It can sometimes be hard to tell whether the US housing market is hot or cold. Currently, existing-home inventory is tight and prices are stable—indicators of a hot market—while sales volume is down and home price appreciation has slowed. So, what’s the temperature? We believe the housing market is solid, and a confluence of market forces and public policy should support mortgage-backed securities (MBS).

Public Policy Could Increase Demand for Agency Mortgages

The potential catalysts for MBS begin with housing initiatives coming from the White House. In an effort to lower mortgage rates, President Trump in January ordered government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac to purchase $200 billion of agency MBS. These securities’ spreads—their yield advantage over Treasuries—soon tightened.

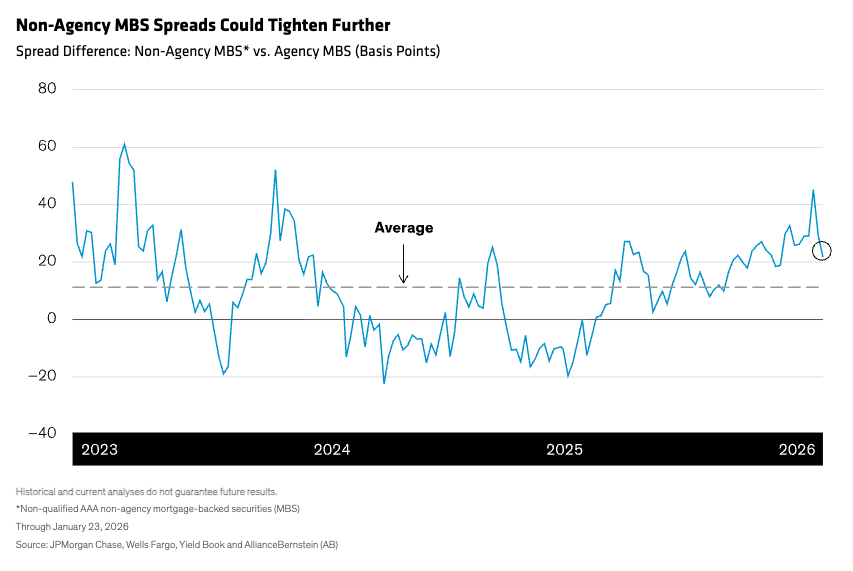

But the spillover effect has yet to fully reach related sectors. For now, the spread between non agency and agency MBS is hovering above its historical average (Display). Over time, we expect non agency spreads to tighten as investors capitalize on this dislocation. In fact, non-agency MBS have some upside potential, in our view.

The administration also has floated other ideas aimed at lowering mortgage rates and making homebuying more accessible. These include introducing mortgage prepayment penalties, allowing borrowers to transfer an existing mortgage to a different residence, permitting retirement funds to be used for home purchases, and increasing the capital gains exclusion for home sales.

If implemented, these initiatives could provide a tailwind to the housing market and, by extension, MBS. But we question how much housing policy will improve affordability—largely due to the so-called “lock-in” effect.

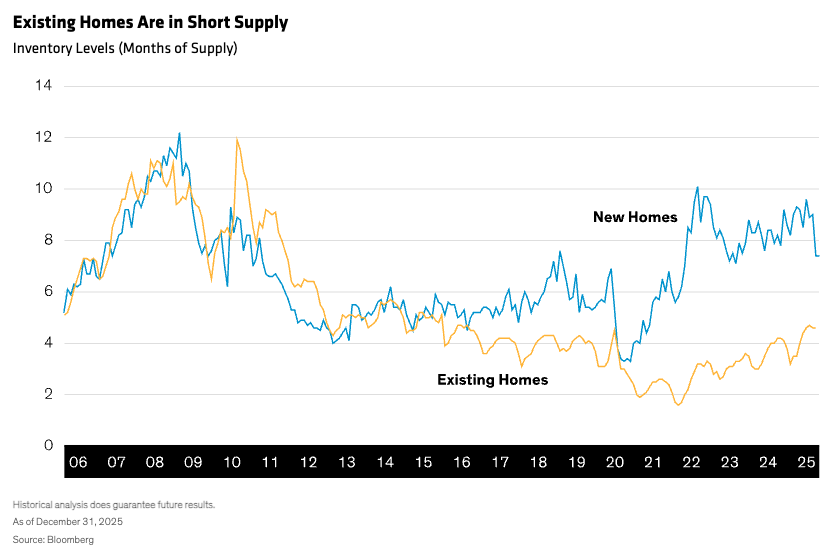

Many homeowners are staying put because they locked in mortgages with ultra low fixed rates during the pandemic. With mortgage rates so low, few homeowners with low-rate mortgages have been motivated to sell, which is restricting existing home inventory (Display) and supporting prices.

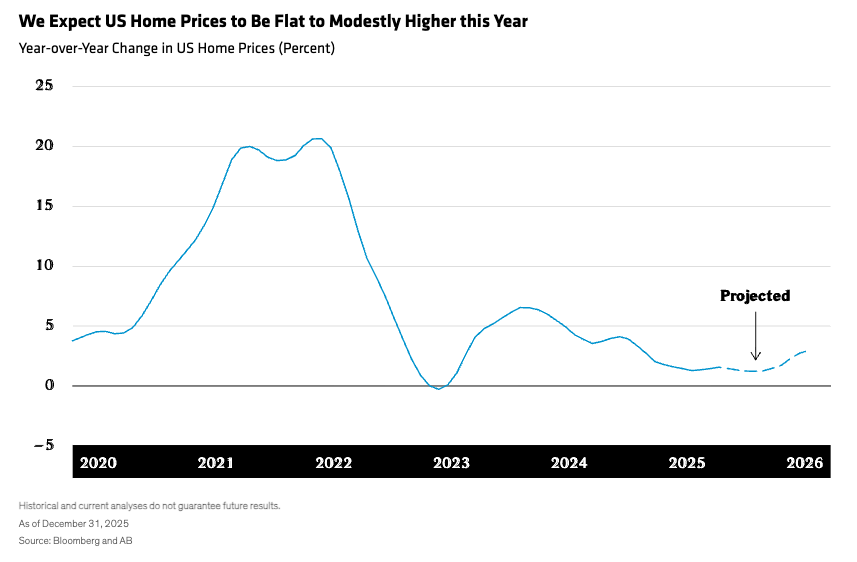

Partly for this reason, we expect home prices to be flat to marginally positive in 2026 (Display).

Strong fundamentals may not do much to improve home affordability, but they could be a boon for MBS. Elevated home prices tend to increase homeowners’ equity in the form of lower loan-to-value ratios, which reduces the probability and severity of defaults.

In addition, low rates on existing mortgages help limit refinancings and prepayment risk. Although we expect some increased prepayments, the majority of borrowers are doing so at rates below 5%, and we don’t foresee mortgage rates returning to those levels anytime soon.

Timing is the wildcard. If mortgage rates come down and affordability increases, home inventory levels could move higher for a time. But as the market loosens and previously sidelined homeowners become buyers again, we would expect inventory levels to tighten, which should support home prices—and MBS.

Of course, rates aren’t the only variable. Homebuilders have scaled back construction of both single-family and multifamily homes, a move that should help ease any buildup in supply.

Fed Easing Increases the Need for Income

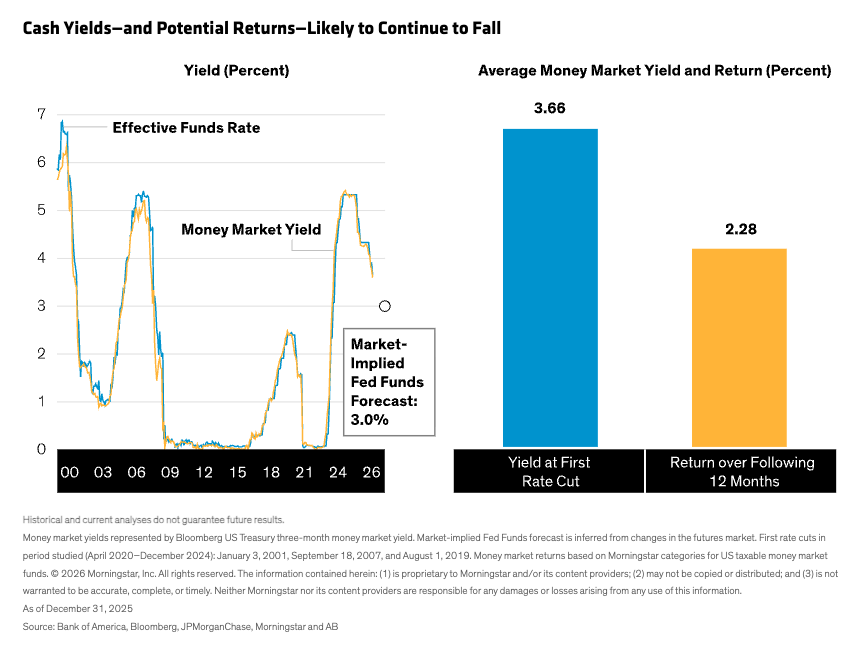

Monetary policy could also benefit MBS, in our analysis. On the heels of 175 basis points in rate cuts this cycle, cash rates have drifted to just above 3.5%. With more cuts on the way—albeit at a potentially slower pace—we expect cash yields to fall to closer to 3%.

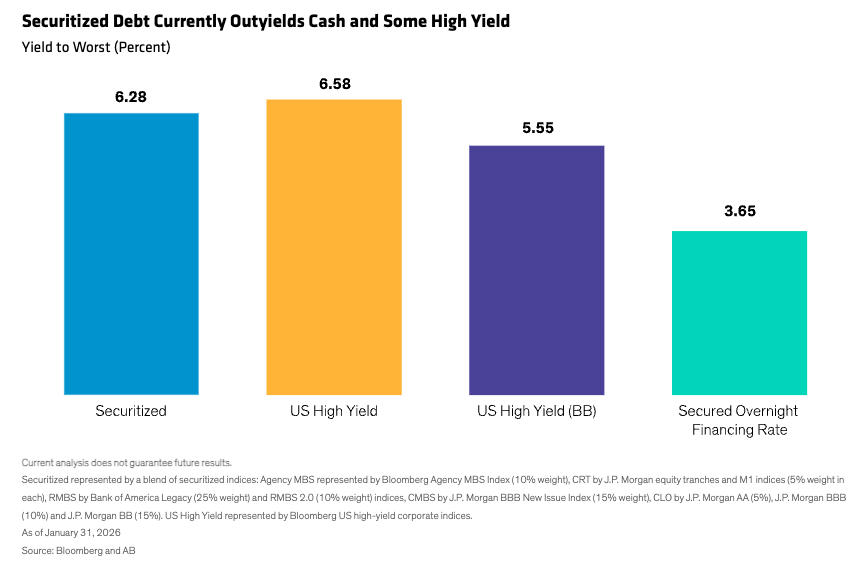

That could put income-oriented investors in a bind. During Fed cutting cycles, cash returns are typically lower than starting yields (Display), necessitating a more reliable source of income.

In our view, this is where MBS can shine. MBS outyield cash in most any market environment and even compare favorably with higher-risk assets like high-yield bonds (Display). And unlike with cash, starting yields on bonds tend to be a reliable indicator of future return over the medium term.

How many of the Trump administration’s proposed housing policies become law remains to be seen. But for the time being, we believe the confluence of public policy and strong housing fundamentals provides a favorable tailwind for MBS investors.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein