Airlines Are Printing Record Numbers. Here’s Why the Growth Story Is Just Getting Started

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs you know, I’ve been watching the travel industry for a long time, and the data right now is telling a compelling story that’s hard to ignore. Despite the negative headlines, rising oil prices and a healthy dose of political noise, global travel is running at full throttle. By virtually every meaningful metric, the runway looks even longer to me.

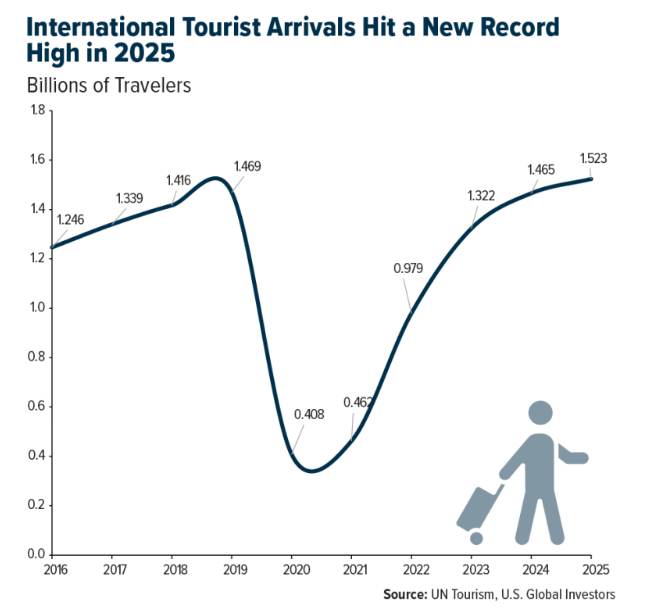

According to the UN World Tourism Organization, an estimated 1.52 billion international tourists traveled the world in 2025. That’s nearly 60 million more than the year before, representing 4% growth, and it marks a return to the steady, pre-pandemic growth trend of 5% annually that the industry enjoyed between 2009 and 2019.

The recovery is real, it’s broad-based and it’s gaining momentum.

Asia-Pacific on Track to Surpass Europe as Largest Travel Market

The World Travel & Tourism Council projects the industry will contribute a record $11.7 trillion to the global economy in 2025, equivalent to 10.3% of world GDP. International visitor spending is forecast to hit $2.1 trillion, surpassing the previous all-time high of $1.9 trillion set in 2019.

Looking further out, a landmark study by Google and Alvarez & Marsal projects that by 2050, international travel will double to roughly 3.5 billion trips annually, generating $6 trillion in spending. That’s $4.2 trillion in incremental value created over the next 25 years.

Asia is the engine powering much of this long-term growth. The Asia-Pacific region (APAC) is in the middle of the largest middle-class expansion in human history. By 2035, APAC will be home to 3.2 billion of the world’s projected 5 billion middle-class consumers. These are people who aspire to see the world, and they increasingly have the means to do it.

APAC, in fact, is on track to surpass Europe as the world’s largest travel source market. China’s Spring Festival travel season is already offering us a preview: flight bookings for the 2026 festival surged an astounding 400% year-over-year.

Record Revenues for the Big Four Airlines

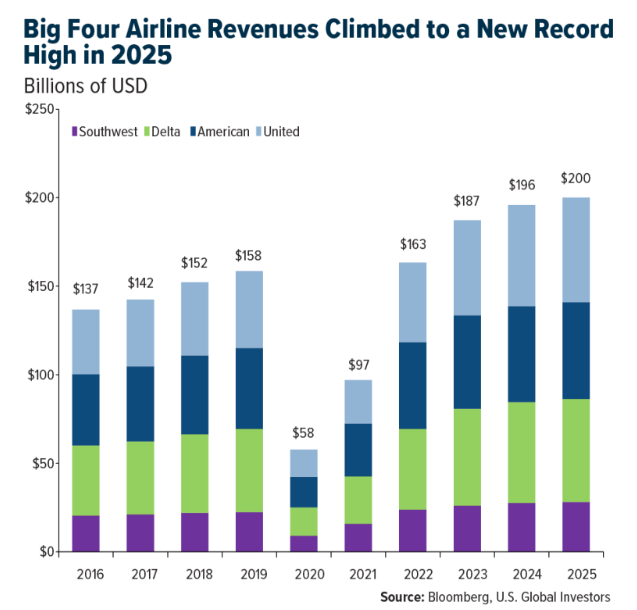

You don’t have to take the macro data at face value. Just look at the earnings reports coming out of the major U.S. carriers.

Delta, for instance, generated a record $58.3 billion in 2025 revenue. United hit $59.1 billion, also a record. American delivered record fourth-quarter revenue of $14 billion. And Southwest, which spent 2025 executing its most ambitious business transformation in company history—introducing bag fees, assigned seating and extra legroom options—reported record fourth-quarter passenger revenues of $3.8 billion, up 7.6% year-over-year.

Premium demand in particular is outperforming. Travelers are trading up, spending more per trip and showing remarkable resilience in the face of economic headwinds.

Europe’s tourism sector illustrated this perfectly. While international arrivals grew a healthy 3.2% in 2025, spending grew nearly 10%. That gap should tell investors about the quality of demand right now. People aren’t just showing up… they’re showing up and opening their wallets.

Short-Term Turbulence: Iran and Oil

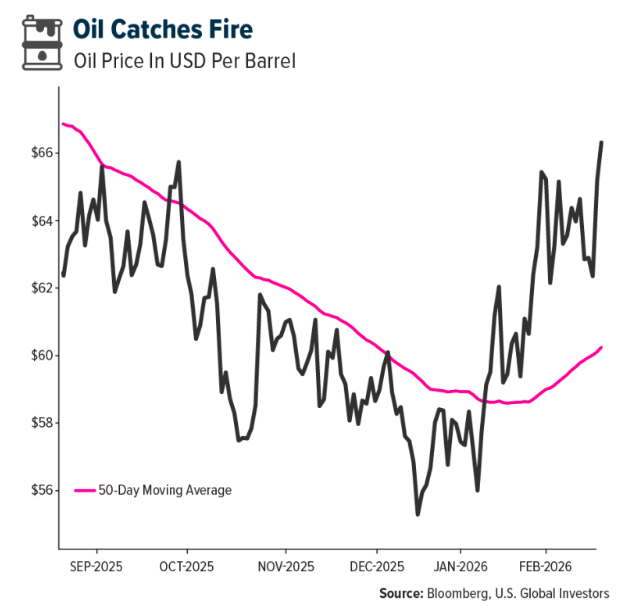

I’d be remiss if I didn’t acknowledge the near-term risks. The most pressing, as I write this, is oil. West Texas Intermediate (WTI) crude is up more than 16% year-to-date, and with President Donald Trump signaling a potential military decision on Iran within days, oil markets are pricing in a meaningful risk premium. For airlines, where fuel costs can represent 20% to 40% of total operating expenses, a prolonged oil spike could be

History tells us, though, that geopolitical shocks to oil prices tend to be temporary in nature. Travel demand has proven remarkably durable through past crises, and the structural drivers—the middle-class expansion, the rising connectivity, the pent-up desire to explore—don’t evaporate because of a short-term spike in crude.

I think smart investors know to distinguish between cyclical noise and secular trends. And right now, the secular trend in travel is unmistakably upward.

A Word on the Plunge in Canadian Travel to the U.S.

Canadian visits to the U.S. fell roughly 20% between January and October 2025, while January 2026 data from Statistics Canada shows Canadian trips to the U.S. down a staggering 28% compared to 2024 levels. A Blue Cross survey found that 76% of Canadians now say they are less likely to visit the U.S., a direct result of some of President Trump’s political rhetoric directed at our northern neighbors.

As a proud Canadian-born American, I’ve long believed that former Prime Minister Justin Trudeau’s economic policies hurt Canada, and I wasn’t alone in that view. But there’s a huge difference between criticizing a government’s policies and treating an entire nation and its people as adversaries.

Canadians are among the most loyal visitors, trading partners and friends the U.S. has ever had. Alienating them is a self-inflicted economic wound, I believe, and the numbers are beginning to prove it. The U.S. Travel Association estimates that Canadian visitors generated $20.5 billion in spending and supported 140,000 American jobs in 2024. That’s not a trivial number to wave away.

The Investment Thesis Remains Intact

Despite the near-term volatility, I remain firmly constructive on the travel and tourism sector as a long-term investment opportunity. The macro tailwinds are among the strongest I’ve seen in my career: a once-in-a-generation middle-class expansion across Asia, record global tourism volumes, airline earnings at all-time highs and a pipeline of growth stretching out to mid-century.

U.S. hotel investment hit $24 billion in transaction volume in 2025—up 17.5% year-over-year—signaling that institutional capital is moving confidently into the sector. The 2026 FIFA World Cup, hosted across major U.S. cities, is a near-term catalyst that analysts project could drive mid-double-digit revenue-per-available-room growth in host markets. Europe is forecasting 6.2% arrival growth in 2026, with long-haul travel expected to surge 9%.

The short-term risks (elevated oil prices, the Iran situation, U.S.-Canada relations) are real and deserve monitoring. But they don’t change the fundamental trajectory of an industry that’s growing larger, more global and more economically significant with each passing year. For patient investors with a long-term appetite, that trajectory is the story worth focusing on.

Wheels up!

Interested in investment opportunities in the commercial airlines sector? Send an email to [email protected] with the subject line AIRLINES.

Airlines and Shipping

Strengths

- Boeing secured major orders from Vietnamese carriers, including a record commitment for up to 40 787-9 Dreamliners from Sun Phu Quoc Airways and a finalized order for 50 737-8 MAX jets from Vietnam Airlines. The wide-body deal marks Vietnam’s largest ever, while the 737 MAX aircraft will support Vietnam Airlines’ domestic and regional expansion, with both models offering 20–25% fuel efficiency improvements over older jets.

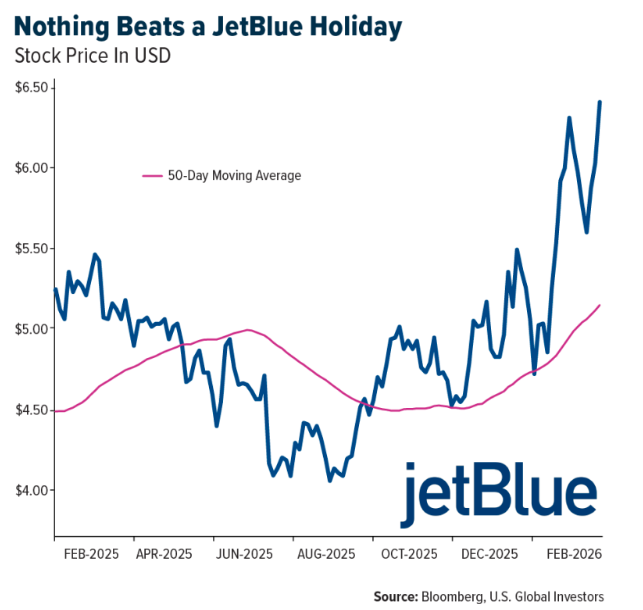

- JetBlue Airways said first-quarter demand momentum remains “really strong,” adding that it is “super pleased” with trends as it works toward breakeven or better operating margins—its top priority to enable positive free cash flow in 2017. The carrier also said the impact from East Coast storm Fern was de minimis and will not affect its annual guidance, speaking at the Barclays 43rd Annual Industrial Select Conference.

- The Government of Israel has approved the construction of a new international airport in the Ziklag area of the Negev. It will be developed alongside another facility in Ramat David, with the aim of easing congestion at Ben Gurion International Airport and supporting economic growth, despite earlier security concerns about its proximity to Gaza.

Weaknesses

- Airbus SE shares declined after the company guided for 870 aircraft deliveries in 2026, below expectations, citing significant engine shortages from Pratt & Whitney that are slowing A320 production ramp-up plans. Although 2025 revenue, profit, and orders rose, the weaker delivery outlook and reduced A320 rate target for 2027 overshadowed the results and pressured the stock.

- Delta Air Lines Flight 2557, operated by a Boeing 717, returned to Houston Hobby shortly after departure when a passenger caused a disturbance near the cockpit, prompting an emergency landing and arrest, with no injuries reported.

- The Danish Maritime Authority has detained a sanctioned containership formerly known as Cerus, and later Nora, linked by the United States Department of the Treasury to a network allegedly tied to Mohammad Hossein Shamkhani, son of Ali Shamkhani, after authorities found discrepancies in its claimed registry and certifications.

Opportunities

- CMA CGM has ordered six LNG powered containerships from Cochin Shipyard Limited, its first such order in India, while launching an R and D hub with Capgemini, deepening its presence in the country across shipbuilding, crewing, infrastructure, and digital innovation.

- Embraer and Mahindra Group plan to establish a maintenance, repair, and overhaul facility in India for the C 390 Millennium following the aircraft’s selection in the Indian Air Force’s Medium Transport Aircraft program.

- DHL Group, a unit of Deutsche Post AG, plans to expand its Life Sciences and Healthcare business by launching a dedicated Airfreight Cold Chain Network to transport temperature sensitive medicines, vaccines, and advanced therapies. The network will initially connect major hubs in Brussels and Cincinnati, reducing reliance on third party carriers, with additional routes planned across Europe, the Middle East, Asia, and Latin America.

Threats

- The Danish Maritime Authority has detained a sanctioned containership formerly known as Cerus and later Nora, linked by the United States Department of the Treasury to a network allegedly tied to Mohammad Hossein Shamkhani, son of Ali Shamkhani, after authorities found discrepancies in its claimed registry and certifications.

- Russian airstrikes on Ukraine’s Black Sea ports in the Odesa region late last year cut export capacity by up to 30%, damaged civilian bulk vessels, and disrupted grain and iron ore shipments, despite Kyiv maintaining operations along its coastal maritime corridor.

- A JetBlue flight departing Newark Liberty International Airport for West Palm Beach was forced to return shortly after takeoff due to engine failure, with passengers evacuated via slides after smoke was reported in the cockpit, temporarily halting airport operations before reopening later that evening.

Luxury Goods and International Markets

Strengths

- On Wednesday, Viking Holdings Ltd, known for its river cruise business, saw its share price rise sharply over the past year, reflecting strong investor interest. The company also announced new 2027 itineraries on the Mississippi and Ohio rivers, with bookings now open for voyages such as the 15-day Bayous, Blues and Bluegrass and eight-day Mississippi and Ohio River Explorer routes.

- Europe’s February preliminary Manufacturing PMI came in at 50.8, beating expectations of 50.0 by 0.8 points and rising from 49.5 in January. This marks a return to expansion territory, signaling improving manufacturing activity and stronger momentum than markets had anticipated.

- Moncler, the Italian luxury goods maker, was the best performing name in the S and P Global Luxury Index over the past five days, with shares jumping after the company reported strong earnings and better than expected revenue growth, driven by solid demand in Asia and the Americas.

Weaknesses

- U.S. economic growth slowed sharply in Q4 2025, with GDP rising just 1.4% annualized, well below expectations of around 2.8%. The weaker than expected result points to a softer end to the year, driven by slowing consumer spending and reduced government outlays, which weighed on overall economic momentum.

- Tesla recently lowered prices on its Cybertruck lineup, introducing a new dual motor all wheel drive model priced at about 59,990 dollars, the lowest entry price yet, which is roughly 20,000 dollars below prior base prices. At the same time, the highest end Cybertruck model was reduced to about 99,990 dollars, down from around 114,990 dollars previously.

- Rivian Automotive, the electric vehicle maker, was the worst performing name in the S and P Global Luxury Index over the past five days, with shares declining amid continued concerns around pricing dynamics, demand visibility, and competitive pressure in the EV market.

Opportunities

- Lunar New Year celebrations in China began on Tuesday, February 17, 2026, marking the start of the Year of the Fire Horse. It is one of the most important holidays in China and traditionally drives a surge in consumer spending, particularly on luxury goods. The celebration is closely tied to gift giving, with consumers purchasing high end fashion, jewelry, watches, and beauty products as symbols of prosperity and goodwill.

- Toll Brothers reported strong results, driven in large part by continued demand from wealthier buyers. In its most recent quarter, the company delivered homes at an average selling price of approximately $977,000, significantly higher than the broader U.S. housing market’s median sales price of around $400,000. This premium pricing underscores Toll Brothers’ positioning toward more affluent customers.

- Luxury hotels are benefiting from growing demand for luxury bookings as affluent travelers return to premium stays and push occupancy and room rates higher across major markets. This trend is lifting performance for large operators such as Hilton Worldwide, InterContinental Hotels Group, and Accor. Many of these companies have also announced share buyback programs, with Hilton increasing its repurchase plan to about $4.6 billion and InterContinental Hotels Group launching a $950 million buyback to return capital to shareholders.

Threats

- Rising geopolitical tensions surrounding a potential escalation involving Iran have pushed oil prices higher, increasing concerns across global markets. Higher oil prices raise fuel and operating costs for airlines and cruise operators, while also pressuring consumer travel demand through higher transportation expenses. Travel-related stocks may experience further pressure if international tensions escalate.

- LVMH shares have been volatile, with the stock experiencing significant swings after cautious outlook comments from management and slower demand signals, including softer sales momentum in China than investors had hoped, which has dampened confidence in the luxury recovery. This volatility has weighed on LVMH’s share performance relative to broader markets.

- Kering has faced pressure as well, in part due to weak sales performance in key brands and operational adjustments like store closures, which signal challenges around maintaining volume and profitability growth.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was wheat, up ~6%, due to dry Midwest weather that could hurt crop yields and potential supply disruptions from Ukraine. WTI crude oil rose ~5.5% and held near a six-month high of $67 per barrel as supply risks rattled energy markets, including President Trump’s 10-to-15-day ultimatum to Iran and live-fire drills by Iran’s Revolutionary Guard that partially closed the Strait of Hormuz. Russian seaborne crude exports have fallen to approximately 2.8 million barrels per day in February from 3.8 million in December, driven by refinery drone strikes, Baltic port ice conditions, and U.S. sanctions, with Rystad Energy projecting a potential further cut of 300,000 barrels per day by spring.

- Lundin Mining and BHP’s Vicuna District Preliminary Economic Assessment outlines one of the most consequential mining projects in recent history, with a 70+ year mine life and peak annual production of approximately 800,000 tonnes copper-equivalent, including 500,000 tonnes of copper, 800,000 ounces of gold, and 20 million ounces of silver, representing a genuinely generational asset. The deal’s NPV sensitivity is striking, with the base case at $9.5 billion jumping to $28.8 billion at spot prices, though today’s ~3% pullback in Lundin shares reflects broader metal weakness and investor caution given the phased complexity of moving from Josemaria through the Filo components toward first production in 2030.

- Uranium market fundamentals are tightening as Cameco and Kazatomprom release production figures showing a structural supply squeeze. Cameco’s 2025 output of 21.0 million pounds exceeded guidance but was 10% below 2024 levels, while Kazatomprom cut 2026 targets by ~10%, removing roughly 8 million pounds, or 5% of global supply. With the U.S. accelerating reactor deployment and awarding HALEU enrichment contracts, the long-term uranium contracting cycle is poised for a major reset.

Weaknesses

- Natural gas prices have continued to sell off sharply, down ~6% this week, after inclement winter weather earlier this year briefly drove the commodity as high as $7/MMBtu, with demand uncertainty now weighing on the market as seasonal tailwinds fade and supply remains robust. Adding to the murky demand outlook, Bloomberg reported that Gentry Beach — a U.S. investor with ties to the Trump family — has struck an early-stage deal with Russia’s sanctioned Novatek to develop LNG in Alaska, a project facing steep regulatory and legal hurdles given that Novatek has been subject to U.S. sectoral energy sanctions since 2014, leaving the market questioning whether new domestic LNG infrastructure demand will materialize at all.

- Hudbay Minerals declined over 6% after reporting Q4 adjusted EPS of 22 cents, well below the 39-cent consensus, as copper production fell 24% year-over-year and revenue missed expectations at $733 million versus $750 million estimated. The company guided for a 5% increase in copper production for 2026 but expects lower gold output, while analysts maintain 19 buy ratings against one hold.

- Lithium carbonate futures fell roughly 9% to around CNY 138,000 per tonne after hitting a two-year high of CNY 180,000 in January. The pullback reflects slower demand recovery and sentiment-driven trading, while structural headwinds remain from high-cost supply restarts, potential Australian mine reactivations, and the risk that supply returns faster than demand can absorb.

Opportunities

- John Deere posted a strong Q1 fiscal 2026 earnings beat, reporting EPS of $2.42 versus a $2.02 consensus and revenues of $9.61 billion, up 13% year-over-year and well above the $7.59 billion forecast, as construction and small agriculture equipment demand drove higher shipment volumes. CEO John May called 2026 “the bottom of the current cycle,” raising full-year net income guidance to $4.5–$5.0 billion and projecting 15% net sales growth for Small Agriculture & Turf and Construction & Forestry. Large agriculture remains pressured by weak crop prices and $1.2 billion in estimated tariffs, but broad equipment demand and strengthening order books signal a recovery into 2027.

- Rio Tinto CEO Simon Trott said the company’s U.S. focus is advancing the Resolution copper project in Arizona with BHP, noting a Ninth Circuit decision on the court injunction is expected soon. Trott highlighted engagement with the U.S. government on broader opportunities and underscored the strategic potential of the Kennecott copper operation in Utah for critical mineral production.

- India’s power grid modernization and energy storage are key investment targets, with an estimated $101 billion needed for transmission upgrades to integrate growing renewable capacity. Development finance institutions, including British International Investment, are shifting focus from generation to distribution, as renewables and hydro now exceed thermal capacity, though coal still generates roughly 75% of electricity.

Threats

- Brent crude rose sharply as traders weighed the risk of a potential U.S. military campaign against Iran, which could disrupt flows through the Strait of Hormuz, against tentative progress in nuclear talks, with Iran offering to transfer enriched uranium to Russia and suspend enrichment for three years. Oil is holding near six-month highs above $71 as Trump’s 10-to-15-day ultimatum and the deployment of two U.S. carrier strike groups raise the specter of supply disruptions. U.S.-brokered Russia-Ukraine peace talks collapsed after just 90 minutes in Geneva, adding further geopolitical uncertainty.

- A military escalation with Iran could affect commodities beyond crude oil, as Iran produces roughly 17–20% of global pistachios, the world’s second-largest after the U.S., and disruption would tighten global tree nut supplies already strained by U.S. and Turkish harvests. The U.S. and Iran together control about 70% of global pistachio exports, and any supply shock amid surging demand from the Dubai chocolate trend and broader snack nut consumption would likely drive sharp price dislocation.

- Russia’s oil drilling fell 3.4% in 2025 to a three-year low of about 29,140 kilometers of production wells, with December activity down 16% year-over-year due to sanctions, Urals discounts, and a stronger ruble reducing profitability. Separately, Trump’s $33 billion Ohio gas mega-project, billed as the largest U.S. gas power plant at 9.2 gigawatts, lacks binding commitments from Japanese investors, has not been filed with Ohio’s power siting board, and was reportedly unknown to grid operator PJM. The gap between announcement and execution on major projects adds uncertainty to U.S. power supply and highlights how policy-driven deal-making can obscure market fundamentals.

Bitcoin and Digital Assets

Strengths

- XRP Ledger (XRPL) has strengthened its institutional appeal by activating the XLS-81 (Permissioned DEX) and XLS-85 (Token Escrow) amendments. These tools allow banks and brokers to trade in members-only venues while meeting KYC/AML requirements, attracting major players and expanding stablecoin use.

- ProShares’ entry into the stablecoin ecosystem with the IQMM ETF provides the first SEC-regulated vehicle meeting the GENIUS Act’s 1:1 Treasury backing requirement. This move standardizes reserves under professional custody, enhancing transparency, solvency, and safety for a market projected to reach $3 trillion by 2030.

- Despite Bitcoin’s recent 50% price crash, Ledn closed a $188 million bond deal backed by Bitcoin loans. Its automated liquidation system protected bondholders, demonstrating that Bitcoin-backed debt can function reliably for institutional investors.

Weaknesses

- The lending protocol Moonwell incurred $1.8 million in bad debt due to an “oracle misconfiguration” on the Base network, as reported by The Block. The incident occurred when the system received incorrect price data, allowing loans to be issued against improperly valued collateral, highlighting DeFi’s vulnerability to manual configuration errors.

- Peter Thiel, the billionaire co-founder of PayPal and Palantir, has completely exited his position in ETHZilla through his venture capital firm, Founders Fund. This high-profile exit coincides with analysis from K33 Research suggesting Bitcoin is approaching late bear market territory, signaling a lack of confidence in near-term recovery.

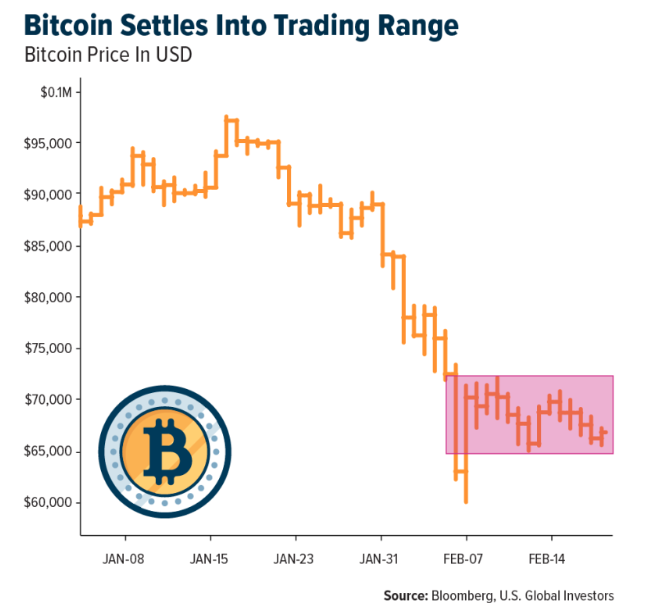

- Bitcoin remains trapped in a narrow trading range near $67,000, down 50% from its October all-time high of $127,000. This stagnation has prompted professional investors, including Sigil Fund, to de-risk and move toward cash, underscoring weak institutional conviction.

Opportunities

- The tokenization of equities is turning traditional stocks into “digital cash,” eliminating the 4 p.m. closing bell and multi-day settlement lag. With Kraken’s xStocks surpassing $10 billion in volume and Nasdaq filing to trade tokenized shares 24/7 on the same order book as traditional stocks, investors can now use shares as programmable collateral in real time, while the DTCC prepares for blockchain-based settlement in late 2026.

- The partnership between Anchorage Digital and non-U.S. banks to use the USAt stablecoin offers a way to bypass the legacy correspondent banking system. By enabling 24/7 settlement under a federally regulated framework, international payments can avoid the delays and high fees of SWIFT, bringing trillions in global liquidity onto compliant blockchain rails.

- A new report by Anchorage Digital shows 77% of stablecoin users would open a digital wallet with their traditional bank if available. This demonstrates a massive opportunity for banks to retain deposits, integrate blockchain custody, and capture liquidity currently flowing to crypto-native platforms.

Threats

- Google searches for “Bitcoin going to zero” have spiked to their highest levels in years, signaling extreme fear that threatens market stability. Such bearish sentiment can trigger panicked selling, forced liquidations, and delay price recovery, undermining investor confidence.

- According to Artemis Analytics, the supply of Tether (USDT), the world’s largest stablecoin, has shrunk by $1.5 billion this month, its largest decline since the FTX collapse in 2022. This sudden reduction in on-chain liquidity increases vulnerability to market crashes, as less “digital cash” is available to support crypto prices.

- Minneapolis Fed President Neel Kashkari dismissed the crypto industry as “utterly useless” and called stablecoins a “buzzword salad.” This highlights persistent skepticism at the Federal Reserve, raising the risk of stricter regulations that could hinder institutional adoption.

Defense and Cybersecurity

Strengths

- Airbus reported a record €17.7 billion in defense orders for 2025, driven by strong Eurofighter demand, and is merging its space activities with Thales and Leonardo to create a larger European space prime, while engine supply constraints from Pratt & Whitney are impacting the A320 family ramp-up.

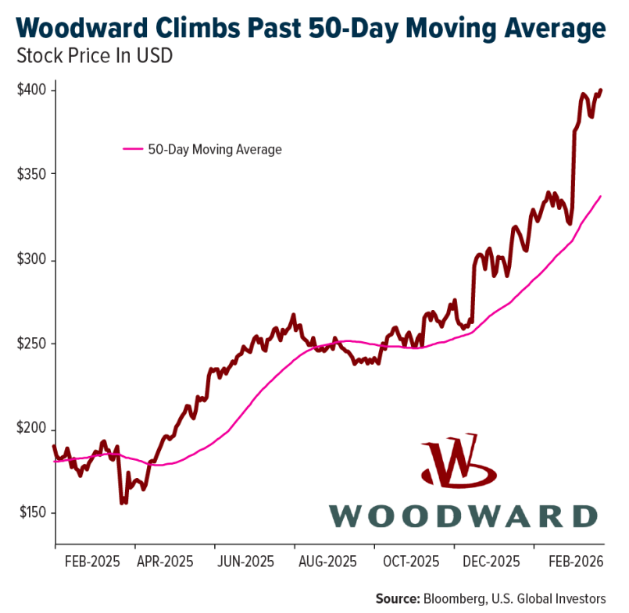

- Woodward’s recent performance reflects steady execution: quarter after quarter, aerospace demand remained firm, aftermarket activity expanded, and cash flow continued compounding, giving investors confidence that the business was operating smoothly. With management reinforcing momentum through disciplined capital returns and clear guidance, the stock has established itself as a durable aerospace compounder rather than a short term trade.

- Leonardo DRS secured significant contracts under the SHIELD Missile Defense Program with a potential ceiling of $151 billion, positioning the company for future task orders and enhancing its role in next-generation defense systems. The program involves providing advanced capabilities to military forces, reinforcing Leonardo DRS’s role in next‑generation defense systems.

Weaknesses

- Radware reported a significant 168% increase in global DDoS attacks in 2025, with Israel being the most targeted country, accounting for 12.2% of these attacks.

- Amazon Web Services experienced a major outage in Northern Virginia, disrupting streaming and e-commerce platforms worldwide and highlighting systemic dependence on a small number of cloud providers.

- Chinese hackers exploited a zero-day vulnerability in Dell data protection appliances, targeting systems used by numerous U.S. organizations. The vulnerability allowed prolonged unauthorized access for about 18 months, raising serious national security concerns, according to threat intelligence firms.

Opportunities

- Nvidia has expanded its AI footprint by launching a Hindi-first large language model for education in India and partnering on India’s first electric air taxi, while AMD’s $300 million loan guarantee to Crusoe for AI chips raises concerns about potential circular trading.

- Meta’s multi-year AI infrastructure partnership with Nvidia, involving a $325 billion investment in Nvidia’s Blackwell architecture and the adoption of the Spectrum-X Ethernet stack, represents a significant strategic move in AI infrastructure development.

- Micron plans to start production at its assembly, test, mark, and package (ATMP) facility in Sanand, Gujarat, by the end of February 2026. This will mark India’s first commercial-scale semiconductor production and will benefit from a ₹76,000 crore incentive package under the India Semiconductor Mission.

Threats

- Recent peace negotiations between Ukraine, Russia, and the United States have failed to produce a political breakthrough, reinforcing the risk of a prolonged conflict. While reports citing unnamed sources suggest internal expectations of a multi-year war, these claims have been officially denied by the Ukrainian government, highlighting high uncertainty, limited transparency, and continued geopolitical instability that could extend military activity and defense spending well beyond the near term.

- Escalating tensions between Iran, the United States, and Israel pose a growing geopolitical threat, as Iran has warned that any military action would prompt retaliation against U.S. and allied assets, while Israel has signaled readiness to act against perceived strategic risks. With diplomacy stalled and military posturing increasing, the risk of a wider regional conflict remains elevated, adding uncertainty to global security and energy markets.

- AI and data center growth is increasingly constrained by physical limits, including shortages in advanced semiconductors, packaging, high-bandwidth memory, and power infrastructure. As supply chain lead times remain extended, these bottlenecks raise execution risk and cost pressure, threatening the pace and efficiency of AI-driven expansion.

Gold Market

Gold futures closed the week at $5,117.80, up $71.50 per ounce, or 1.42%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.23%. The S&P/TSX Venture Index came in up 4.98%. The U.S. Trade-Weighted Dollar rose 0.85%.

Strengths

- The best performing precious metal for the week was silver, up 8%. Silver continues to demonstrate its role as gold’s high-torque sidecar – climbing alongside bullion to as high as ~$79/oz as Middle East tensions and Federal Reserve uncertainty drive haven demand. With both monetary and industrial demand underpinning its rally, silver historically outpaces gold during sustained bull markets, offering investors amplified upside as the precious metals cycle matures, Bloomberg writes.

- Pan African Resources delivered exceptional H1 FY26 results with revenue surging 157.3% to $487.1 million, record profit of $147.8 million and a 50.3% EBITDA margin, driven by strong production gains across its portfolio and record gold prices which lifted its share price 14% this week. Pan African highlights the strength that comes from exposure to high-margin, growth-oriented gold producers, with the company guiding 275,000–292,000 oz for FY26 and pursuing multiple organic expansion projects to drive further production growth.

- Centerra Gold (CGAU) delivered a standout Q4 2025 beat, with adjusted EPS of $0.41 surpassing the $0.33 consensus estimate. Earnings more than doubled year over year from $0.17 in Q4 2024 and increased from $0.33 in Q3 2025, as elevated gold prices flowed directly to the bottom line. Centerra also exercised its pro rata participation rights in Thesis Gold’s C$44 million AngloGold Ashanti-led financing, subscribing for approximately C$5.7 million at C$2.79 to maintain its 9.9% ownership. The underlying project carries a PFS-level 54.4% after-tax IRR and a C$2.37 billion NPV at US$2,900 per ounce gold, ahead of a 2026 feasibility study. When a major such as AngloGold validates an asset with fresh capital and an existing strategic investor immediately maintains its stake, Centerra is building more than a mine operator. It is assembling an embedded optionality pipeline with leveraged upside to exploration success.

Weaknesses

- The worst performing precious metal for the week was gold, still up 1.4%. Gold remained a pillar of strength, pushing above $5,000 an ounce for a third consecutive day of gains as Middle East tensions and an uncertain Federal Reserve outlook sustained haven demand — yet among the precious metals complex, bullion posted the most modest advance.

- Royal Gold reported Q4 earnings, resulting in a decline in its share price this week while its peers posted further gains. The company guided Q1 2026 GEO sales flat with Q4 and indicated it would be the lowest quarter of the year, creating a near-term headwind for a stock priced for growth. Revenue per share rose both year over year and quarter over quarter. However, the primary concern is capital commitment risk. Royal Gold still needs to fund $100 million for its Warintza stream in two tranches over the coming months, continues to incur costs on the Hod Maden joint venture it is attempting to restructure, and faces a potential $225 million outlay to convert its MARA royalty into a stream, all while carrying debt that will not be fully repaid until early 2027.

- Newmont, the world’s largest gold miner, warned that 2026 production is expected to decline roughly 10% due to planned mine upgrades — a supply-side signal that operational headwinds and rising costs across the industry remain a structural drag on margins, even as gold prices press above $5,000

Opportunities

- Wheaton Precious Metals Corp’s $4.3 billion acquisition of BHP Group’s additional 33.75% silver stream at Antamina Mine doubles its silver exposure, adding roughly 6–7.5 million attributable ounces annually and supporting GEO growth to 1.2 Moz by 2030. At current silver prices, the incremental production adds approximately $225–240 million in annual revenue, underpinning management’s $3.2 billion operating cash flow forecast for 2026. Investors should monitor the $2.4 billion net debt load taken on to fund the deal. Management is showing a vote in confidence that the current silver prices are sustainable.

- Turkey’s Treasury sold 2027 gold-denominated bonds and gold-based sukuk backed by more than 30 metric tons of gold, reinforcing gold’s deepening role as a sovereign monetary anchor and reflecting sustained institutional appetite for hard-asset-linked debt as a hedge against currency volatility.

- The Supreme Court’s 6-3 IEEPA tariff ruling today—striking down Trump’s reciprocal and fentanyl-related tariffs—creates a compounding fiscal tailwind for gold: the Treasury faces a potential $175 billion refund liability that must be financed through additional debt issuance, layered on top of a structural trade deficit that already floods foreign reserve holders with dollars and drives them toward gold diversification. The Tax Foundation estimates U.S. households absorbed roughly $1,000 in tariff costs in 2025, with the ruling potentially cutting that burden nearly in half—but the fiscal hole left behind only deepens the sovereign borrowing trajectory. More debt, a weaker dollar, and rising questions about U.S. fiscal credibility reinforce the structural bull case for bullion.

Threats

- Sudan’s Ministry of Minerals signed a cooperation agreement with a subsidiary of the Saudi Gold Refinery Company focused on gold exploration, broader mineral development, and upgrading mining infrastructure. While the pact aims to increase production and strengthen Sudan’s mining capacity, it deepens Saudi access to primary gold supply through a country with significant geopolitical and operational risk—flagging the growing pattern of Gulf sovereign capital moving to secure upstream precious metals exposure in frontier jurisdictions, which could introduce new competitive dynamics into African gold supply chains and raise questions about Western investment access to the same assets.

- From a fundamental standpoint, Bank of America sees total gold production in 2026 lower by 2% to 19.2 million ounces for the 13 North American precious metals stocks in their coverage, with consensus approximately 2% too high for 2026 production estimates. Average all-in sustaining costs (AISC) are seen rising 3% to $1,600/oz in 2026, and cost drift remains a feature of the current gold market as producers increasingly chase incremental, lower-margin material. With margins remaining strong given elevated gold prices, the sector appears focused on growth with cost control a lower priority—a dynamic that could blunt free cash flow generation if spot prices correct materially from current levels, according to UBS.

- Persistent Federal Reserve hawkishness poses a headwind for gold, as Governor Stephen Miran dialed back calls for deep rate cuts amid stronger-than-expected economic data — with higher-for-longer rates elevating the opportunity cost of holding non-yielding bullion and risking a reversal of the haven bid should geopolitical tension de-escalate faster than markets anticipate.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2025):

Boeing

JetBlue

Airbus SE

Delta Air Lines

United Airlines

American Airlines

Southwest Airlines

Deutsche Post

Embraer

Vikings Holdings

Moncler

Tesla

Toll Brothers

Hilton Worldwide

LVMH

Kering

Airbus

Leonardo DRS

Lundin Mining

BHP

Hudbay Minerals

Pan African Resources PLC

Centerra Gold Inc.

Royal Gold Inc.

Newmont Corp.

Wheaton Precious Metals Corp.

BHP Group Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Argus Jet Fuel Index is a comprehensive, daily benchmark for global jet fuel pricing, providing spot prices and market insights for airlines, suppliers and traders.

The NYSE Arca Airline Index (XAL) is a modified equal-dollar weighted index tracking the performance of highly capitalized U.S. and international airline companies.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits