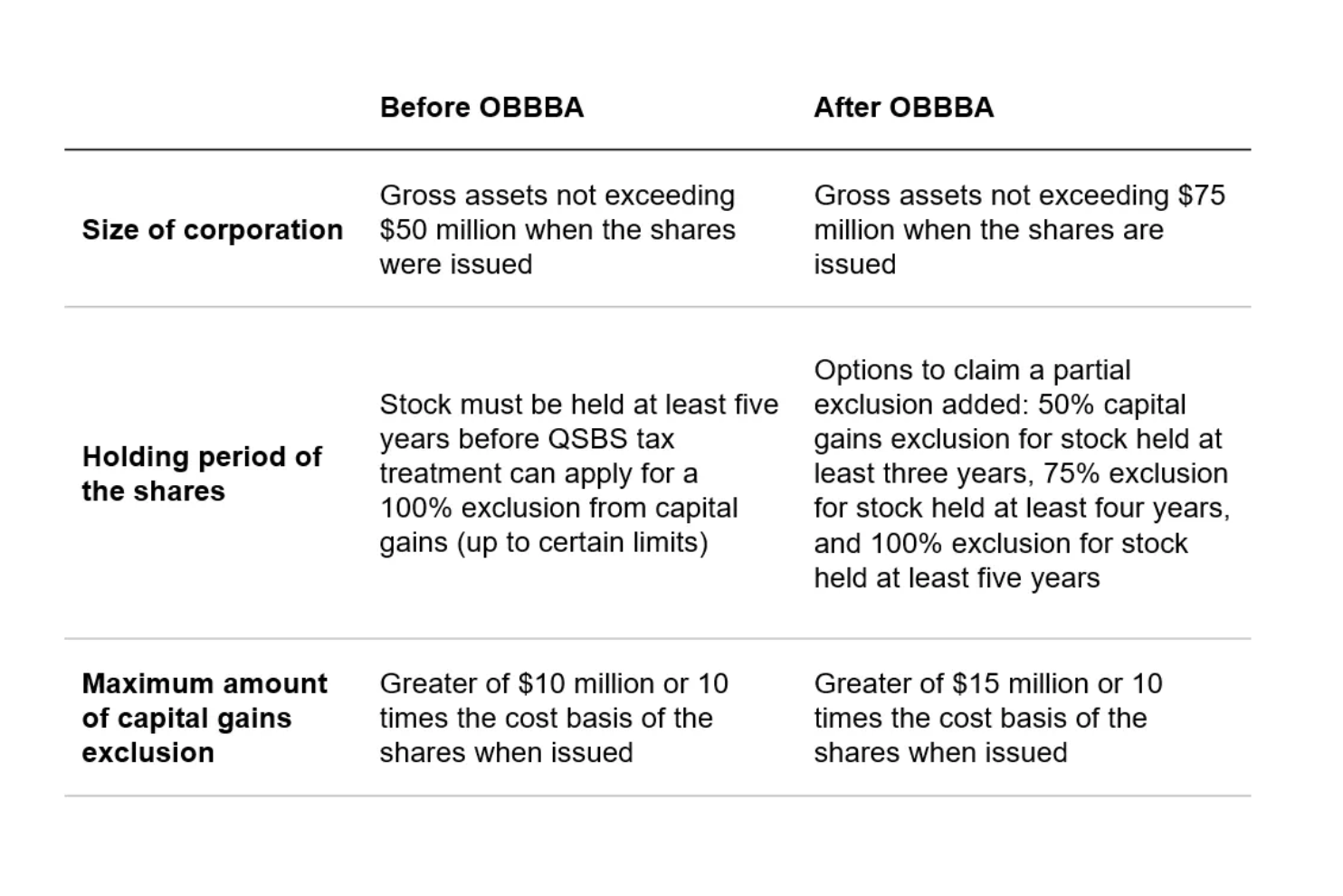

A little-known provision in the tax code, Qualified Small Business Stock (Section 1202), allows certain business owners to avoid capital gains on the sale of closely held business shares. What was a significant tax benefit historically is further enhanced after the passage of the One Big Beautiful Bill Act (OBBBA) in 2025. If specific requirements are met, an owner of business shares may be able to exclude up to $15 million (or more in certain cases) of appreciation in the stock from federal capital gains taxes.

This provision is considered one of the most complex areas of the tax code requiring in-depth analysis from a qualified tax professional.

What is Qualified Small Business Stock (QSBS)?

When stock shares meeting the definition as QSBS are sold, up to $15 million of capital gains or 10 times the original cost basis of the stock—whichever is greater—can be excluded from capital gains treatment. To benefit from this massive tax break, the shares being sold must meet specific qualifications. First, this tax treatment only applies to a business organized as a domestic C-corporation (or an LLC that elects to be taxed as a corporation). Companies structured as pass-through entities for purposes of taxation are not eligible. These would include sole proprietors, partnerships, most LLCs and S-corporations.

Here are some additional requirements to meet the definition of QSBS:

- The company must meet an aggregate gross assets test to determine if shares may be considered QSBS. Currently, if gross assets exceed $75 million at the time the shares are issued, QSBS treatment is not available.

- The stock must generally be acquired directly from the company through an initial issuance, which means that shares purchased from another corporate shareholder are not eligible for this special tax treatment. However, QSBS acquired from an original issue and subsequently gifted to another person may be eligible for the capital gains exclusion.

- The corporation must use at least 80% of its assets in a “qualified trade or business” which generally excludes professional service-related firms (law, accounting, finance, banking, etc.). Other types of businesses operating in the areas of hospitality, natural resources and farming are excluded as well. Additionally, the company must not hold more than 10% of its assets in securities.

How the OBBBA expands the tax benefits of QSBS

The OBBBA expands QSBS tax treatment for shares issued after the signing of the law on July 4, 2025.

Planning considerations for business owners

- When establishing a smaller business that may have significant growth potential and meet the requirements of being considered a qualified small business under Section 1202, weigh the benefits of structuring the entity as a C-corporation instead of a pass-through entity like an LLC or S-corporation. This may allow for capital gains exclusion in the future when the shares are disposed. A decision like this must be made in consultation with the appropriate tax and legal experts, performing a thorough analysis of the type of business entity making the most sense based on particular circumstances.

- S-corporation business owners may consider converting the firm to a C-corporation to “start the clock” on reaching the holding period necessary to benefit from QSBS tax treatment when shares are sold. This can be a complicated process requiring thorough analysis and consultation with qualified professionals.

-

Gift shares of QSBS to other family members. When QSBS is gifted, the holding period for the shares generally carries over to the recipient for purposes of meeting the five-year requirement for capital gains exclusion (or the three- or four-year period to benefit from partial exclusion). Additionally, the tax benefit of QSBS in some cases may be “stacked” when shares are gifted to other beneficiaries, since each recipient may benefit from the maximum capital gains exclusion based on their gifted shares (up to $15 million or ten times the cost basis, whichever is greater).

Seek professional guidance

As noted, this is one of the most complex areas of the federal tax code. In addition to the requirements highlighted, there are more nuanced areas of Section 1202 that may need to be addressed. Consulting with a tax and legal professional with working knowledge and expertise around this area of the tax code is needed. Lastly, since some states may not recognize this special tax treatment, there may be state income tax ramifications when QSBS is sold.

Source: Internal Revenue Code Section 1202

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Franklin Templeton

Read more commentaries by Franklin Templeton