartered in France, noted that U.S. and Middle Eastern visitors remain key spenders.

Threats

- A member of the Hermès family, Nicolas Peuch, is suing the CEO of LVMH over missing Hermès shares valued at roughly €14 billion. Peuch alleges that his former wealth advisor secretly sold the shares to the LVMH CEO without his consent, effectively stripping him of a major portion of his inheritance. The case has drawn significant attention given the longstanding competition between the two luxury groups and the large value of the disputed stake.

- According to Bloomberg’s article “Holiday Spending Shows Effects of an Uneven Economy,” published December 10, 2025, more shoppers, including middle- and higher-income households, are seeking discounts and shifting spending toward value retailers such as Walmart, Dollar General, and Dollar Tree. This reflects rising financial strain and greater price sensitivity, though the top 10% of households continue to spend freely on luxury, helping higher-end retailers like Bloomingdale’s maintain strong sales.

- The U.S. Retail Sales and Consumer Spending report will be released on December 16. This data will show how much consumers are actually spending, and any weaker-than-expected results could raise concerns about slowing demand for big-ticket and discretionary items such as luxury goods. Softer retail activity would reinforce fears of cooling consumer momentum, putting pressure on sentiment across the luxury sector.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was zinc, up about 3.54%. Zinc ended the week higher despite a later week pullback, reflecting broader strength across base metals as tighter supply conditions and improving macro tailwinds supported prices. Its weekly gain mirrors copper’s advance, underscoring how both metals continue to be driven by shared industrial demand drivers, inventory tightness and expectations for stronger global growth.

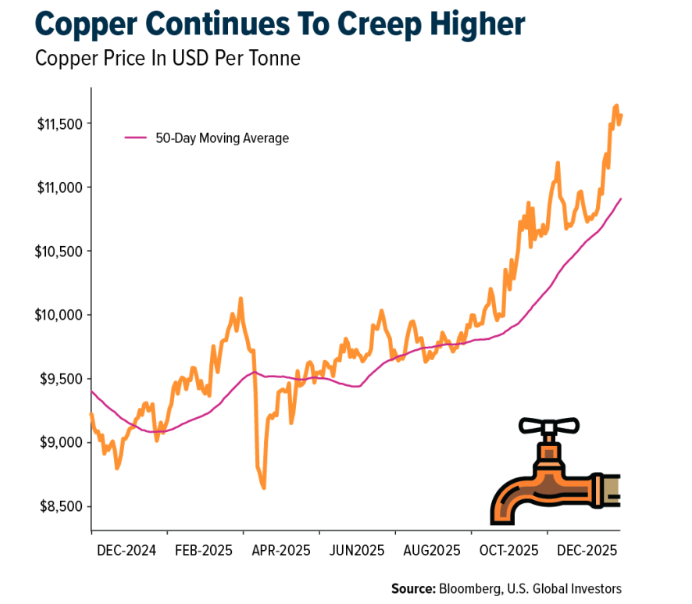

- Copper climbed to a fresh record above $11,290 a ton as mounting supply fears—from mine disruptions to tight concentrate markets—intensified following warnings of potential shortages next year. Traders are rushing shipments to the U.S. ahead of possible 2027 import tariffs, further straining global availability and driving copper nearly 30% higher on the LME this year.

- Orsted A/S and Vestas Wind Systems A/S shares rose significantly, with Orsted reaching a four-month high after a U.S. federal judge overturned President Donald Trump’s executive order banning new wind projects as arbitrary and capricious, though both companies later pared gains amid ongoing regulatory uncertainties. While the ruling supports offshore wind proponents and could face an appeal, analysts remain skeptical of its broader impact given the administration’s oppositional stance, weakened tax incentives and persistent supply-chain challenges in the industry.

Weaknesses

- The worst performing commodity for the week was natural gas, down about 22.08 %. U.S. natural gas prices plunged nearly 8% Monday alone, as warmer mid-December forecasts crushed heating-demand expectations and triggered heavy selling. The decline came despite a bullish storage draw nearly double the five-year average, underscoring how weather-driven sentiment is overwhelming otherwise supportive fundamentals.

- Trafigura Group reported a net income of $2.67 billion for the financial year ending September, a 3% decline from the prior year but bolstered by strong performances in its oil and metals divisions, leading to record earnings in nonferrous metals trading amid supply disruptions and regional shortages. The company increased share buybacks to $2.9 billion, a 43% rise that outpaced profits, while anticipating continued market volatility driven by geopolitics, the energy transition and potential supply gluts in 2026, alongside ongoing reviews of past frauds and asset impairments.

- OPEC+ output fell further below targets in November, underproducing quotas by roughly 419,000 bpd as several members struggled to raise supply despite higher ceilings. The shortfall — led by deeper Russian underproduction and uneven compliance from Kazakhstan and Iraq — comes even as the group unwinds cuts, adding uncertainty to an oil market that BNEF expects to move into surplus through 2025–26.

Opportunities

- Poland is positioning itself to become Central and Eastern Europe’s primary LNG gateway as the region phases out Russian gas, evaluating a third Baltic import terminal that would leverage its geographic advantage and connect U.S. LNG supplies to countries like Ukraine, Slovakia and Hungary. Strong demand signals—14 entities expressing interest, with peak needs nearly four times planned capacity—underscore Poland’s potential role, though regulatory hurdles still limit its appeal as a trading hub.

- Google Cloud and NextEra Energy have agreed to co-develop multiple data-center campuses paired with dedicated power plants, deepening the integration of tech and energy as AI-driven electricity demand accelerates. NextEra also announced roughly 2.5 GW of new clean-energy contracts with Meta, underscoring the scale of hyperscaler power needs and the growing reliance on utility partnerships to meet them.

- Smackover Lithium, the Standard Lithium–Equinor joint venture, has received over $1 billion in expressions of interest from major export credit agencies—including EXIM and Norway’s Eksfin—to support project financing for the South West Arkansas lithium development. Combined with strong indications from commercial lenders, interest now exceeds the JV’s targeted $1.1 billion project debt package, underscoring the strategic importance and de-risking of what could become the first large-scale lithium project in the Smackover formation.

Threats

- President Zelensky said peace talks with the U.S. remain stuck over the status of Donetsk and control of the Zaporizhzhia nuclear plant — regions that are not only strategically vital but also rich in uranium, lithium, and other critical minerals essential to modern energy and defense supply chains. Control over these assets, along with Europe’s largest nuclear power facility, heightens the stakes of any settlement and creates potential global bottlenecks in nuclear fuel, battery materials, and energy security should the conflict continue unresolved.

- Indonesia will impose fines ranging from 354 million to 6.5 billion rupiah per hectare on miners operating beyond their forest permits, with penalties varying by the duration of the breach and the commodity, hitting nickel producers hardest under President Prabowo Subianto’s crackdown on illegal activities in the commodities sector. This move, which has already led to seizures at operations like PT Weda Bay Nickel and probes into state entities, marks a stark shift from the previous administration’s expansion-friendly policies, aiming to curb environmental damage and recover up to 300 trillion rupiah in lost state revenue.

- China’s Central Economic Work Conference signaled a shift toward stronger resource nationalism in 2026, elevating “optimizing supply” as a top policy mandate — a move that points to tighter capacity controls, strategic inventory purchases, and greater state intervention in critical materials like copper and polysilicon. While the meeting projected a more supportive macro stance, the prioritization of domestic security and supply-chain control underscores a growing threat of tighter export policies and reduced availability of key commodities for the rest of the world.

Bitcoin and Digital Assets

Strengths

- Tether joined a €70 million funding round led by CDP Venture Capital and AMD Ventures to fund Italy’s Generative Bionics, accelerating development of its physical‑AI humanoid robots, with the company set to debut its first full humanoid at CES in January, reports Bloomberg.

- BMW is now using JPMorgan’s Kinexys blockchain platform to automate FX transfers, moving euros to New York whenever dollar balances fall, enabling instant, 24-7, rules‑based transactions, and reducing the company’s need for manual treasury management and capital buffers, according to Markets Media and related coverage.

- The CFTC has approved a pilot letting Bitcoin, Ether, USDC, and tokenized Treasuries be used as collateral for derivatives trades, reports Decrypt, marking a major step in integrating crypto assets into U.S. financial market infrastructure.

Weaknesses

- Shares of newly public Bitcoin treasury firm Twenty One Capital plunged 24% on its NYSE debut after merging with Cantor Equity Partners, despite holding $3.9 billion in Bitcoin and securing backing from Tether, Bitfinex, and SoftBank.

- The crypto fall has pushed some Bitcoin miners below profitability as hash-price revenue hits record lows, forcing many to cut power usage while accelerating a broad pivot toward AI and high-performance computing, where miners are retooling their facilities into data centers to secure far more stable, long-term revenue.

- Bloomberg reported on December 9 that U.S. spot Bitcoin ETFs saw their largest withdrawals of the year, with BlackRock’s IBIT alone losing about $2.3 billion in November and total market outflows exceeding $5 billion. The sharp pullback signaled weakening institutional demand and added further pressure to an already fragile crypto market.

Opportunities

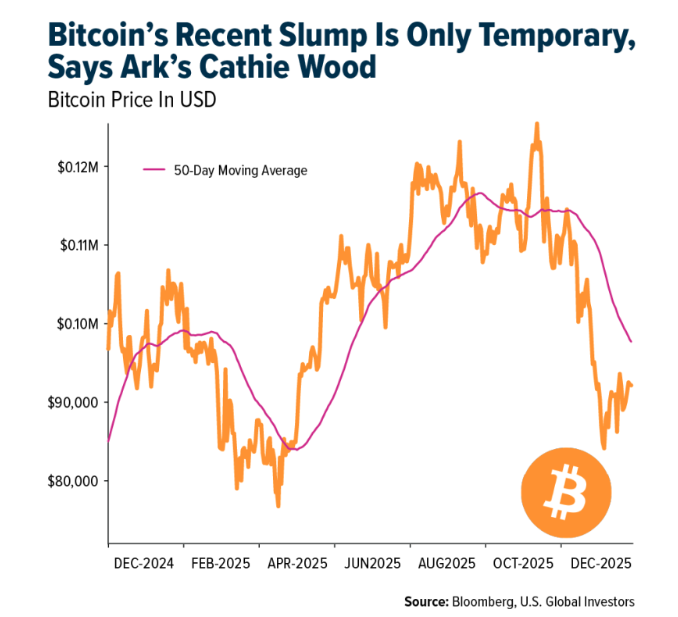

- Ark Invest’s Cathie Wood said Bitcoin’s recent slump is just temporary “wall-of-worry” behavior, arguing that institutional adoption will smooth out its boom-bust cycles, while Ark continues expanding its crypto exposure and remains bullish on both Bitcoin and AI.

- HashKey, Hong Kong’s largest licensed crypto exchange, is seeking up to HK$1.67 billion ($215 million) in an IPO to fund tech expansion, hiring, and stronger risk controls, with cornerstone investors like UBS and Fidelity committing $75 million.

- Ripple’s $500 million share sale attracted major Wall Street investors like Citadel and Fortress at a $40 billion valuation, but only after they secured strong protections including guaranteed returns and preferential rights reflecting how traditional finance is hedging risk as it pushes deeper into crypto.

Threats

- Peter Schiff criticized Michael Saylor’s plan to buy unlimited Bitcoin and turn it into high‑yield BTC‑backed credit, calling the idea unrealistic and arguing that Saylor cannot promise stable, perpetual returns from a highly volatile asset.

- Coinbase Citadel accused Andreessen Horowitz‑backed DeFi platforms of threatening U.S. stock‑market protections as tokenized equities grow, sparking a public clash over whether decentralized exchanges like Uniswap should be allowed to operate as de facto brokerages without traditional regulatory obligations.

- Bloomberg’s Odd Lots newsletter argues that the AI boom is absorbing every available industrial, energy, and technological resource, from Bitcoin miners’ grid connections to jet‑engine turbines, as companies repurpose any asset capable of supporting the exploding demand for AI datacenters.

Defense and Cybersecurity

Strengths

- Germany’s record €52 billion defense procurement approval marks a decisive acceleration in European rearmament. The authorization of 29 major contracts spanning vehicles, missile defense, satellites and basic equipment reinforces long-term visibility for European defense primes and suppliers. This move structurally strengthens Europe’s defense-industrial base and supports multi-year backlog growth across land, air, and space domains.

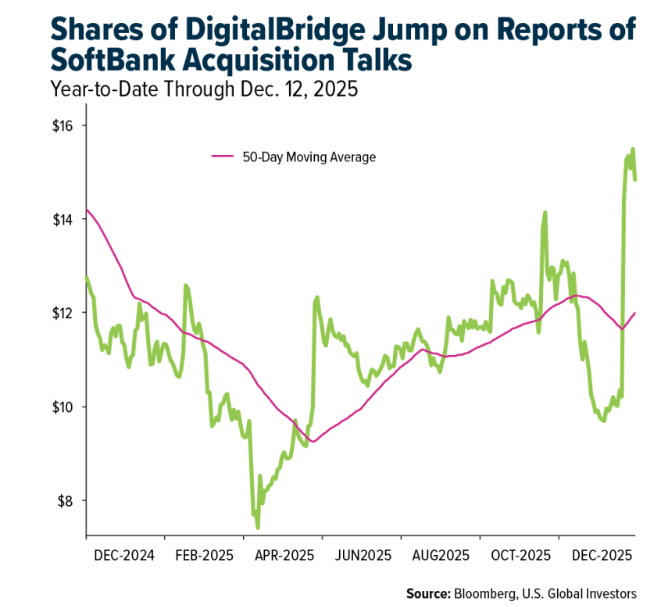

- Shares of DigitalBridge surged as SoftBank entered reported talks to acquire the company, highlighting renewed appetite for AI infrastructure assets. Investor confidence has been boosted by expectations of a take-private transaction tied to data centers and digital infrastructure critical to AI workloads. The rally underscores strategic value being assigned to scaled, power-dense infrastructure platforms amid accelerating AI capex cycles.

- The best performing stock this week was Rocket Lab, rising 25.35% after investors reacted to key Neutron rocket testing milestones, including final validation of reusable hardware. Renewed optimism toward the space sector also drove strong buying interest.

Weaknesses

- Oracle’s mixed earnings exposed near-term execution and valuation sensitivity despite massive AI-driven backlog growth. While RPO surged to $523 billion (+438% YoY), revenue missed consensus and shares fell sharply after hours, highlighting the gap between long-term AI demand and short-term financial delivery. The sale of Ampere also signals strategic recalibration rather than vertical integration confidence.

- Amazon’s decision to select Alchip over Marvell for Tranium 3 and 4 removed a key growth catalyst for Marvell. The loss underscores customer concentration risk and competitive pressure in custom silicon, where hyperscalers increasingly diversify design partners. It also highlights volatility in long-cycle semiconductor design wins tied to AI infrastructure roadmaps.

-

The weakest stock for this week was Aerovironment. Shares of the company declined 14.15% following earnings, as record sales of $472.5 million—driven by the the BlueHalo acquisition—were overshadowed by acquisition-related charges that pressured adjusted EPS, despite solid guidance and unanimously bullish analyst sentiment.

Opportunities

- Nvidia received U.S. approval to sell its H200 AI chips to select customers in China, providing incremental revenue upside despite ongoing export restrictions. While next-generation Blackwell and Rubin architectures remain fully restricted, access to H200 represents a significant performance upgrade versus legacy alternatives. This supports near-term sales while preserving strategic limits on the most advanced AI capabilities.

- Defense and enterprise technology partnerships continue to expand into higher-margin software, AI and cybersecurity layers. Collaborations such as Lockheed Martin with Microsoft on counter-UAS systems and F5 with NetApp on post-quantum security demonstrate rising demand for software-defined, AI-enabled platforms. These initiatives broaden addressable markets beyond hardware and strengthen recurring revenue potential.

- Large-scale government and hyperscaler investments in AI and cloud infrastructure are accelerating globally. Microsoft’s $17.5 billion AI and cloud investment plan in India reflects rising demand for data centers, connectivity and sovereign cloud capabilities across emerging markets. This trend supports long-term growth for infrastructure, semiconductor and cybersecurity providers positioned along the AI value chain.

Threats

- Legal and sanctions-related risks for semiconductor companies are increasing amid heightened geopolitical scrutiny. Lawsuits in Texas alleging that U.S. chips were used in Russian weapons systems raise the possibility of tighter compliance enforcement and reputational damage. Such developments could disrupt global supply chains and constrain international sales channels.

- Competition for scarce AI talent is intensifying and increasingly spilling into legal disputes. Palantir’s lawsuit against Percepta AI over alleged employee poaching highlights how talent shortages are becoming an operational and strategic risk. Rising compensation costs, litigation, and turnover may slow execution across the AI ecosystem.

- The rapid buildout of AI and defense infrastructure faces mounting execution risks tied to power availability, supply chains and system integration. Complex projects spanning data centers, advanced manufacturing and military software depend on tight coordination across multiple layers. Delays or cost overruns at any stage could pressure returns despite strong secular demand.

Gold Market

This week gold futures closed up 2.04%, despite fluctuations during the week. Gold stocks, as measured by the NYSE Arca Gold Miners Index, were up 5.27%. The S&P/TSX Venture Index rose 1.58%. The U.S. Trade-Weighted Dollar fell by 0.63% by the close of the week.

Strengths

- The best performing precious metal for the week was platinum, up about 6.21%. Platinum strength continues as the metal hits a 52-week high, benefiting from its growing status as a designated critical mineral and rising strategic importance across clean energy, hydrogen and industrial applications. Investor demand has followed, with steady ETF accumulation reinforcing the rally and signaling sustained institutional interest despite already outsized year-to-date gains.

- Silver extended its speculative surge for a fourth straight session, hitting a record above $64/oz and heading for a ~10% weekly gain as ETF inflows, momentum trading and tight physical supply collided. The rally has been amplified by aggressive call-option buying and a weaker-rate backdrop, with silver now sharply outperforming gold despite growing warnings of blow-off-top risk.

- Kinross Gold’s early repayment of US$500 million in 4.50% Senior Notes continues its balance-sheet cleanup, reducing interest costs and lowering financial risk after retiring US$1.5 billion of debt across 2024–2025. While the move strengthens flexibility for future projects and shareholder returns, it doesn’t materially change near-term production or cost pressures, which remain the key drivers of the investment narrative.

Weaknesses

- The worst performing precious metal for the week was gold, still up about 2.04%, as the yellow metal pared earlier gains from hawkish-leaning comments from Fed officials cast doubt on the pace of further rate cuts in 2026, pushing long-end Treasury yields higher and weighing on bullion. The move was exacerbated by a broader risk-off tone, with equity losses prompting some investors to trim metals positions to cover declines elsewhere.

- Chow Tai Fook’s shares fell as much as 2.5% after Jefferies cut its price target to HK$17 from HK$18.5 and reduced earnings estimates, citing weak consumer retail sales and a shift in gold and jewelry consumption from event-driven to discretionary spending. The analysts lowered FY26/27/28 net profit forecasts by 8%/11%/11%, assuming sales declines of 5%/5%/6%, while noting management’s conservative stance on guidance despite positive same-store-sales trends, and maintained a buy rating.

- Bank of America notes that, in the past year, gold’s rally has shown a lower correlation with other asset classes than it did throughout the entire post-COVID period. Its connection to Treasuries has also decreased. Additionally, although commodities typically gain when the dollar weakens, this trend has diminished in the current year. For example, crude oil prices have dropped year-to-date, mainly due to decisions by OPEC and geopolitical factors.

Opportunities

- Robex Resources is expected to exercise its matching rights imminently in response to Perseus Mining’s rival offer for Predictive Discovery, following its initial merger proposal that was disrupted last week. The company, advised by Canaccord Genuity and Peloton Legal, is pitching to Predictive shareholders that a merger could lead to future takeovers by major players like AngloGold or Barrick, while funding development of the Bankan asset through cashflow without new equity, though the exact terms, including Robex’s potential ownership reduction from 49% to as low as 36.5%, remain unclear.

- Goldman Sachs says its $4,900/oz gold forecast for end-2026 could see “significant upside” if U.S. investors increase their very low allocations to gold ETFs, noting that even a one-basis-point shift in portfolios would lift prices by roughly 1.4% due to the market’s small size.

- India will now allow its $177 billion National Pension System to invest in gold and silver ETFs for the first time, potentially unlocking around $1.7 billion of new demand for the metals. The move reflects growing global acceptance of precious metals as mainstream portfolio assets, coming alongside similar policy shifts in China and amid record rallies in both gold and silver.

Threats

- Restrictions on exporting gold bullion from Russia will enter effect in 2026, as stated by Deputy Prime Minister Alexander Novak during a meeting on strategic development and national projects. The measures also aim to prevent uncontrolled exporting of cash rubles of unknown origin from Russia, including to member states of the Eurasian Economic Union.

- Marex Group says the silver market has become “overexcited,” arguing prices are about 15% too high in the short term and due for consolidation or a pullback. While private wealth flows into precious metals remain strong amid concerns over debt and fiat currencies, Marex warns that silver’s recent surge has outpaced fundamentals even as long-term support for gold remains intact.

- Dozens of Tibetans were reportedly detained after staging a rare protest against a new gold mine in Sichuan’s Gayixiang township, with activists saying authorities have sealed off the area, cut communications, and tightened security. The incident highlights mounting tensions over resource extraction on the Tibetan plateau, where communities fear environmental damage and loss of traditional livelihoods amid broader crackdowns on cultural and religious freedoms.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2025):

American Airlines

Ryanair Holdings

COSCO Shipping Holdings

Southwest Airlines

Boeing

Tesla

Ferrari

LVMH

Hermes

Kinross Gold Corp.

Chow Tai Fook

Perseus Mining Ltd.

AngloGold Ashanti Plc

Barrick Mining Corp.

Grupo Aeroportuario del Pacifico

Sabre Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits