Proposals to engineer secondary trading in private assets, often championed by vocal critics of public market liquidity, have gained renewed momentum. For some, enhanced tradability is viewed as a remedy to growing unease over the absence of transparent, real‑time valuation signals in private portfolios. For others, secondary trading is presented as a way to mitigate “jump risk” in direct lending credit portfolios, where loans are commonly carried at par until fundamentals deteriorate and repricing becomes unavoidable.

This debate is unfolding against a notable backdrop. Public credit market liquidity today is as strong as at any point since the global financial crisis, while spreads between less liquid direct lending and more liquid public credit have compressed materially in recent years.

For investors, this raises a fundamental question: Am I being adequately compensated for the illiquidity I am assuming in private markets? In our view, the answer is often no, particularly in corporate credit. The promise of greater secondary liquidity in private assets is, in some cases, being used to justify a meaningful erosion of the illiquidity premium in direct lending relative to public markets, rather than to genuinely improve investor outcomes.

More structurally, we see several key obstacles to creating meaningful liquidity in private credit:

-

Permissioned transfer of loans: Unlike public markets, many private credit documents require borrowers to consent to any sale or transfer of their loan from the lender(s) of record.

-

Information asymmetry: In private credit, buyers often lack access to credit agreements, amendment details, collateral packages, or standardized financial documents. This information has been paramount to building confidence and liquidity in public markets and is completely ad hoc in today’s private credit market.

-

Confidentiality: Nondisclosure agreements are often required for any information to be shared with potential loan purchasers, adding to the information asymmetry.

-

Lack of trading infrastructure: Private credit markets lack centralized reporting, execution, or settlement infrastructure, all details that have become integral to the build-out of robust liquidity in public markets. While public markets and 144A private placement deals can trade seamlessly, many private investment grade and direct lending deals have the additional challenges of physical settlement, which can be onerous for both buyers and sellers.

-

Incentives: Not all private market participants have the same desire for an increase in liquidity. Some prefer the opacity in private markets, while others want to avoid mark-to-market volatility that more often aligns with public markets.

Even if some of these obstacles are addressed, private markets exist precisely because many assets are idiosyncratic and negotiated, making continuous price discovery difficult and often economically inefficient. Attempts to force liquidity into these markets tend to produce thin trading, wide bid‑ask spreads, and unreliable price signals. Rather than improving transparency, sporadic secondary trades often introduce noise, reflecting liquidity needs rather than underlying fundamentals.

The illiquidity premium is the point

There is also a deeper economic tension. A core appeal of private assets is the illiquidity premium earned by long‑horizon investors willing to lock up capital. If private assets were to trade frequently and reliably in secondary markets, that premium would inevitably erode – undermining one of the primary reasons investors allocate to private assets in the first place.

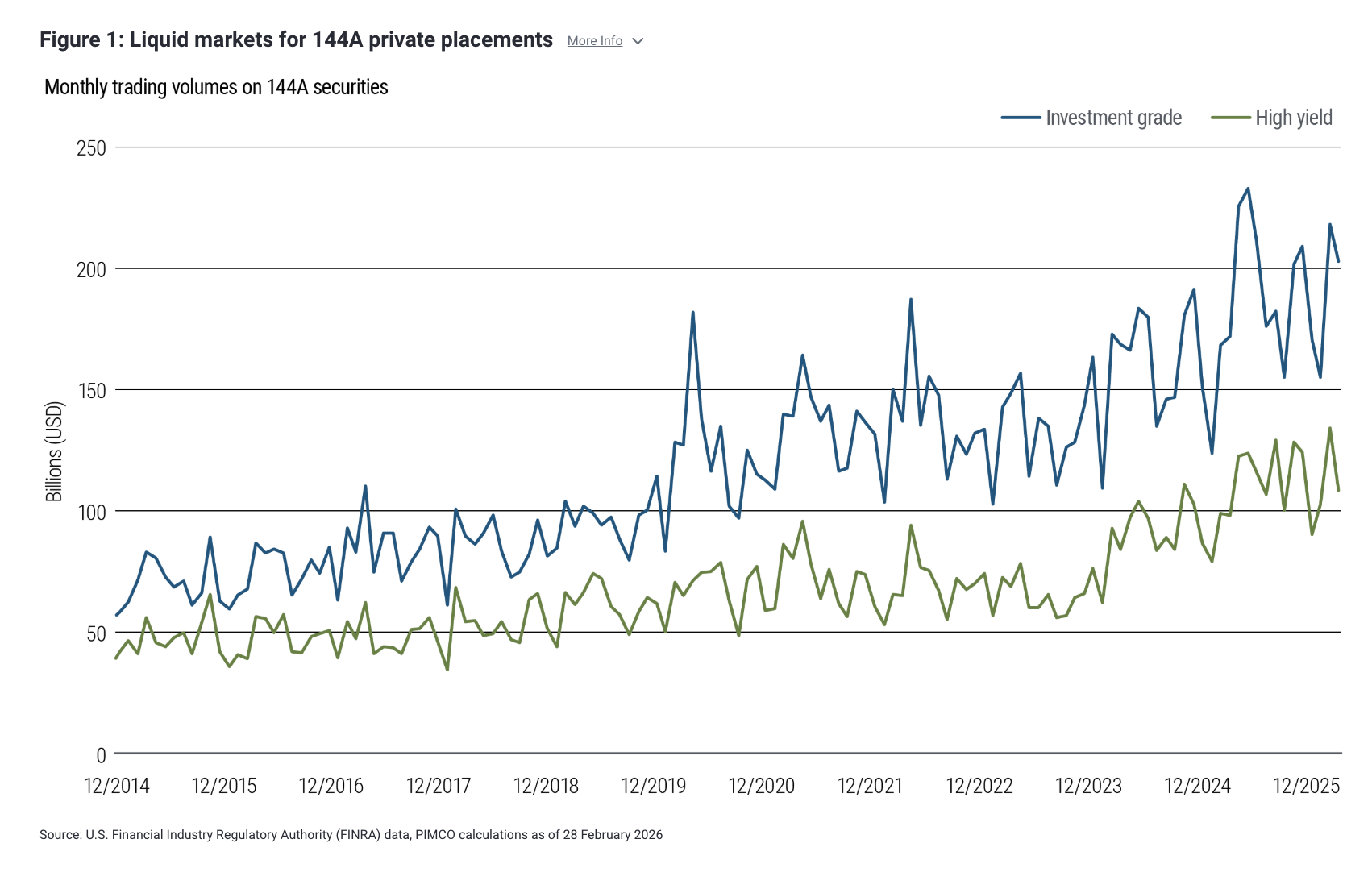

Further, much of the debate around “increased liquidity” in private credit conflates true private assets with 144A private placements, which have been liquid for more than two decades. Recent headlines – driven by a small number of large transactions, including Meta’s $27 billion data‑center financing – highlight the depth of the 144A market, not a structural improvement in liquidity for private credit.

For context, 144A securities represent roughly 18% of the U.S. dollar investment‑grade (IG) market and 82% of high yield (HY), with monthly trading volumes hovering around $200 billion in IG and $100 billion in HY (see Figure 1). It is therefore essential to distinguish the established liquidity of 144A markets from the persistent illiquidity of true private credit, investment grade or otherwise.

Why the syndicated loan playbook doesn’t translate

Finally, while the evolution of the broadly syndicated loan market is often cited as evidence that a once‑private asset class can become relatively liquid and tradable, that comparison overlooks a key distinction. The broadly syndicated loan market’s path to liquidity relied on heavy standardization and the rise of dedicated vehicles such as collateralized loan obligations (CLOs), and more recently ETFs, that created consistent secondary demand.

It is far from clear that private credit can, or should, follow the same path. And if it did, many of the features that at times make private credit attractive to borrowers, including certainty of execution and the ability to provide bespoke capital solutions, would likely be diminished.

A question of risk and compensation

The absence of continuous, mark‑to‑market pricing in private assets should not be viewed as a structural flaw. Rather, it reflects a distinct risk profile, one for which investors must be explicitly and adequately compensated.

Importantly, this risk is not static. Investors’ liquidity needs, constraints, and preferences can evolve over time. Managing this dynamic liquidity risk has therefore given rise to a mature, though costly, ecosystem of solutions, including limited partner (LP) interest transfers, general partner (GP) stake transactions, continuation vehicles, and broader portfolio‑level strategies – all designed to provide flexibility and address shifting liquidity demands.

Jason Mandinach contributed to this report.

Disclosures

All Investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Collateralized Loan Obligations (CLOs) involve a high degree of risk and are intended for sale to qualified investors only. The amount of distributions, if any, on CLOs will be affected by, among other things, the timing of purchases of loans, rates of repayment of or distributions on the underlying assets, the timing of reinvestment in substitute underlying assets and the interest rates available at the time of reinvestment. CLOs are typically illiquid, and holders may not be able to sell these securities at an attractive time or price, or at all. CLOs are also exposed to risks such as credit, default, liquidity, management, volatility, interest rate and credit risk. An investment in an ETF involves risk, including the loss of principal. Investment return, price, yield and Net Asset Value (NAV) will fluctuate with changes in market conditions. Investments may be worth more or less than the original cost when redeemed.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0317-5314365

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO