The World’s Largest Oil Reserves Is Now Under U.S. Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhat happened in Venezuela last weekend may turn out to be the most consequential energy and geopolitical event of the decade.

In a swift, coordinated operation that stunned the world, U.S. forces captured Venezuela’s longtime socialist dictator, Nicolás Maduro.

Nearly just as swiftly, President Donald Trump declared that the U.S. will not only rebuild the country’s devastated oil infrastructure but also control all crude exports indefinitely.

To some, this might sound like neo-colonialism. But to investors, it could be an opportunity.

The U.S. Reasserts Its Sphere of Influence

Our office was visited this week by retired Army lieutenant general John Evans, who commented that the operation was a demonstration as much for America’s non-Western Hemisphere adversaries—Russia, China, Iran, et al—as it was for Venezuela, Colombia and Cuba.

As I talked about in a previous post, what we’re seeing unfold is the rebirth of the Monroe Doctrine, the 200-year-old idea that the U.S. is the dominant force in the Western Hemisphere and that European powers shouldn’t interfere.

The 21st-century iteration of the Monroe Doctrine—nicknamed the Trump Corollary, or the “Donroe Doctrine”—is similarly meant as a warning to China and Russia that Latin America’s vast resources, including oil, is off-limits.

In Trump’s own words, “We’re going to be using [Venezuela’s] oil, and we’re going to be taking oil.”

The administration has already announced it will market and sell 30 to 50 million barrels of Venezuelan oil, with proceeds controlled directly by Trump. Energy Secretary Chris Wright went further, confirming that the U.S. will be selling Venezuelan oil “indefinitely,” starting with backed-up storage barrels and expanding future production.

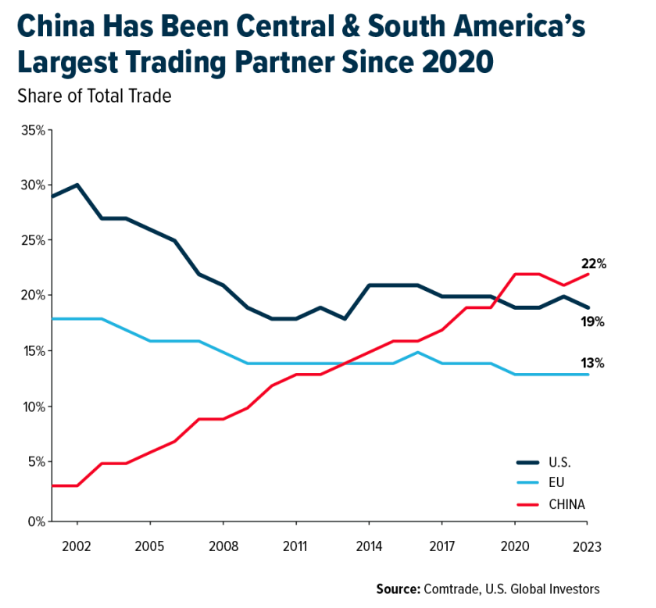

China is Venezuela’s largest oil customer, buying 80% of the exports, and Latin America’s largest trading partner since 2020. It’s invested heavily across the region, in ports, telecom, power grids and more. With 37 port projects under its belt and $13 billion in credit lines pledged to the region, Beijing may not give up Latin America so easily.

Venezuela: Rich in Resources but Poor in Production

Some investors still don’t realize just how resource-rich Venezuela is.

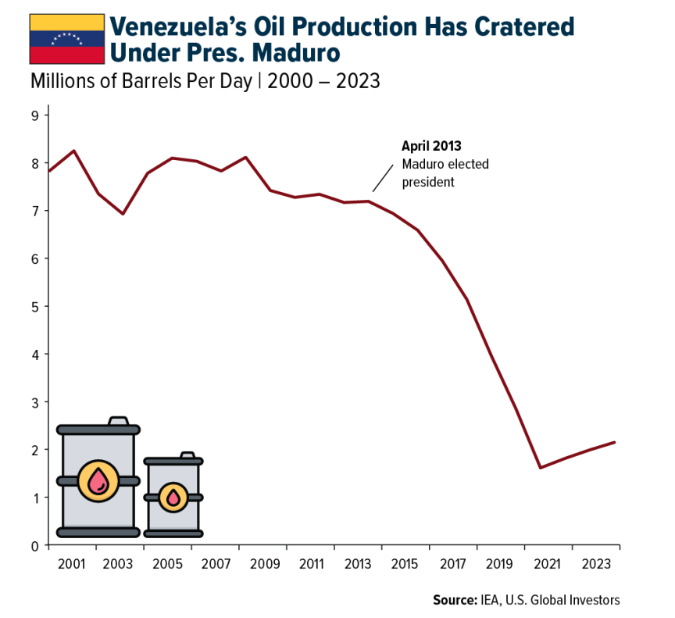

The country holds over 300 billion barrels of proven oil reserves, more than any other nation on the planet. That’s nearly one-fifth of the world’s total reserves.

And yet today, Venezuela accounts for just 1% of global oil production.

Thanks to decades of socialism, corruption and mismanagement, Venezuela’s oil infrastructure has crumbled. Output has plummeted from between 7 and 8 million barrels a day to under 1 million barrels today.

Why Reviving Venezuela’s Oil Won’t Be Cheap or Easy

With Maduro out and Washington in charge, there’s renewed optimism in Venezuela’s oil industry… but also massive capital requirements. Energy consultancy firm Rystad estimates it will take as much as $110 billion in capex spending just to restore Venezuelan output to where it was 15 years ago.

That dollar amount is twice what all U.S. oil majors spent globally in 2024 alone, according to a CLSA report to investors.

This may be why Trump said the government would reimburse oil companies for getting the country’s oil operations “up and running” again.

“A tremendous amount of money will have to be spent, and the oil companies will spend it, and then they’ll get reimbursed by us or through revenue,” the president told NBC News.

Even if the money shows up, there’s still the problem of manpower. Tens of thousands of skilled engineers and geologists have not only fled the country but stripped and/or stole equipment, vehicles and copper wiring from the country’s state-run oil company, Petróleos de Venezuela. Much of Venezuela’s oil is ultra-heavy crude, requiring special treatment and naphtha blending to be transported.

Defense and Energy Stocks Catch a Bid

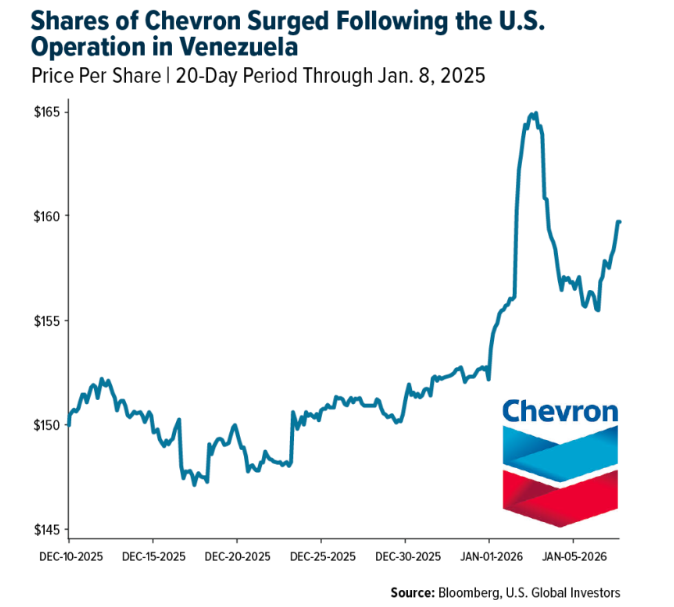

Despite these hurdles, markets rallied hard on the news of Maduro’s removal. The best performing Dow Jones stock on Monday was Chevron, surging as much as 10% in intraday trading but ending the day up around 5%.

Chevron—currently the only U.S. major operating in Venezuela, exporting about 140,000 barrels a day—is reportedly negotiating with the U.S. for an expanded license to export more Venezuelan crude, and not just to U.S. refineries but to thirty-party buyers.

European defense contractors also jumped on Monday, including Rheinmetall (+9.06%), Leonardo (+6.41%), BAE Systems (+5.10%) and Thales (+4.80%).

U.S. defense names followed suit: Northrop Grumman (+4.38%), General Dynamics (+3.54%), Lockheed (+2.92%).

Final Takeaways

Venezuela’s return to oil markets will likely increase global supply, putting downward pressure on crude prices: Bloomberg’s Mike McGlone sees West Texas Intermediate (WTI) trading in the $42 to $65-per-barrel range this year.

That may be bad for OPEC, but good for U.S. consumers and refiners, not to mention airlines and cargo ships.

From an investment point of view, I might urge investors look at energy selectively. Names like Chevron may benefit from Venezuela’s reopening.

I also think investors should consider staying overweight defense, for obvious reasons, especially when combined with news that a military takeover of Greenland isn’t off the table. What’s more, Trump is actively pushing for the 2027 U.S. military budget to be raised to a mind-boggling $1.5 trillion.

And of course, as always, I recommend a 10% weighting in gold, split evenly between physical bullion and high-quality gold mining names.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Frontier, up 16%, on the news of Jim Dempsey stepping in as the new CEO. According to UBS, Cathay Pacific’s second-half group RPK was up 28% year-over-year, exceeding the capacity expansion rate of 26% and driving a 140 basis points (bp) year-over-year improvement in passenger load factor to 84.9%.

- The Baltic Exchange Airfreight Index showed that air cargo rates from Hong Kong to North America increased by 6.7% month over month in December to reach $6.60 per kilogram, the highest monthly average recorded this year, according to Morgan Stanley.

- Frontier noted that it now expects to land at the high end of its $0.04 to $0.20 early-November earnings per share (EPS) guidance, versus consensus of $0.07, according to Raymond James. Frontier has seen strong close-in bookings over the last few weeks of December.

Weaknesses

- The worst-performing airline stock for the week was Ryanair, down 3.8%. Grupo Aeroportuario del Pacífico’s total traffic increased 0.1% year-over-year in December. International traffic declined 6.2% YoY, lagging domestic traffic, which rose 5.8% YoY. Traffic in Guadalajara increased 9.2% YoY, while traffic in Tijuana decreased 2.7% YoY. Traffic at Jamaican airports fell 32.6% YoY due to disruptions caused by Hurricane Melissa, according to Morgan Stanley.

- ZIM shares declined after the Companies Authority intervened in the sale of the shipping company, slightly cooling the sales process, according to Calcalist’s Golan Hazani. The Authority issued a warning to Chairman Yair Saroussi that the state has the right to object to the sale of more than 24% of ZIM’s shares, according to Morgan Stanley.

- Water safety on aircraft remains a concern. Delta, Frontier, and Alaska score exceptionally well on water safety, while American ranked the worst and received a failing grade. Approximately 3% of airline water samples fail bacterial tests. Passengers are advised to drink only bottled water, avoid coffee, and refrain from washing hands with onboard tap water.

Opportunities

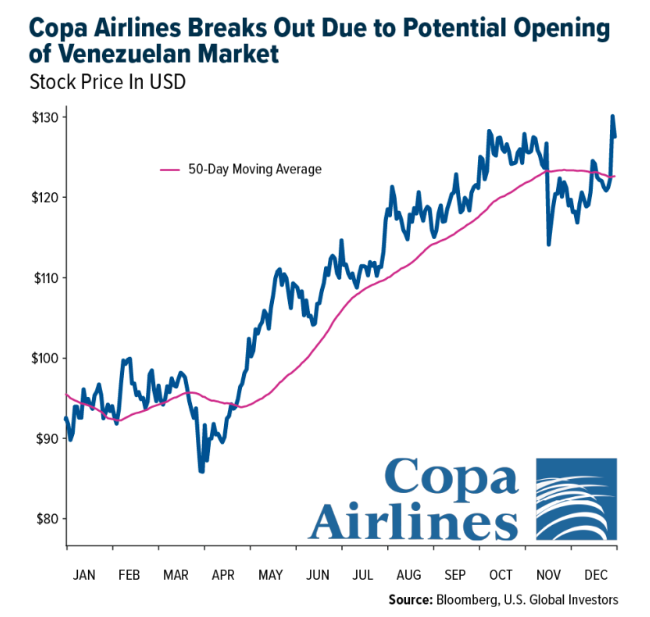

- Copa Holdings is the only listed carrier with exposure to Venezuela, operating one daily flight to Maracaibo. However, prior to 2014, Copa derived 10–15% of its revenue from Venezuela, and JPMorgan views the company as the main potential long-term beneficiary of a significant reopening of the Venezuelan market.

- Key takeaways from Goldman Sachs on China Merchants Port Holdings include: 1) management guidance for 1–2% throughput growth at domestic terminals in 2026, and low- to mid-single-digit growth at overseas terminals; and 2) expectations for 3–4% average selling price growth year-over-year at overseas terminals in 2026.

- American Airlines announced that it is reshaping its operations at DFW to improve reliability and the customer experience. Specifically, the airline is moving from a nine-bank flight schedule to a 13-bank structure beginning in April, spreading flights more evenly throughout the day and making connections smoother and more dependable for customers passing through DFW each day, according to Raymond James.

Threats

- Per FlightAware, JetBlue canceled 21% of flights earlier in the week, followed by Frontier at 10%, due to the Venezuela situation. Cancellations have eased for the most part since then. The situation could drive some near-term booking shifts away from the Caribbean.

- Suez Canal transits appear to be creeping higher, up 28% week over week and 64% versus the prior month. This could mark the beginning of a full-scale return, though more data points are needed to confirm, according to Morgan Stanley.

- West Coast jet fuel, which accounts for roughly 50% of Alaska Air’s consumption, has increased by more than $0.55 per gallon since the start of the year. The airline’s exposure is partially mitigated by its geographic fuel mix, with approximately 50% sourced from the West Coast (Los Angeles jet fuel at $2.74 per gallon), 25% from Singapore (currently $1.89 per gallon), and the remainder split between the Gulf Coast ($1.86 per gallon) and New York ($1.94 per gallon), according to Bank of America.

Luxury Goods and International Markets

Strengths

- Almost 100 Chinese cities welcomed foreign visitors for New Year celebrations. Inbound ticket bookings surged 110% across Chinese cities, according to data from the platform Qunar. Additionally, reservations for experiential entertainment products increased 30-fold, highlighting tourists’ growing preference for immersive experiences over traditional sightseeing.

- This week, the services PMI for the U.S., Eurozone, and China all reported readings above 50, indicating continued sector expansion. This broad-based improvement underscores resilience in global economic conditions and reflects ongoing demand strength across major regions.

- Ralph Lauren was the best-performing stock in the luxury index this week, rising more than 20.6%. Investors reacted positively to a series of analyst upgrades and higher earnings expectations, boosting sentiment around the company’s near-term growth prospects.

Weaknesses

- Volkswagen’s U.S. sales performance weakened considerably in the fourth quarter of 2025, with deliveries falling about 19.8% year-over-year to roughly 82,800 vehicles. This decline capped a challenging year for the German automaker, which saw overall annual sales drop approximately 13% compared with 2024.

- Pandora’s shares continue to decline as sharply rising silver prices pressure margins, forcing the company to raise prices and adjust its product strategy while still struggling to offset costs without reducing demand. The company now expects lower-than-previously forecast growth, reflecting weaker consumer sentiment and ongoing input cost headwinds.

- Melco Resorts & Entertainment was the worst-performing stock in the luxury index this week, falling 11.8%. The company’s stock has been under pressure as broader Macau gaming names slid amid investor concerns about slower growth and volatility in gaming revenue, with some reports noting Melco losing market share to peers.

Opportunities

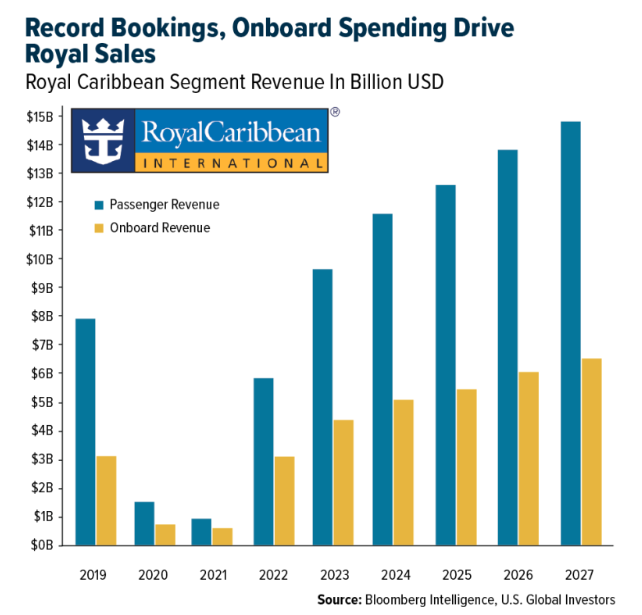

- Record bookings and increasing onboard spending will translate into strong revenue growth for Royal Caribbean. It is the world’s second largest cruise operator, with 24% of global capacity. The company owns three lines: Royal Caribbean, Celebrity and Silversea. It will enter high-end river cruising through its Celebrity brand in 2027.

- On December 30, European Luxury Market Research released its 2026 market outlook, highlighting Poland as one of Europe’s most structurally resilient and strategically important luxury markets. The country is now among the world’s top 20 largest economies, and growth in Poland’s luxury sector is being driven primarily by domestic consumers rather than tourism or short-term spending spikes.

- India is projected to be the fastest-growing major economy in 2026, with forecasts calling for growth of around 6–7%, supported by strong domestic demand, investment, and structural reforms. While smaller emerging markets may post higher percentage growth rates, India stands out among the world’s largest economies, outpacing China, the United States, and Europe, making it a key driver of global economic expansion in 2026.

Threats

- Saks Fifth Avenue is reportedly exploring a possible bankruptcy filing as financial pressures continue to mount across the luxury retail sector. The company has faced weaker consumer demand, rising operating costs, and intensifying competition from online luxury platforms. The situation was further complicated by the recent resignation of its CEO, adding uncertainty to the company’s leadership and strategic direction.

- Nvidia announced its new autonomous driving AI technology, called Alpamayo, which could potentially compete with Tesla’s FSD over the long term. Mercedes plans to integrate Nvidia’s self-driving system starting in 2026, and companies such as Uber and Lucid are also partnering around Nvidia’s technology. For now, Tesla remains advantaged in real-world data and vertical integration. Elon Musk commented that “Nvidia’s Alpamayo technology could be competitive with Tesla’s FSD in the next five or six years.”

- BMW’s fourth-quarter vehicle deliveries declined due to slumping sales in China. Sales of BMW and Mini models in key Asian markets fell 16%, offsetting modest gains in Europe. Global auto deliveries for the quarter fell 4.1%, resulting in roughly flat full-year sales. German automakers continue to lose market share in China to local competitors, led by BYD.

Energy and Natural Resources

Strengths

- Lithium carbonate was the best-performing commodity of the week, rising just over 22%. Prices surged in China due to supply cuts in Jiangxi after authorities canceled 27 mining permits, alongside bullish demand forecasts from major producers tied to energy storage growth.

- Ukraine’s decision to grant development rights for the Dobra lithium deposit to a Western-backed investor group marks a strategic step toward integrating its critical minerals into U.S. and allied battery supply chains. The move reduces geopolitical risk and improves the long-term outlook for Western lithium supply.

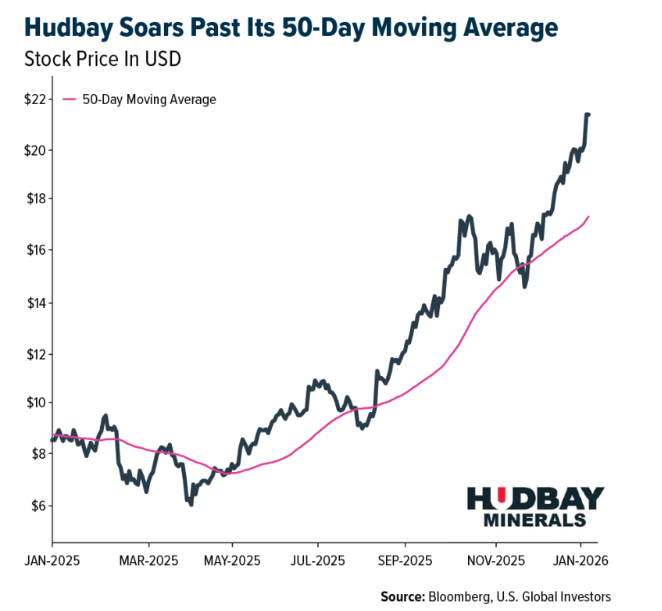

- Copper’s rally reflects tightening supply and strong demand tied to global electrification and infrastructure spending. Trade concerns and mine disruptions have reinforced its strategic value, with Hudbay reaching a new 52-week high, highlighting strong momentum across the copper sector.

Weaknesses

- Natural gas was the weakest-performing commodity of the week, declining approximately 12%. Prices slid amid mild winter weather and ample storage levels across key markets, reflecting muted heating demand and oversupply concerns. This underperformance contrasts sharply with gains in industrial metals such as aluminum and copper and underscores ongoing volatility in gas markets as near-term fundamentals remain bearish.

- Crude oil markets continue to show structural weakness, with Saudi Arabia cutting its flagship Arab Light price to Asia for a third consecutive month despite OPEC+ maintaining a pause on output increases. This pricing action, combined with International Energy Agency projections for a sizable global surplus, confirms persistent oversupply and soft demand conditions. Broad regional price cuts signal that supply coordination alone is no longer sufficient to stabilize crude prices.

- Shell warned that its oil trading performance in the fourth quarter will be significantly lower than the prior quarter, signaling a weak end to the year amid slumping crude prices and oversupply concerns. The company also expects a significant loss in its chemicals division, adding pressure ahead of earnings season. This highlights the challenges Big Oil faces in a lower-price environment, despite Shell’s earlier cost-cutting and asset sales strategy.

Opportunities

- Capital flows into clean-energy infrastructure continue to accelerate, with global green-debt issuance reaching a record $947 billion last year. Banks earned about $3.7 billion in climate-related fees in 2025, exceeding fossil-fuel financing for the fourth straight year, driven increasingly by improved economics rather than ESG considerations.

- Copper offers a compelling multi-year opportunity as AI data centers, electrification, and the energy transition drive demand while supply remains constrained. Mine disruptions, long project timelines, and slowing discovery rates support tighter availability and higher long-term prices.

- The potential reopening of Venezuelan oil flows under a clearer legal framework offers medium- to long-term upside for global traders and integrated producers. While near-term supply gains may be limited, reduced geopolitical friction and eventual reinvestment could unlock incremental volumes over time, positioning Venezuela as latent optionality rather than an immediate supply shock.

Threats

- Nickel markets highlight the fragility of policy-driven rallies, with prices retreating sharply after Indonesia failed to provide concrete details on planned production cuts. Exemptions for committed investments and the absence of enforceable quotas signal limited near-term supply discipline, exposing persistent structural oversupply. The episode increases downside risk for nickel and related battery-metal exposures, according to Bloomberg.

- Trade and tariff distortions remain a key risk across industrial metals, particularly copper, where stockpiling ahead of potential tariffs has driven sharp pricing and inventory dislocations. As physical flows normalize, these policy-driven spreads risk rapid mean reversion, introducing volatility and downside risk for prices and equities exposed to artificial tightness.

- China’s decision to halt export license reviews for rare earths to Japan escalates geopolitical tensions and threatens critical supply chains for semiconductors, autos, and defense. The restrictions could cost Japan an estimated $17 billion in economic losses, underscoring Beijing’s willingness to weaponize its dominance in rare-earth materials and highlighting vulnerabilities for Japanese manufacturers and global electronics production.

Bitcoin and Digital Assets

Strengths

- The tokenization of Brazilian credit card receivables through BlackOpal’s GemStone platform highlights the growing maturity of real-world asset tokenization. By combining true-sale legal structures, central bank registry integration, and traditional payment rails, the initiative delivers institutional-grade, U.S. dollar–denominated yield (approximately 13%) while improving liquidity for merchants. This underscores crypto’s expanding role as financial infrastructure, particularly in emerging markets.

- Ether strengthened crypto’s institutional credibility by expanding beyond stablecoins into tokenized gold. With XAUT backed by more than 1,300 gold bars and a market capitalization of approximately $2.3 billion, the launch of Scudo (1/1,000-ounce units) improves the divisibility and on-chain settlement of gold. This reinforces crypto’s role as infrastructure for hard assets alongside Bitcoin, especially amid record central bank gold accumulation.

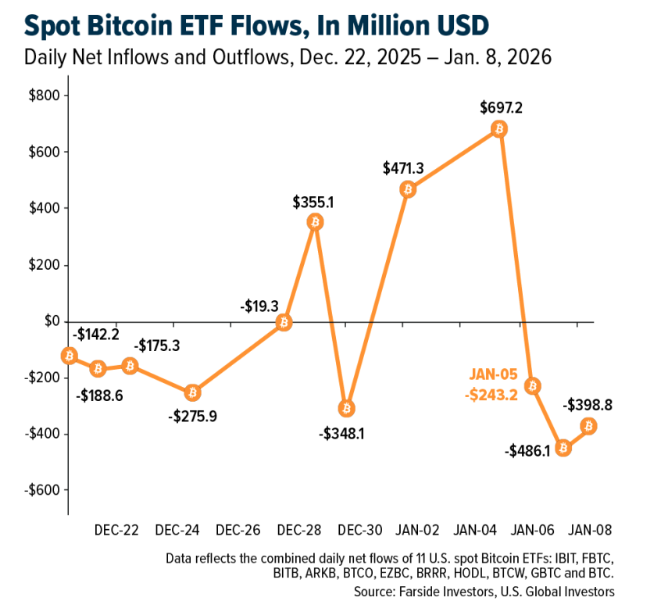

- U.S. spot Bitcoin ETFs reaffirmed their role as the primary institutional access point to crypto, attracting $697 million in inflows on the second trading day of 2026 and more than $1.1 billion in total inflows across the first two days of the year, according to Farside Investors. Despite significant outflows in late 2025, ETF assets remain above $110 billion, highlighting durable institutional participation and positioning ETFs as a structural, long-term allocation channel rather than short-term speculative capital.

Weaknesses

- Bitcoin’s failure to break above $95,000 and its repeated tests of the $89,200 support highlight weakening momentum amid ETF outflows and lighter trading volumes. At the same time, derivatives positioning shows rising leverage, with open interest nearing 700,000 BTC and persistently positive funding rates. This crowded long positioning increases downside risk, as even modest price declines could trigger forced liquidations and amplify volatility.

- The latest pullback highlighted crypto’s continued sensitivity to macro risk sentiment, with speculative segments leading losses. Memecoins and DeFi underperformed sharply, the CoinDesk Memecoin Index fell 8.6% in 24 hours, while DeFi and metaverse indexes dropped over 5%, as ETF outflows of $729 million reversed more than half of the prior week’s inflows. The episode underscores how quickly tourist capital exits during periods of uncertainty, reinforcing downside reflexivity across the market.

- The mass resignation of the Electric Coin Company team exposed governance and incentive misalignment within one of crypto’s most established privacy protocols. Internal disputes over nonprofit versus for profit structures triggered ecosystem fragmentation, a sharp ZEC sell off, and renewed questions around execution risk. The episode highlights how organizational instability, rather than technology, can undermine investor confidence and long-term adoption.

Opportunities

- Optimism’s proposal to allocate 50% of Superchain revenue to OP token buybacks marks a shift toward clearer value accrual models in crypto. By linking token economics directly to sequencer fee revenue from major ecosystems such as Base, Uniswap, and Sony-backed chains, the initiative reflects a broader industry move toward sustainable, revenue-backed token frameworks. If adopted, this model could strengthen long-term holder alignment and set a precedent for Layer 2 token design.

- The launch of regulated crypto ETFs that incorporate staking highlights a growing opportunity to position digital assets as yield-bearing instruments. Morgan Stanley’s proposed Ethereum ETF would allow investors to earn staking rewards currently estimated at 3% to 4% annually on Ether, in addition to price exposure. This comes as U.S. spot Ether ETFs have retained more than 80% of their peak inflows despite the 2025 crypto market drawdown, signaling sticky institutional demand. With global crypto ETF assets exceeding $125 billion in 2025, the integration of yield mechanisms could materially expand addressable capital and accelerate adoption of crypto within income-oriented and multi-asset portfolios.

- The launch of regulated stablecoin and RWA tokenization indexes by MarketVector, alongside NYSE-listed ETFs, underscores the growing institutionalization of crypto infrastructure. These products allow traditional investors to gain compliant exposure to stablecoin and tokenization technologies without holding digital assets directly, reinforcing crypto’s integration into mainstream financial markets.

Threats

- The potential delay of U.S. crypto market structure legislation until 2027 extends regulatory uncertainty for exchanges, issuers, and investors. Election-driven politics and conflict-of-interest debates increase the risk of legislative paralysis. The lack of near-term clarity may slow institutional investment and strategic decision-making in the U.S. crypto market.

- U.S. crypto regulation has reached a do-or-die moment as Senate negotiations stall over stablecoin yield rules and unresolved concerns around presidential conflicts of interest. Without strong bipartisan support, the market structure bill risks failing outright, potentially delaying regulatory clarity until after the 2026 midterms. Prolonged uncertainty would preserve the status quo, limiting institutional participation and reinforcing policy risk across digital assets.

- Despite high crypto adoption, Latin America continues to face regulatory uncertainty and fragile fiat infrastructure. Coinbase’s suspension of peso on- and off-ramps in Argentina, alongside Brazil’s move to tax crypto-based cross-border payments and stablecoin usage, underscores execution and policy risk even for global Tier 1 players. These constraints limit crypto’s ability to scale beyond trading into payments and financial inclusion, reinforcing dependence on regulatory clarity and banking cooperation across the region.

Defense and Cybersecurity

Strengths

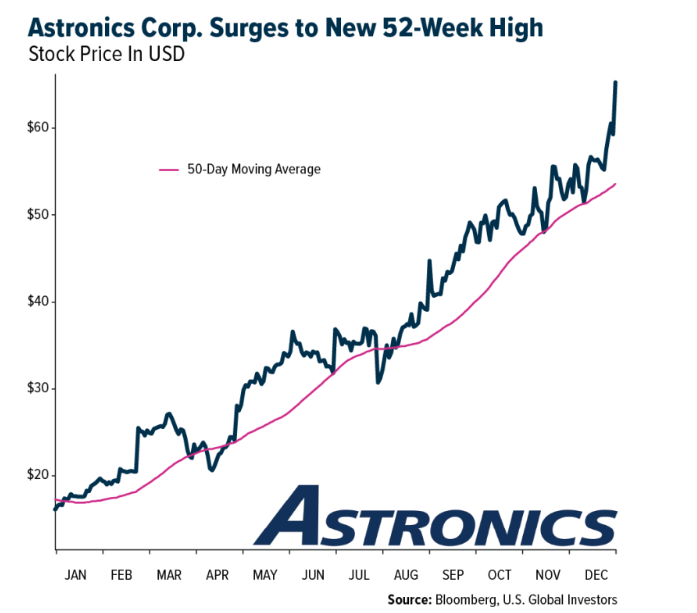

- Shares of Astronics Corp. surged to a new 52-week high after the company issued 2026 revenue guidance of $950–$990 million, beating consensus expectations on strong bookings, backlog momentum, and preliminary fourth quarter results that topped forecasts.

- The successful U.S. military operation in Venezuela demonstrated overwhelming operational superiority and showcased the ability of American forces to execute missions that no other country could realistically attempt. The precision and coordination of elite units, including Delta Force, reinforced the perception of the U.S. as the world’s unquestioned military leader, directly supporting confidence in U.S.-centric defense capabilities and the strategic credibility that underpins global security markets.

- The best-performing stock in the XAR ETF last week was Kratos Defense & Security, up 43.4%, after the company announced a Marine Corps CCA contract for its Valkyrie drone with Northrop Grumman. Analysts view the deal as a “needle-moving” positive, alongside broader defense-sector gains driven by President Trump’s proposal to increase the U.S. military budget by roughly 50%.

Weaknesses

- Restrictions imposed by the U.S. administration on dividends, share buybacks, and executive compensation for major defense contractors have introduced a structural overhang on the sector. Despite rising defense budgets, these measures weaken capital-return visibility and valuation support for companies such as Lockheed Martin and Northrop Grumman, limiting upside from budget-driven revenue growth.

- The accelerating shift toward AI-enabled warfare, autonomous systems, and next-generation platforms increases execution risk for incumbents with heavy exposure to legacy programs. Failure to adapt fast enough to new operational doctrines could result in contract displacement and erosion of long-term backlog visibility.

- The weakest-performing stock in the XAR ETF last week was Carpenter Technology, down 2.86% as investors reassessed valuation concerns. The stock may already reflect peak growth, stiff competition, and cyclical aerospace demand that could soften near-term revenue expectations.

Opportunities

- NVIDIA unveiled its Rubin architecture at CES 2026, marking a step change in data-center computing with sharply lower inference costs and improved performance at scale. The shift toward rack-scale systems and reduced reliance on traditional cooling strengthens NVIDIA’s long-term dominance in AI infrastructure while reshaping the broader data-center supply chain.

- The planned joint venture between Rheinmetall and MBDA to develop naval laser weapon systems highlights Europe’s accelerating move toward directed-energy defenses. Successful testing and a targeted 2026 launch open a high-margin segment in naval air and missile defense with strong export potential.

- Large-scale capital inflows into AI infrastructure, including funding rounds for xAI and NVIDIA-backed Nscale, signal a sustained global build-out of compute capacity underwritten by hyperscalers and model providers. This benefits second- and third-order players across networking, power management, advanced cooling, and cloud infrastructure.

Threats

- Russia’s latest large-scale strike on Ukraine reportedly used the Oreshnik missile with its warhead removed to limit destruction while demonstrating speed, trajectory, and delivery. Open-source estimates suggest it reaches hypersonic velocities above Mach 20, meaning even without explosives, the kinetic impact is equivalent to multiple tons of TNT. The event highlights the sharply reduced interception window for current air- and missile-defense systems and the growing challenge of high-speed delivery platforms.

- The expanding attack surface of AI-enabled and cloud-connected systems continues to elevate systemic cyber risk, as shown by recent exploit chains targeting enterprise software and identity layers. High-profile vulnerabilities may drive heavier regulation, slower AI deployment cycles, and structurally higher compliance costs for governments and corporations.

- Endor Labs disclosed a high-severity vulnerability in the widely used jsPDF library that could allow attackers to embed sensitive local files, such as passwords or configuration data, directly into generated PDFs. Upgrading to jsPDF version 4.0.0 and enforcing stricter file-access controls has addressed the issue, but it underscores how automated document-generation pipelines can be exploited for data exfiltration in AI- and cloud-based environments.

Gold Market

This week gold futures closed the week at $4497.90, up $168.90 per ounce, or 3.89%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 7.42%. The S&P/TSX Venture Index came up 6.06%. The U.S. Trade-Weighted Dollar rose 0.75%.

Strengths

- The best-performing precious metal of the week was silver, up 11.80%. Prices set a fresh record, closing above $80 per troy ounce for the first time. Gold and silver miners raised the most cash through share sales in more than a decade last year, led by smaller players as prices rallied. More than $6.2 billion was raised by companies listed in the U.S. and Canada, according to Bloomberg.

- Central banks bought nearly as much gold in late 2025 as they did in the first eight months of the year, surpassing ETF purchases and signaling continued support for bullion in 2026 despite high prices. The World Gold Council reported net purchases of 45 tons in November alone, bringing total buying for September through November to 137 tons, just below the 142 tons purchased from January through August 2025, according to Bloomberg.

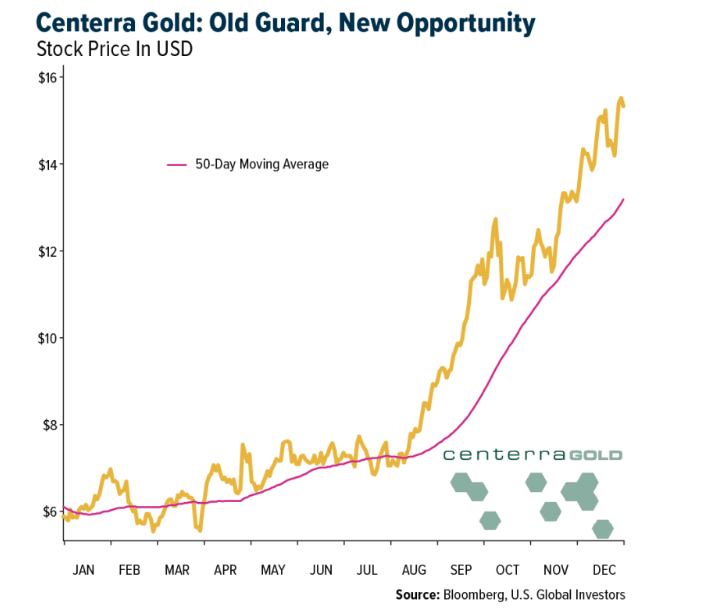

- Centerra Gold Inc., a bellwether producer focused on organic and inorganic growth, reinforced its exploration optionality by exercising its top-up right in Dryden Gold Corp., funding district-scale drilling while maintaining a 9.99% stake. The move comes ahead of Centerra’s fourth-quarter 2025 results and 2026 guidance on February 19, positioning Dryden as a leveraged exploration.

Weaknesses

- The weakest-performing precious metal of the week was gold, though it still gained 3.89%. Gold posted a modest advance, trading up to $4,514 per ounce as mixed U.S. jobs data tempered expectations for an immediate Federal Reserve rate cut. Traders continue to price in two cuts for 2026, while geopolitical tensions and central bank buying remain supportive, reinforcing gold’s role as a safe-haven asset.

- Newmont reported damage from bushfires to a portion of the water supply infrastructure at its Boddington operations in Western Australia. The company expects the infrastructure to be fully restored by February, with an estimated impact of 60,000 ounces of gold production in the first quarter of 2026, according to Bloomberg.

- Endeavour Silver reported fourth-quarter 2025 silver production of 3.8 million ounces, below its estimate of 4.2 million ounces. Lower-than-expected output from its Mexican mines, Terronera, Guanaceví, and Bolañitos, more than offset a strong quarter at the Kolpa mine in Peru, according to Raymond James.

Opportunities

- Silver has become a strategic commodity under China’s tightening export controls, with the Ministry of Commerce now requiring two-year special licenses for exports of silver, tungsten, and antimony. While supply restrictions support prices after last year’s strong rally, the outlook is complicated by China’s solar industry shifting toward silver-light and silver-free photovoltaic technology, as manufacturers substitute base metals to relieve margin pressure from overcapacity.

- According to Bank of America, with gold prices at record highs, a substitution of just 1 percent of gold jewelry demand could increase the platinum deficit by nearly one million ounces, or about 10 percent of annual supply. In the second half of 2025, the launch of physically backed platinum and palladium futures contracts by the Guangzhou Futures Exchange has provided additional price support.

- Gold should continue to rally as the purchasing power of paper currencies weakens, according to Evy Hambro, BlackRock’s global head of thematic investing, speaking on Bloomberg TV. He noted that accelerating currency depreciation, combined with rising geopolitical risks, is likely to support gold and other precious metals.

Threats

- From a fundamental perspective, Bank of America expects total gold production in 2026E to be 2% lower, at 19.2 million ounces, across the 13 North American precious metals stocks in its coverage. The firm believes consensus estimates are about 2% too high for 2026E production, creating a near-term headwind. For these 13 stocks, Bank of America forecasts average all-in sustaining costs rising 3% to $1,600 per ounce in 2026E.

- As silver prices reach multi-decade highs, a senior mining analyst is warning against rising investor exuberance, particularly in the junior mining space. Speaking on the Resource Talks podcast on Saturday, Joe Mazumdar, a senior mining analyst at Exploration Insights, said he has become increasingly uneasy with how some investors are valuing silver companies, citing what he described as overly simplistic assumptions.

- Donald Trump’s latest threats toward Mexico, framed around cartel crackdowns and potential unilateral action, are rattling business leaders and raising concerns about economic disruption across North America. Mexico is the world’s largest silver producer and home to many U.S.- and Canadian-listed miners, making any deterioration in U.S.-Mexico relations a direct risk to supply chains and investor confidence. Tariff threats and geopolitical tension could strain the United States Mexico Canada Agreement framework, amplify trade uncertainty, and inject volatility into silver markets, where restricted supply and elevated demand have already driven sharp price moves.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2025):

Frontier Group Holdings

Cathay Pacific

Grupo Aeroportuario del Pacífico

Delta Air Lines

Alaska Air Group

American Airlines

Copa Holdings

General Dynamics Corp.

Ralph Lauren

Volkswagen

Royal Caribbean

Tesla

BMW

Centerra Gold

Hudbay

Newmont

Endeavour Mining

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits