What you need to know

The agenda is being reset for US shareholder meetings in 2026. Regulatory shifts have led to a steep decline in overall shareholder proposals while governance issues are becoming the biggest battleground. As companies gain new power to block shareholder proposals, investors may turn to other routes to make their voices heard. Research-driven independence and a focus on governance fundamentals can guide investors through a changing environment.

Change is in the air as the 2026 US proxy voting season begins. Regulatory shifts and new voting dynamics will challenge investment firms to remain principled in their approach to stewardship.

The proxy pendulum is swinging. After several years in which environmental and social issues gained prominence, governance matters such as director elections and executive compensation have reentered the spotlight.

This year, ballots will be cast amid significant regulatory and legal moves. Proxy advisory firms are under intense scrutiny while state and federal laws and enforcement actions have added layers of complexity to governance decision making. We believe investment firms should enter proxy season with eyes wide open: aware of what’s changing yet guided by a materiality-based framework to vote independently with conviction.

Regulatory and Legal Landscape Is Evolving

From 2020 to 2024, the number of shareholder proposals increased steadily, fueled by growing interest in the ‘E’ and ‘S’ issues of the environment, social and governance (ESG) mix. This year’s proxy season begins after a whirlwind 2025, driven by a series of moves impacting shareholder proposals.

Perhaps the most significant regulatory move will empower companies to have more control of the agenda. During 2025, the US Securities and Exchange Commission (SEC) issued new guidance and decisions that alter the dynamics of the proxy voting process. First, the SEC said it would allow issuers to more easily exclude shareholder proposals—including those in the “ordinary business” bucket. In other words, if a company says a certain shareholder proposal is really a matter of day-to-day business, it will have much more latitude to exclude it from the agenda.

Toward year end, the SEC expanded that guidance, and now it may decline to express a view on certain no-action requests. As a result, it has effectively left it to companies to determine whether to exclude a proposal.

Shareholder proponents may be further constrained by another recent regulatory shift. In January, the SEC narrowed the use of exempt solicitation filings, saying it will no longer accept voluntary filings from shareholders with less than $5 million ownership. This will make it harder for smaller proponents to post supporting materials on EDGAR, limiting a channel often used to amplify arguments behind shareholder proposals or to organize vote‑no campaigns. We expect this change to reduce the volume of publicly filed support materials in proxy season and to dampen vote‑no campaign activity. Proponents may increasingly turn to press outreach and direct engagement with investors, raising cost and coordination hurdles required to be heard.

Companies may also benefit from technical adjustments designed to boost retail voting participation. For example, the SEC allowed ExxonMobil to implement a voluntary program enabling retail investors to opt into automatic proxy voting aligned with management recommendations, which has the potential to bolster management support.

Advisory Firms Under Pressure

Meanwhile, enhanced scrutiny on proxy advisory firms is in full swing. Regulators and lawmakers are investigating firms like Institutional Shareholder Services (ISS) and Glass Lewis over potential conflicts of interest, particularly regarding ESG issues. Attorneys general in Florida, Mississippi and Missouri have led the charge, while Texas has introduced new disclosure requirements for advisory firms and is stepping up oversight and enforcement. President Trump, too, issued an executive order to federal agencies, including the SEC and the Federal Trade Commission, to reevaluate regulatory treatment of proxy advisory firms and market practices.

In response, some large firms have stopped using third-party advisors for US proxy research, opting for alternatives including AI-based solutions. Proxy advisory firms are adapting by offering more customized research options, while new entrants are challenging the dominance of established players.

Shareholder Proposals Go Back to Governance Basics

These dynamics have already prompted shifts in voting trends, which are likely to continue in 2026.

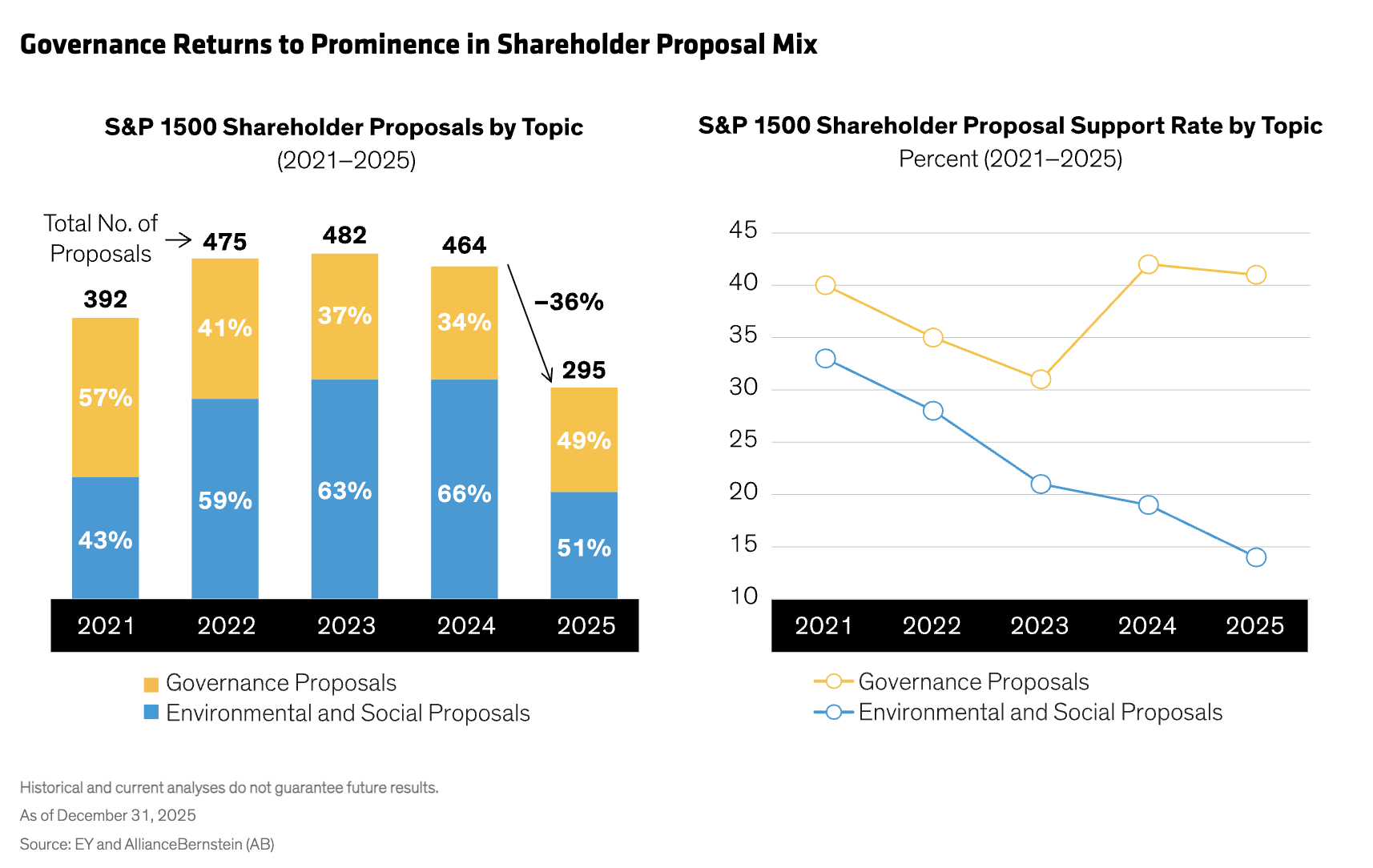

Fewer shareholder proposals reached ballots in 2025, and average support levels declined across major categories. The number of proposals dropped by 36% to 295 across topics, with governance accounting for nearly half of all issues (Display). Governance proposals received 41% support on average—eclipsing support for environmental and social proposals.

It’s true that support for environmental and social proposals has been declining for several years. Now, lower expectations for these initiatives to succeed—along with lower barriers for management to exclude proposals—may discourage proponents from raising them in the first place. In cases where companies face significant environmental and social controversies, we expect shareholders to start exploring other avenues to affect change, for example, through director election votes.

Governance Fundamentals in Focus

Corporate governance doesn’t typically grab headlines. Yet these issues—from board composition and independence to responsiveness to shareholders—are at the heart of how businesses run and can have a material impact on companies’ financial performance.

Director elections, for example, are a powerful tool for investors to weigh in on ineffective boards. In our experience, shares of US companies with boards that we’ve supported have outperformed firms that didn’t meet our governance expectations.

On the governance menu, executive compensation will remain a hot topic. Median total compensation for S&P 500 CEOs reached $17 million in 2024, representing a 5% increase over the prior year, according to Pay Governance. This growth was primarily driven by larger long-term equity grants, which were buoyed by strong equity performance during the period.

The tech titans have been in the compensation spotlight since Tesla awarded unprecedented pay packages to Elon Musk in 2018 and 2025; both were large long-term equity grants with ambitious performance hurdles. We anticipate an increase in these types of CEO packages, which may appear on proxy ballots more frequently in the future.

Beyond the high-profile compensation stories, we expect an increased focused on core governance issues such as board accountability and risk oversight. For example, “common sense” governance proposals are rising, including simple majority vote requirements, the right to call special meetings and board declassification. Proposals like these passed most often in 2025, signaling continued investor support for improved shareholder accountability despite elevated scrutiny of ESG practices.

AB’s Proxy Voting Principles: Materiality and Independence

While the industry grapples with multiple transitions, we believe that our longstanding proxy voting framework continues to provide a strategic path forward. Our approach focuses on issues that are material to business and investors, backed by a willingness to vote independently.

