Key Takeaways

- Market leadership broadened in 2025, and this has continued in 2026, with emerging markets (EMs) and some developed markets outperforming the United States.

- Asset-heavy sectors dominate, reflecting that AI infrastructure and national-security spending are driving a multiyear global capex cycle in data centers, power, defense, and supply chains.

- Investor outcomes hinge on AI capex returns, who captures software profits, and which firms qualify as domestic suppliers in a more localized world.

After a decade defined by narrow, largely intangible businesses driving growth, markets appear to be entering a new phase shaped by physical buildout across AI infrastructure, defense, energy, and supply chains. As discussed in our prior piece, “The Revenge of the Tangibles,” this shift reflects a broader global building cycle that is driving growth and returns beyond the United States and across a wider range of industries and regions. Here, we move from the high-level thesis to examine how that shift is showing up in markets today—and the questions it raises for investors.

A Broader Market Awakening

When discussing the future of the markets, it is always useful to begin with what markets have already told us.

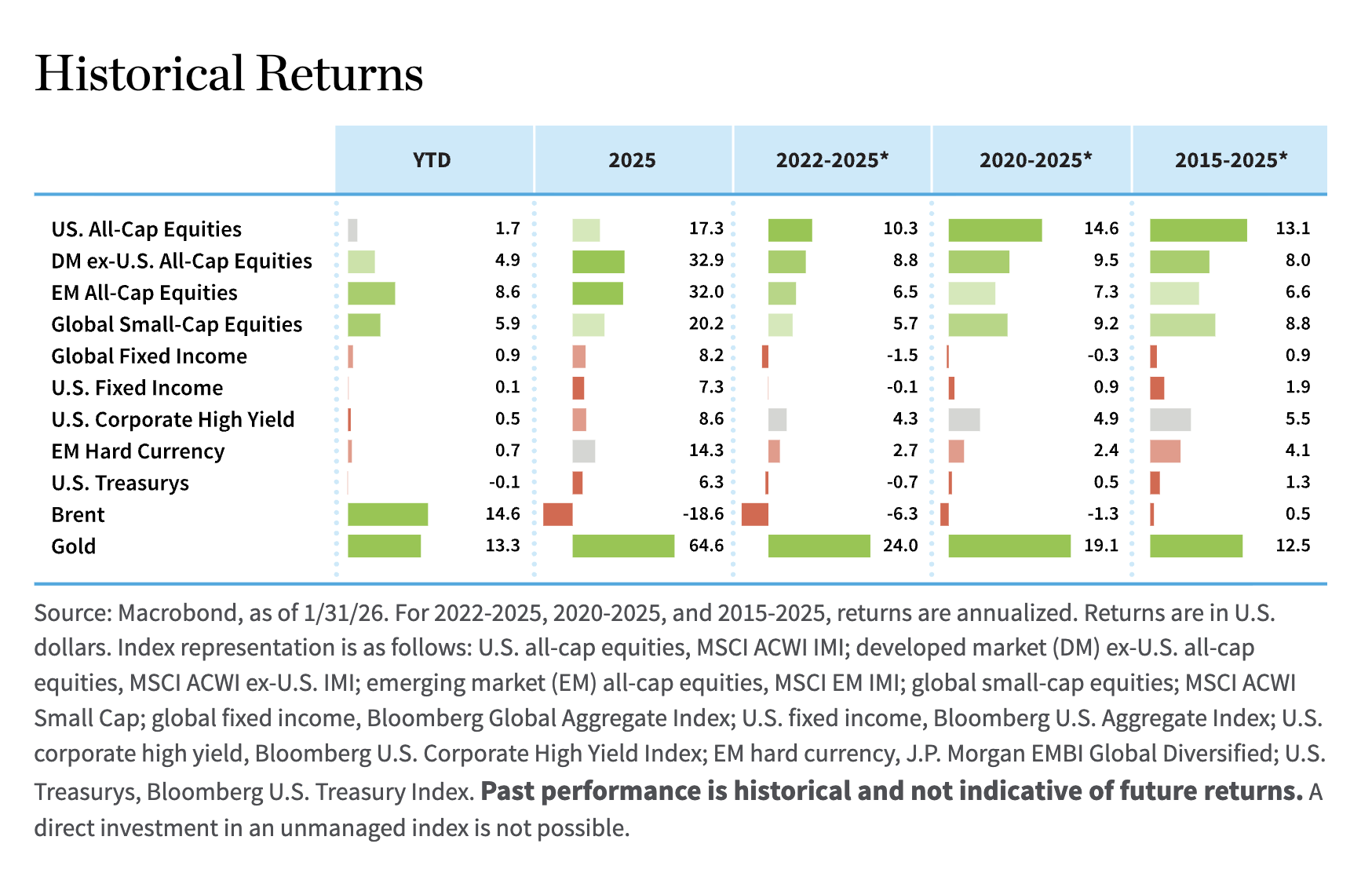

Over the past decade, returns across major asset classes created a clear narrative. A long-term investor who allocated to equities and looked away may have concluded that the United States was the only place to generate meaningful returns. U.S. equities delivered annualized gains two to four times higher than most alternatives. That is a substantial gap over a long period and it shaped asset-allocation decisions around the world.

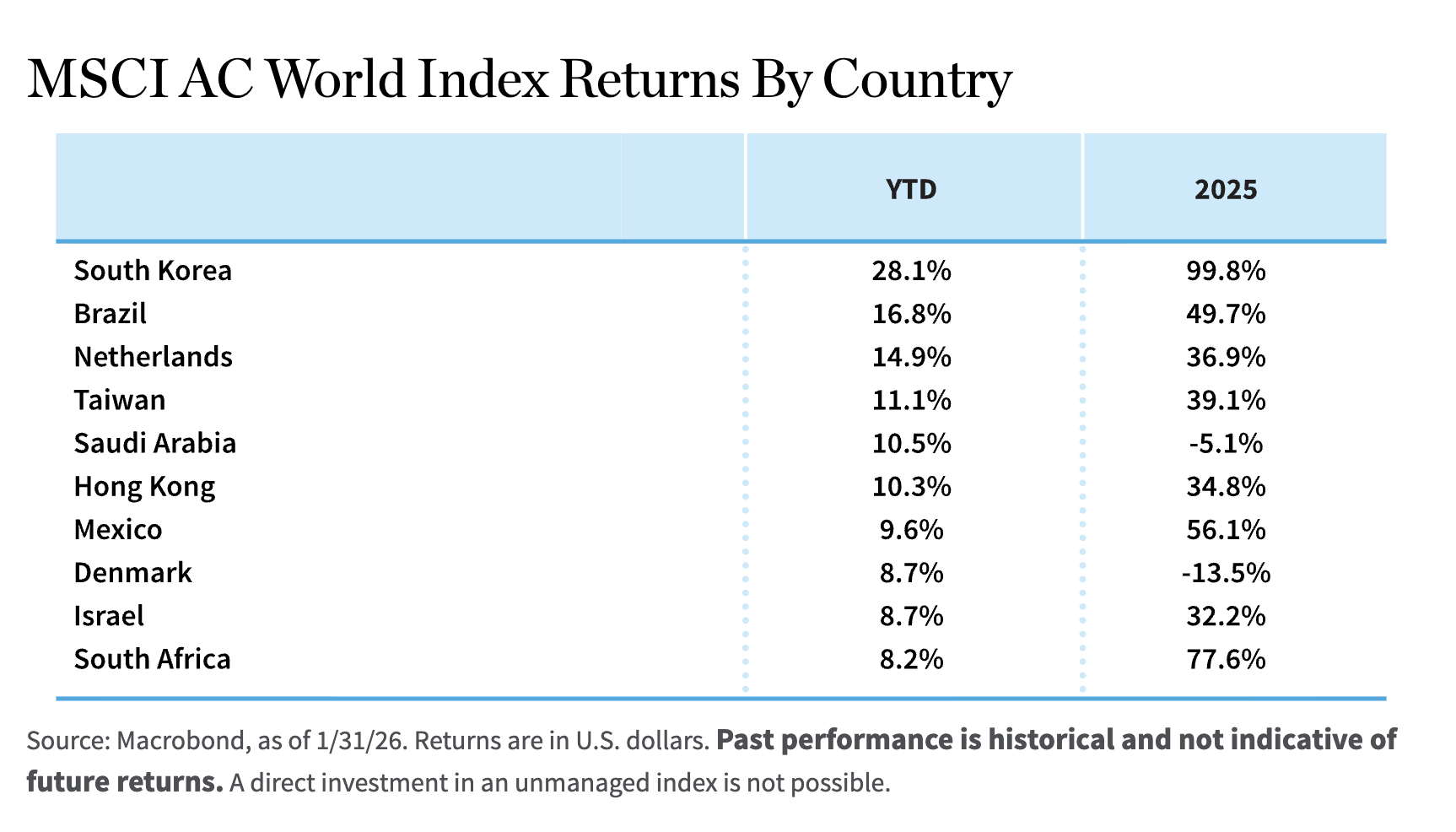

Over the past three years, however, that picture has begun to change, with jurisdictions that had been dormant showing signs of life. In 2025, U.S. equities, while still vibrant, lagged both EMs and some developed markets. Early 2026 data show the same pattern. While still attractive, the United States is no longer the only engine of global equity performance.

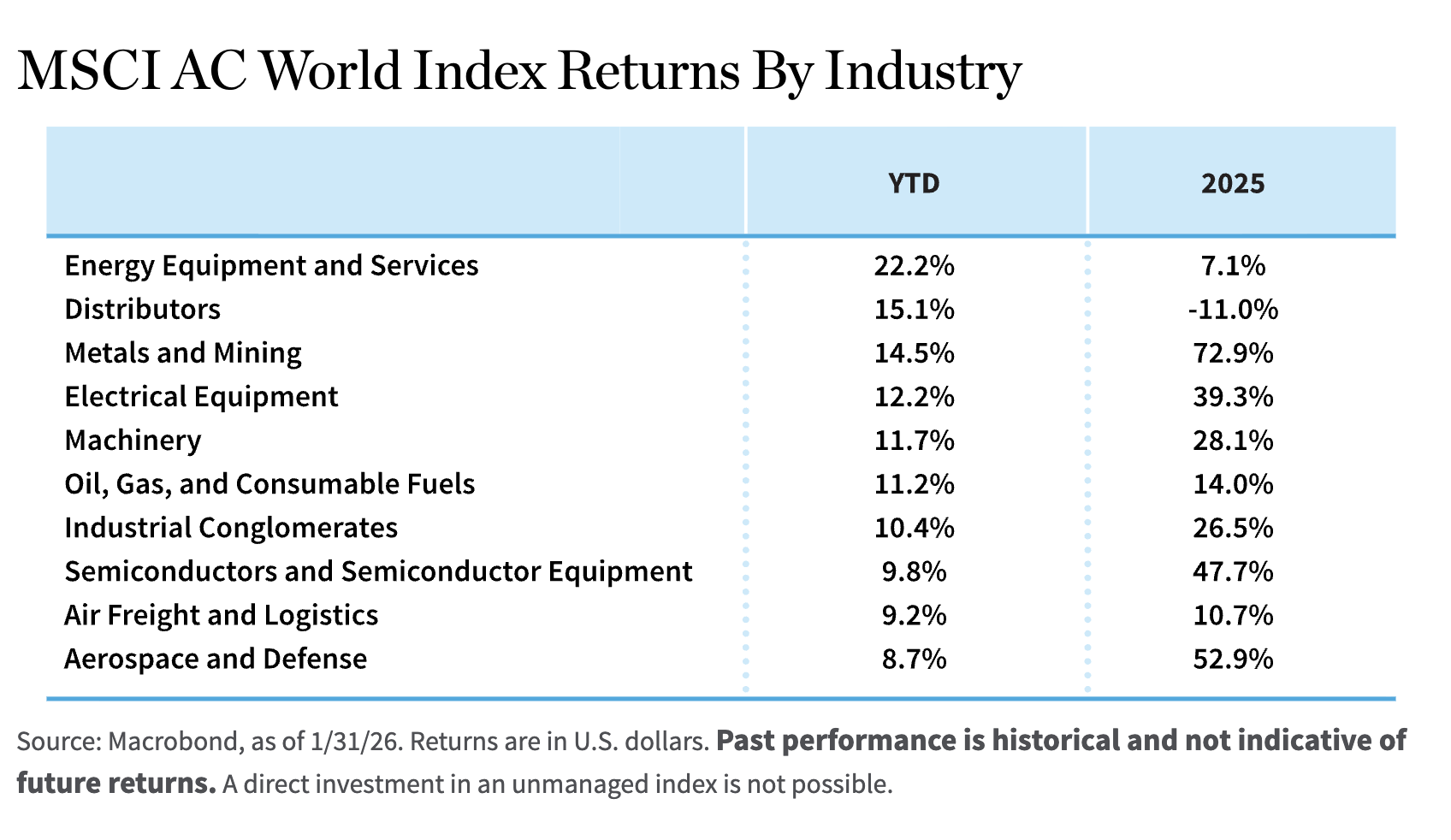

What’s changing? One change is the industry composition of returns. Leading sectors—including semiconductors, hardware, machinery, mining and metals, and industrial conglomerates—are asset-heavy industries. Many underperformed for years and were largely overlooked. Country-level performance shows a similar pattern. Jurisdictions with strong exposure to building and industrial capacity are rising in the rankings. It appears we are in the early innings of a structural shift.

Two Forces Driving Change

What is happening, and how long could it persist? Two forces appear to be acting together to drive this change: technological transformation and geopolitics.

On the technology side, AI has moved from concept to programming to infrastructure buildout. Across the world (though primarily in the United States and China), we are seeing a tremendous buildout of the AI infrastructure. Massive data centers are being built across geographies, and we’ll need to build even more of them as technology becomes a larger portion of everyday life. These facilities will require semiconductors, cooling systems, power infrastructure, and connectivity. They also require roads, airports, transmission lines, and energy supply. This is not confined to one country or region; the scale is global. And the buildout has a long runway; it is measured in years and even decades, not quarters.

The second force is geopolitical. Many countries are now pursuing greater economic autonomy. This is really a response to America First policies, which did not start with the current administration. The shift began a decade ago; the current administration has simply made it more explicit and taken more concrete steps to implement it.

In geostrategic parlance, the shift is toward every country for itself. It’s about abandoning the post-World War II global integrationist order and ensuring the ability to go it alone. In practice, that means every country that is now capable is trying to figure out how to bulletproof their national economies. Policymakers are prioritizing national resilience in defense, energy, and supply chains.

Economic autonomy is really about physical growth, so the practical result is increased public and private investment in physical infrastructure and industrial capacity. As governments negotiate trade agreements, fund defense and energy projects, and lower barriers within regional blocs, we’re seeing growth in more places. Canada, Australia, Japan, and much of Europe are moving in this direction at varying speeds.

This technological investment and geopolitical reprioritization are reinforcing each other. Building AI capability and building national autonomy now require many of the same inputs. Modern defense is less about legacy hardware and more about drones, remotely operated systems, and software-enabled platforms. Supporting those systems requires the underlying industrial stack: critical minerals, electric and magnetic motors, and the full range of components that power electrified and autonomous technologies.

Those same inputs extend beyond defense. The infrastructure needed for autonomous logistics, robotics, and advanced manufacturing—such as drones delivering customers’ Amazon and Walmart packages—relies on the same electric and digital backbone. We need factories and robots, but also software that connects it all, and a lot more copper, silver, and rare earths. The prominence of metals and mining in recent performance reflects that linkage.

When mapped onto a traditional industries-and-countries framework, the resulting investment opportunities appear widely dispersed across regions. Defense-related spending is becoming more compelling in places such as Germany and Japan. Technology hardware and semiconductors remain concentrated in established hubs such as Taiwan and South Korea, with Japan also participating. Metals and mining continue to be anchored in many emerging markets, including Mexico, South Africa, and Chile, particularly in copper.

Lastly, as growth strengthens and investment accelerates, yield curves typically steepen, creating a more favorable environment for financial institutions. Banks, as the conduit for capital flows, tend to participate broadly in such cycles, and this environment is unlikely to be an exception.

Three Questions for Investors

Markets are now grappling with several key questions.

The first is the economics of AI infrastructure. Hyperscale technology companies are investing heavily in data centers and related capacity. Will future revenues and profits justify this investment? Or will business models evolve in ways that reduce cash generation? These companies have been central to market performance for years, and the answer will matter for valuations and capital allocation.

The second is the future of software. Demand for software will undoubtedly rise as AI capabilities expand. The question is who will deliver it. Will incumbent providers adapt their existing platforms, or will new entrants capture a meaningful share of the opportunity? Hyperscalers may choose to move further up the stack, embedding applications and workflows into their ecosystems. The allocation of these profit pools remains highly uncertain.

The third is the definition of a “national builder.” As countries pursue economic autonomy, which companies will be allowed to participate in key projects? Will domestic firms be favored, or will suppliers from allied jurisdictions benefit? Legal, financial, and geopolitical considerations will shape access to markets and profits. These decisions will influence which companies capture value from the current investment cycle.

An Environment Shaped by Building

The common thread across these developments is construction—of infrastructure, supply chains, and industrial capacity. Markets are reflecting that shift. Performance leadership is broadening beyond the narrow set of winners that defined the previous decade. The combination of technological investment and geopolitical priorities suggests that this phase may persist. For investors, periods of dislocation often create opportunity. The current environment appears to be one of those periods.

Olga Bitel, partner, is a global strategist on William Blair’s global equity team.

The Bloomberg Global Aggregate Index is a broad, market-capitalization-weighted benchmark of global investment-grade fixed-income markets, including government, corporate, and securitized bonds across developed and emerging markets. The Bloomberg U.S. Aggregate Index is a A flagship benchmark for the U.S. investment-grade bond market, covering Treasuries, government-related, corporate, mortgage-backed, and asset-backed securities. The Bloomberg U.S. Corporate High Yield Index is a market-value-weighted index that tracks the performance of U.S.-dollar-denominated, below-investment-grade corporate bonds issued in the United States. The Bloomberg U.S. Treasury Index: A benchmark tracking the performance of United States Treasury securities across maturities, including bills, notes, and bonds, in the domestic fixed-income market. The J.P. Morgan EMBI Global Diversified measures total returns for U.S.-dollar-denominated sovereign and quasi-sovereign emerging-market bonds, with country weights capped and redistributed to reduce concentration. The MSCI ACWI ex-U.S. IMI is a global equity index that tracks large-, mid-, and small-cap stocks across developed and emerging markets outside the United States. The MSCI ACWI IMI is a global equity index that tracks large-, mid-, and small-cap stocks across developed and emerging markets, representing the broad opportunity set of publicly listed equities worldwide. The MSCI ACWI Small Cap is a global equity index that tracks small-cap stocks across developed and emerging markets. The MSCI EM IMI is an equity index that measures the performance of large-, mid-, and small-cap stocks across EMs. The MSCI AC World Index is a market-capitalization-weighted index that tracks large- and mid-cap equities across developed and emerging markets globally.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by William Blair