Key takeaways

- We expect that yields should continue to remain attractive this year, but we have highlighted five risks that could come into play.

- The risks include: relative yields returning to post-pandemic averages; federal funding issues for state and local governments; lower demand for munis; an economic slowdown; and market concerns around Federal Reserve independence.

- To help navigate and position for these risks, we think investors should focus on higher-rated issuers and an intermediate-term duration.

We have a positive outlook for the muni market in 2026 but there are risks to that outlook. In general, we think that munis offer a good balance of attractive tax-adjusted yields and stable credit quality. We expect positive total returns for the broad muni market this year driven by a combination of elevated starting yields and positive economic growth. Although it's not our base case, below are five risks that could shake up the muni market this year and derail our positive outlook.

1. Relative yields returning to their post-COVID-19 averages

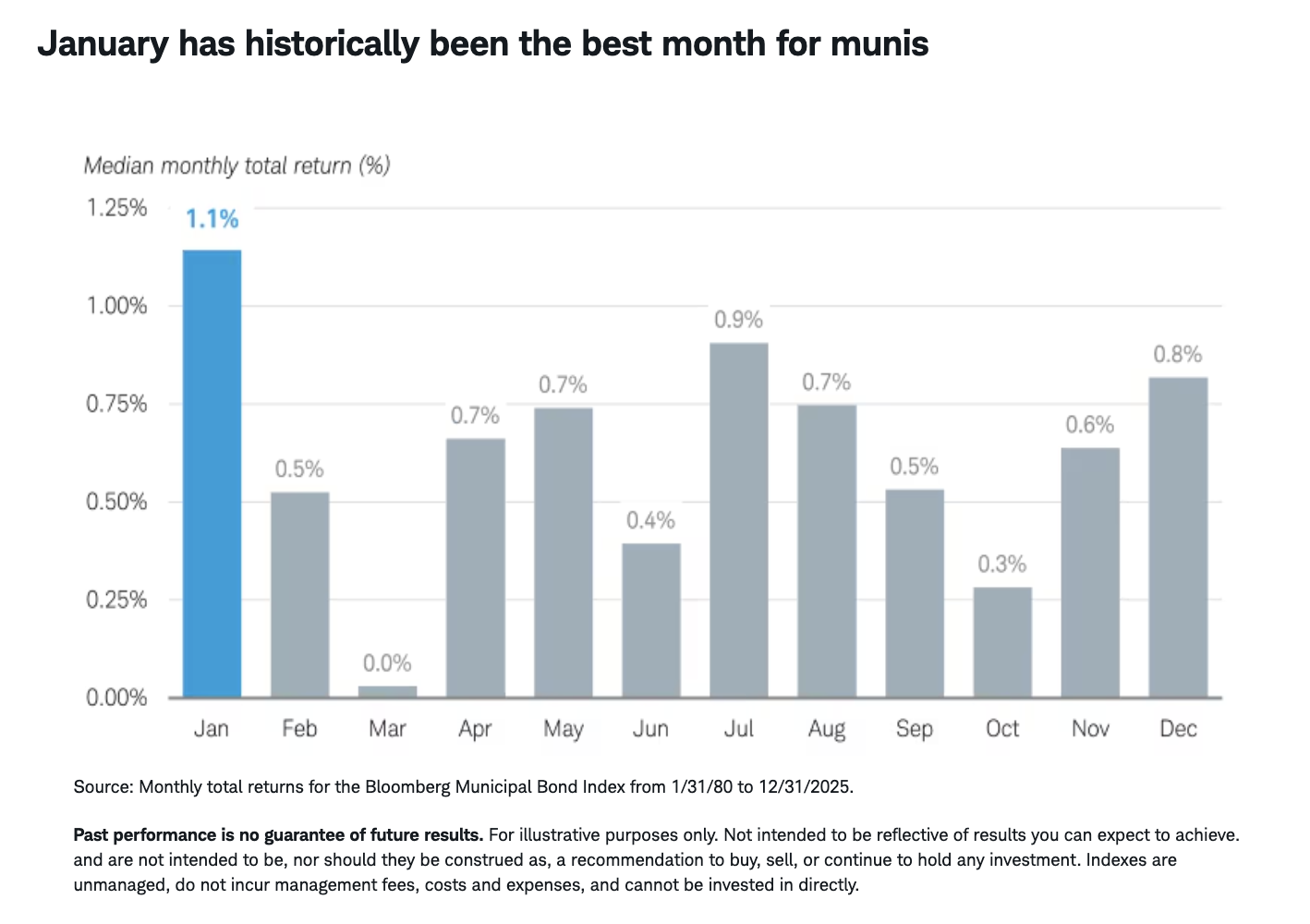

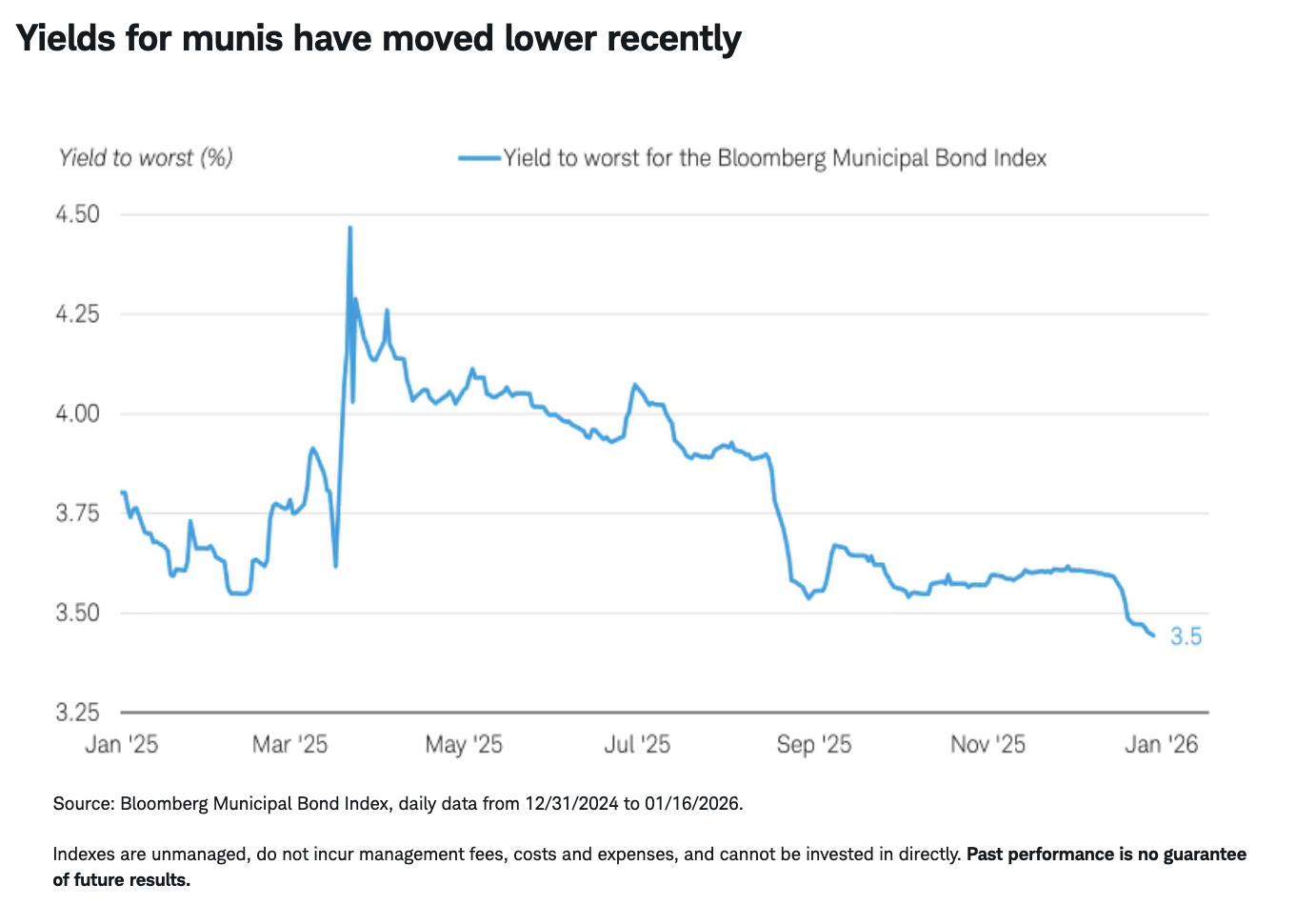

The municipal bond market is off to a strong start this year with the Bloomberg Municipal Bond Index posting a return of 0.9% through January 16, 2026. Munis are outperforming all other major fixed income asset classes that we track. Historically, January has been the best month for total returns because of a mismatch between supply and demand. (However, keep in mind that past performance is no guarantee of future results.) Many munis pay interest or principal payments in December, and investors typically redeploy that capital in January which pushes prices higher and yields lower.

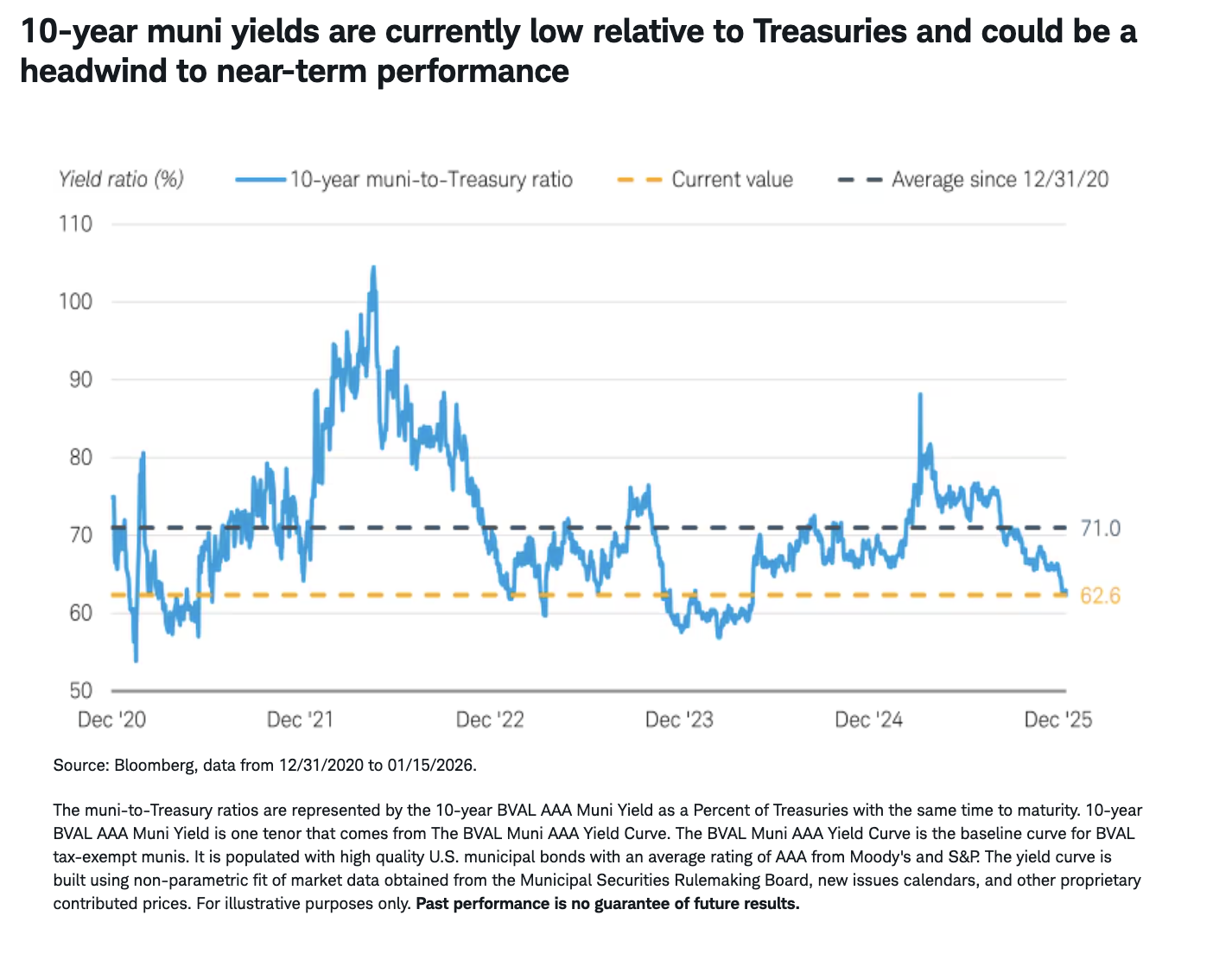

The downside of the strong start to the year is that it has pulled yields lower relative to Treasuries. In fact, the 10-year muni-to-Treasury ratio is now at its lowest level over the past year. The muni-to-Treasury ratio is a ratio between the yield on a generic index of AAA rated munis relative to Treasuries of equal maturities before adjusting for taxes. If muni-to-Treasury ratios were to rise, total returns for munis would trail Treasuries and potentially other comparable fixed income investments.

2. Further strain on the relationship between federal and state and local governments

The financial relationship between states, local governments, and the federal government is complicated. Many programs are funded by the federal government but administered by states. For example, Medicaid, Supplemental Nutrition Assistance Program (SNAP, or food stamps), some housing and community development programs, and Unemployment Insurance are all programs that the federal government funds but states administer. During a speech on January 13, 2026, in Detroit, President Donald Trump said that the administration is planning to halt federal payments to sanctuary cities and or states with sanctuary cities. This is not the first time that the federal government has proposed halting payments to some states and local governments. However, due to the complicated relationship between states and the federal government and the laws related to those funds, halting payments can be legally difficult.

As it relates to the municipal bond market, generally speaking, the money that is used to pay debt service doesn't come from federal funding but instead from other sources such as taxes or usage fees. If the administration is successful in halting payments, a state could choose to make up the difference in the lost funds but is generally not legally obligated to do so. If a state made up the difference, it could put financial pressure on the state's budget, but we believe most states could manage through this temporary distribution. Municipal balance sheets are generally strong, with reserves near record highs, and revenues continue to hold up well.

The risk to the market is that the relationship between the federal and some state and local governments worsens and funds are withheld for an extended period, resulting in fiscal stress. This would likely pose a greater risk to smaller issuers with weaker balance sheets and more economically sensitive revenue streams. Generally speaking, these types of issuers tend to have lower credit ratings.

3. Slowdown in demand

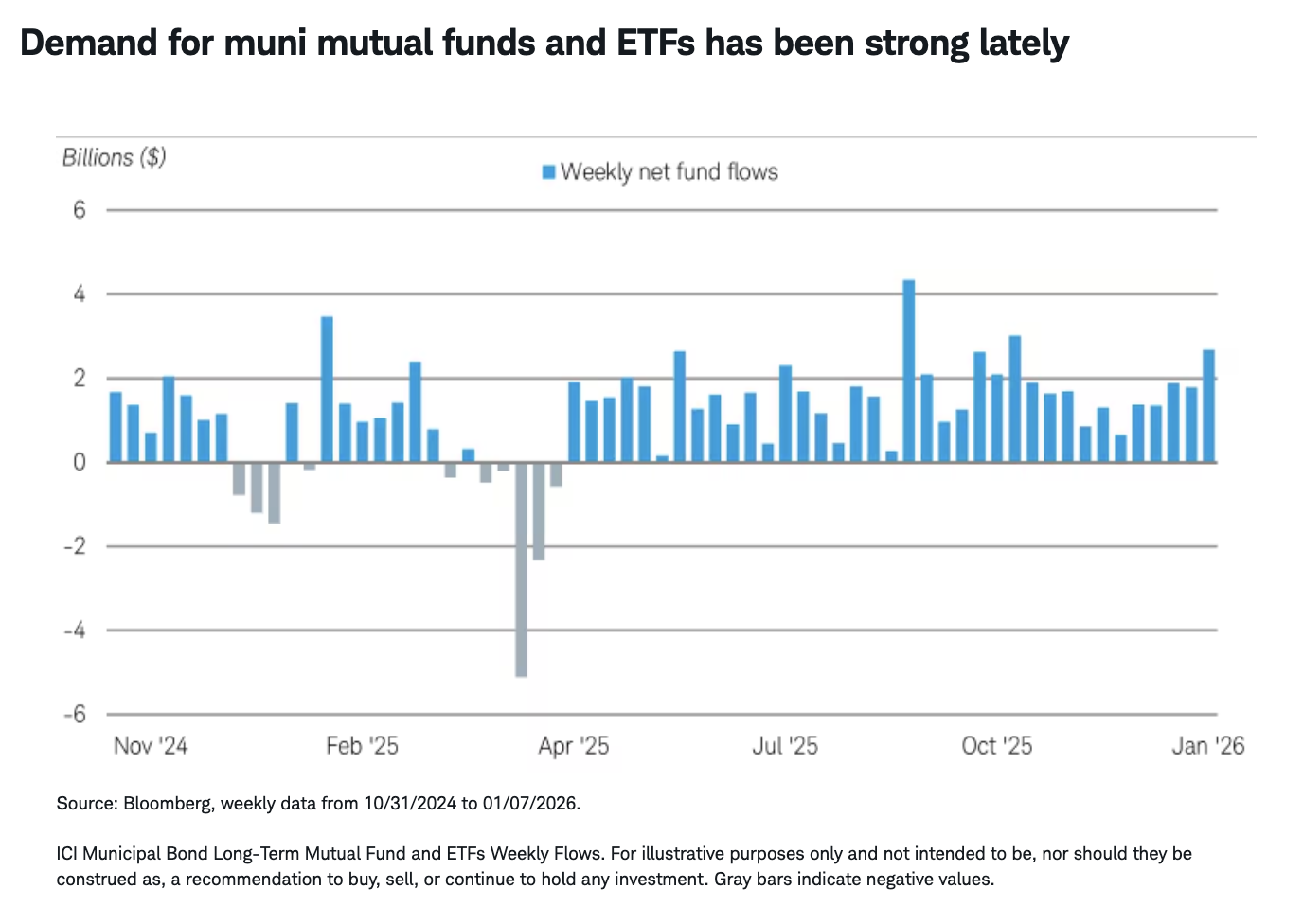

One of the main themes in our 2026 outlook was that issuance should remain elevated. This could be a headwind for total returns if demand doesn't keep up. So far, demand has been positive, as evidenced by flows into municipal bond mutual funds and exchange-traded funds (ETFs). Muni mutual funds and ETFs have reported positive inflows for 37-straight weeks which is tied for the fourth-longest streak of inflows dating back to the beginning of 2013. We believe that demand has been strong for a few different reasons. Yields, especially when adjusted for taxes, are attractive, total returns have been positive, and there haven't been concerns over credit quality. If any of those three factors begin to fade, investors may begin to shy away from municipal bonds and total returns may suffer.

4. Slowdown in the economy

Some municipal bonds have payments that are backed by economically sensitive revenue sources. For example, income and sales tax revenues make up the bulk of revenues for most states. If the economy falters, these revenue sources could come under pressure, but there is often a lag between the economy and a slowdown in revenues. The good news so far is that the economy, in aggregate, has been holding up relatively well. For example, the consensus estimate for real gross domestic product, or GDP, in 2026 is 2.1% according to Bloomberg. Although the economy is expected to continue to hum along this year, there could be an unexpected surprise or two that derails growth.

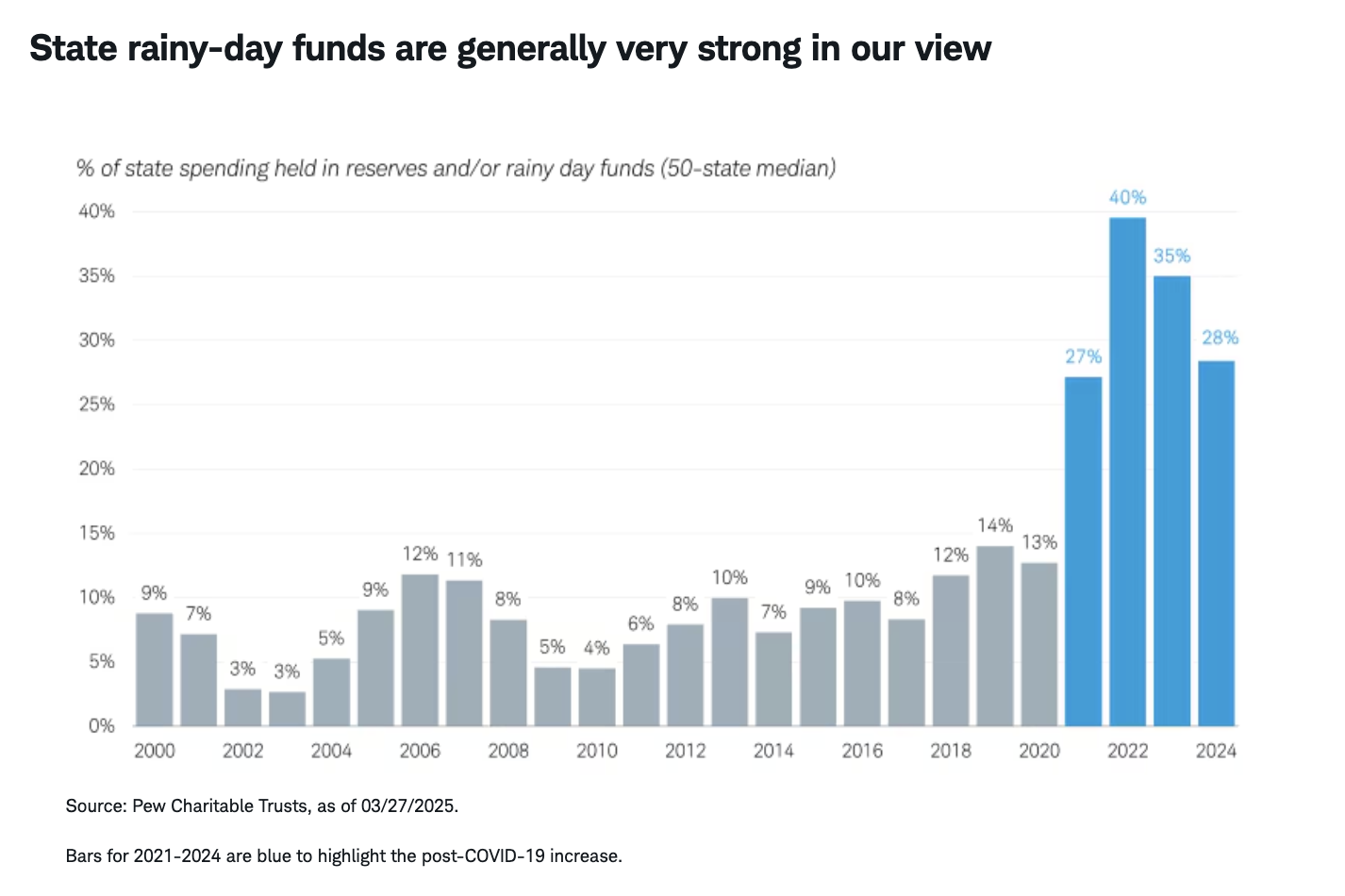

If the economy slows, municipalities with more economically sensitive revenue streams would likely face greater pressures. These tend to be issuers with lower credit ratings in general. In aggregate, we don't view an economic slowdown as a larger risk to the general market because most issuers don't have revenue streams that are economically sensitive. In fact, roughly seven out of the 10 issuers in the Bloomberg Municipal Bond Index are either AAA/Aaa or AA/Aa rated, which are the top two rungs of investment grade credit quality. Additionally, many states and local governments have built up their liquidity positions to very healthy levels, in our view. On average, for every $100 that a state spends, they have $28 in their rainy-day funds. This is down from a peak of $40 but well above the average from 2000 through 2022, as illustrated in the chart below. A rainy-day fund is akin to a savings account that a state can tap into, with restrictions, if necessary.

5. The potential loss of Federal Reserve independence

The uncertainty over the next chairperson and the recently reported news of a potential criminal investigation around the Federal Reserve aren't muni-specific risks but they could impact the muni market. Concerns around Fed independence could raise the risk that inflation would accelerate which could lead to higher longer-term bond yields. So far, longer-term bond yields haven't reacted much to the headlines. The yield to worst for the Bloomberg Municipal Bond Index has held in a tight range since the beginning of the year and volatility has been muted.

If yields were to break out to the upside of this range, either due to the market perceiving a lack of Fed independence or another issue, it could result in negative total returns for munis–especially longer-term munis which are more sensitive to changes in interest rates than shorter-term munis.

What to do now

Although we think the muni market should have a pretty good year, it's not without risks. To help navigate and position for those risks, we think investors should focus on higher-rated issuers and an intermediate-term duration. For the average muni investor, a duration of about six to seven years is a good starting point. Higher-rated issuers tend to have larger liquidity positions and more stable revenue sources and can therefore better manage a slowdown in revenues and other unforeseen credit issues.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The securities and investment strategies mentioned are not suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

Individual situations will vary. Not intended to be reflective of results you can expect to achieve.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate this risk.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Charles Schwab & Co., Inc. does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

This information is not a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager, Estate Attorney) to help answer questions about specific situations or needs prior to taking any action based upon this information.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Charles Schwab

Read more commentaries by Charles Schwab