Maximizing shareholder value is the primary goal of our votes. That’s why our positions are rooted in thorough research and engagement, designed to fully understand the material impact of any proposal on a company’s business—and our clients.*

Translating those positions into effective votes demands independence.

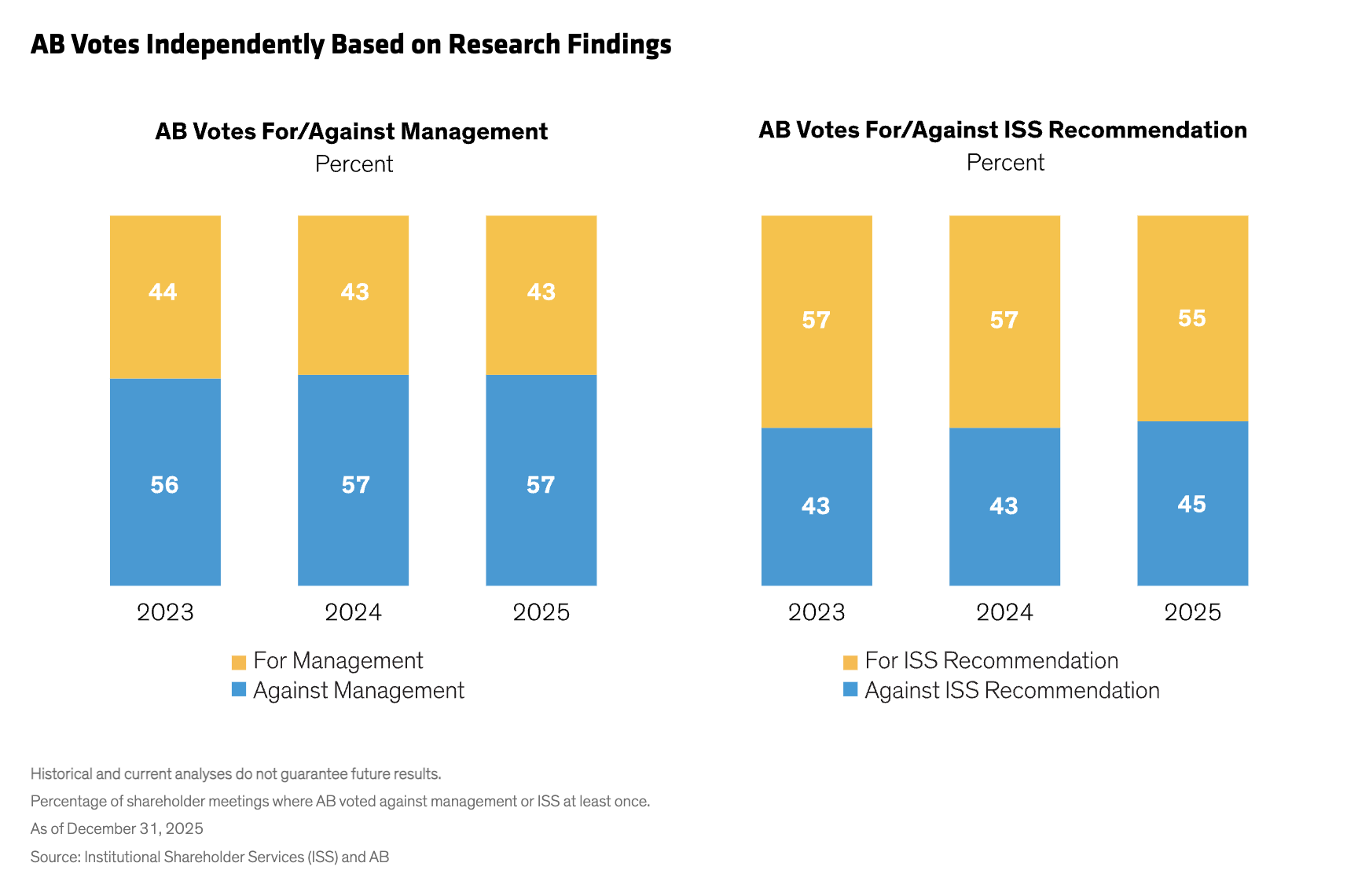

In 2025, we voted against management at least once in 57% of shareholder meetings in which we participated (Display). We also voted contrary to ISS recommendations in 45% of meetings.

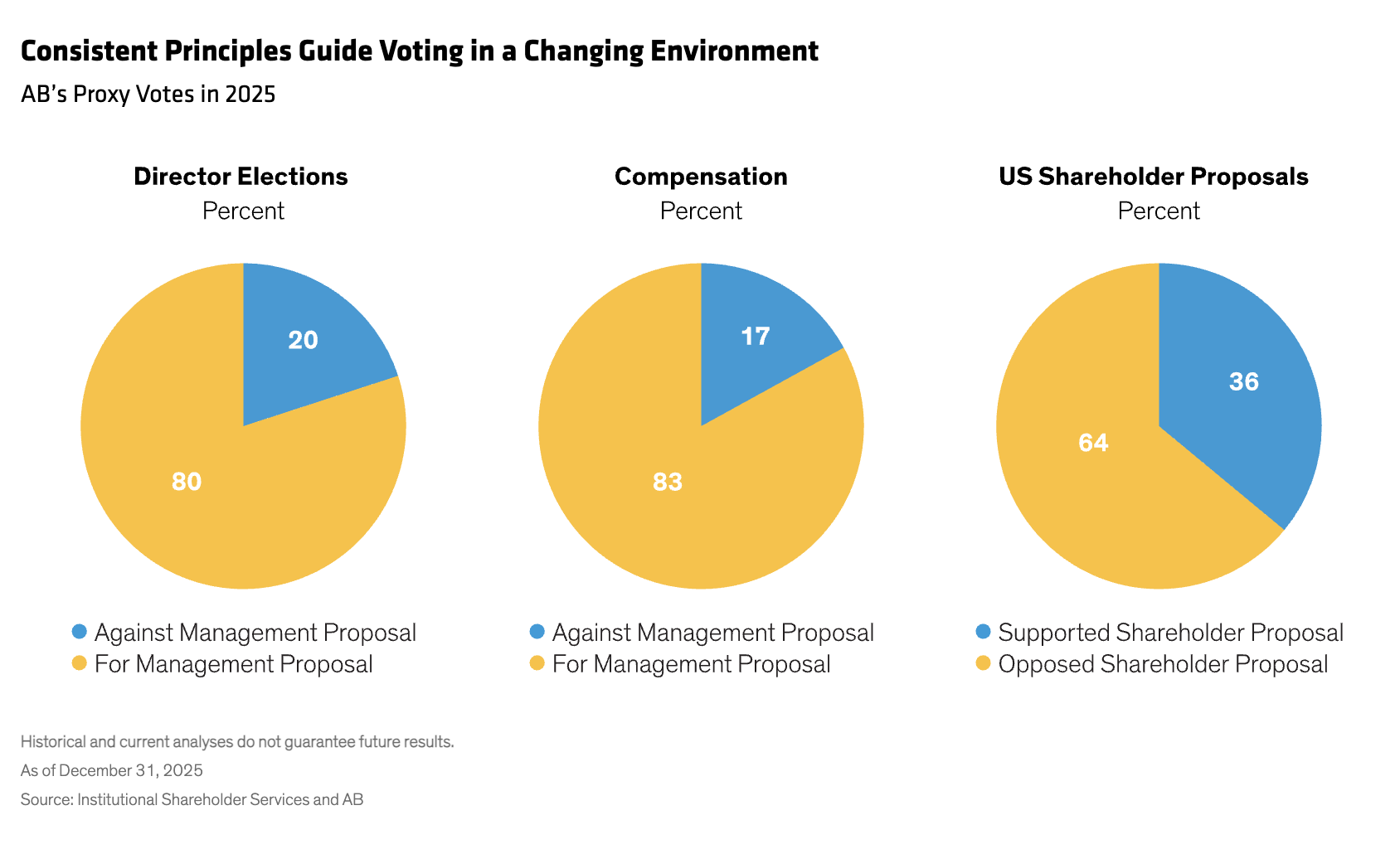

We stood against management proposals on director elections and compensation 20% and 17% of the time, respectively (Display). And we voted in support of approximately 36% of all shareholder proposals.

AB’s investment stewardship approach is rooted in a partnership with our sector analysts and portfolio managers, which enables us to take industry—and company specific considerations into account to make more informed voting decisions. For example, in the healthcare sector, we’ve found that sound compensation practices can make a meaningful difference to long-term investor outcomes.

Shaping the Norms of Responsible Stewardship

As the 2026 proxy season unfolds, investment firms have a responsibility to lead with clarity and a disciplined focus on what drives long‑term value. While the regulatory environment may generate headlines and can be confusing for investors, we think the renewed focus on governance will provide shareholders with ample opportunities to weigh in on an array of issues that can materially affect business success and shareholder outcomes.

Entering the season with well‑defined principles, rigorous research and a readiness to vote independently of management or proxy advisors will be essential—especially as governance issues become the primary arena for impact.

Landon Shea, Investment Stewardship Associate and Research Lead, and Cole Moore, Investment Stewardship Analyst and Engagement Lead, were instrumental in the research supporting this blog.

*AllianceBernstein (AB) engages issuers where it believes the engagement is in the best financial interest of its clients.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

Bob Herr is a Senior Vice President and Director of Corporate Governance within the Responsible Investing team.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein