Saving for college can feel like a monumental task, but families don't have to face it alone. A 529 plan, combined with community support, can turn this daunting challenge into a manageable one. With the average cost of college on the rise, leveraging every available resource is more important than ever.

Why 529 contributions can be a smart gift

-

Tax-free growth and withdrawals: Earnings in 529 plan accounts grow tax free, and withdrawals are not subject to federal income taxes when used for qualified education expenses.

-

Adaptability for diverse educational paths: Funds in a 529 plan can be used for various educational expenses, including tuition, room and board, textbooks and technology, supporting different educational journeys including vocational and technical programs. Lastly, over the past few years we have seen an expansion of how 529 funds can be utilized, most recently for K-12 expenses beyond just tuition (fees, books, other expenses) as well as qualified credentialing programs.

-

Flexibility for all contributors: A 529 plan allows multiple contributors, including parents, grandparents, aunts, uncles, and family friends, making college savings a collective effort.

Building a strong foundation for education

Here's a look at how families can harness the power of a 529 plan and community support to build a strong foundation for a child's future.

The compounding effect: How modest contributions grow

Regular, modest contributions can grow substantially over time due to compounding interest.

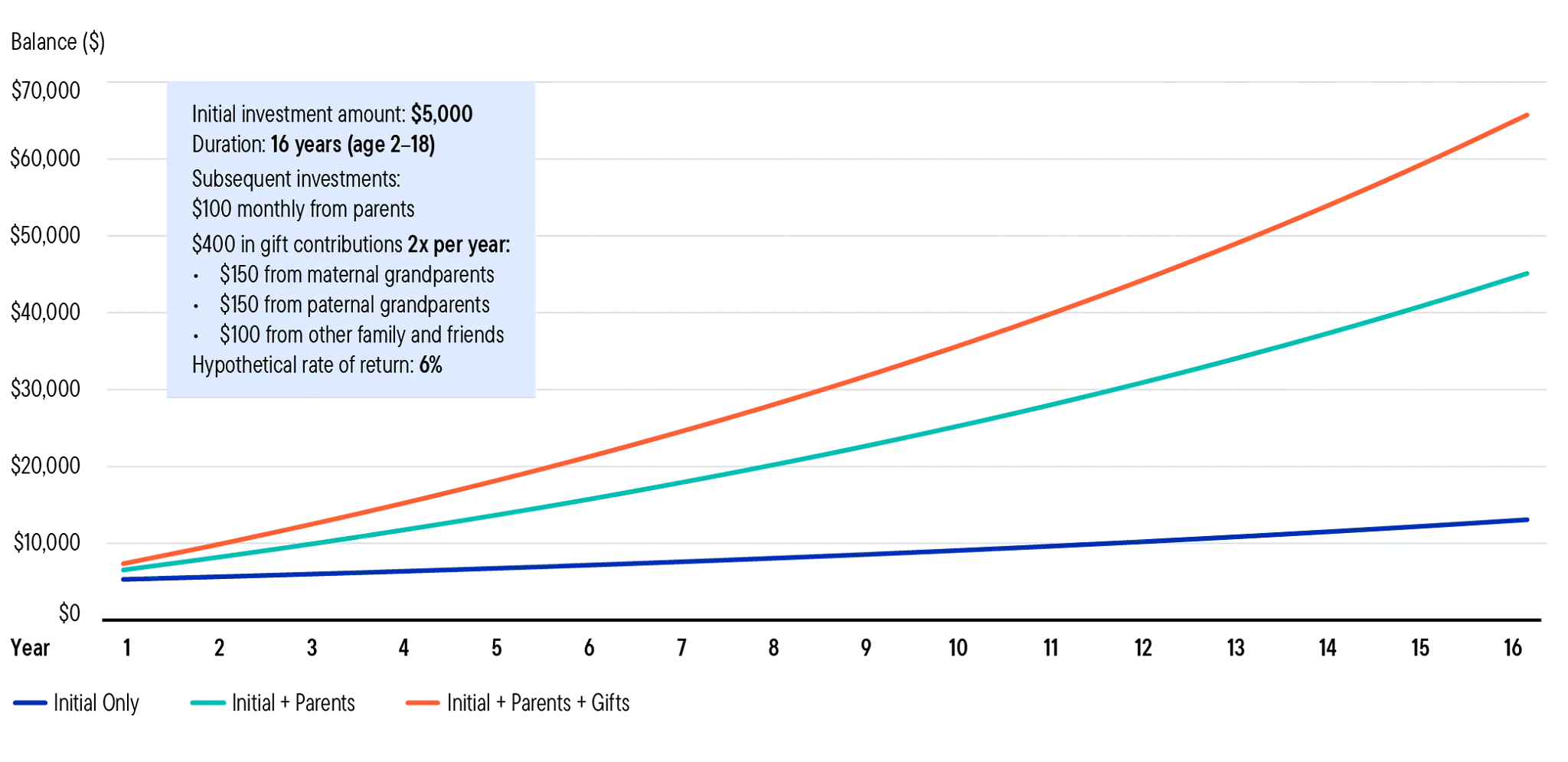

For example, consider this hypothetical example showing how you can maximize your educational savings with the help of family and friends:

A family starts a 529 plan for their two-year-old child with an initial $5,000 contribution and monthly contributions of $100. The child's grandparents and other relatives contribute additional funds on birthdays, holidays and other special occasions. Over 16 years, these collective contributions can add substantially to the total savings, potentially increasing the balance by over $20,000 more than if just the parents were contributing.

Investment Growth Over Time

Source: Franklin Templeton hypothetical calculation.

Illustrative, hypothetical analysis using a 6% annual return with monthly compounding; actual results will vary. Assumes the contributions provided; fees, taxes, trading costs, timing frictions, and cash drag are excluded. Gifts modeled as semiannual deposits; timing differences changes outcomes.

Past performance is not indicative of future results. This is not investment, legal or tax advice.

Advanced gifting (Superfunding)

This strategy allows a lump-sum contribution without triggering a gift tax and can be advantageous for end-of-year giving.

-

How it works: In 2025, an individual can contribute up to $95,000 at one time to a beneficiary's 529 plan, while a married couple can contribute up to $190,000. This represents applying five years’ worth of the annual gift tax exclusion ($19,000 for individuals, $38,000 for married couples electing split gifts).

-

Tax implications: The contribution is treated as if it is spread over five years for gift tax purposes.

-

Filing requirements: IRS Form 709 must be filed, electing to treat the gift as if it were made over five years, during which no additional taxable gifts can be made to the same beneficiary.

Engaging family and friends: Three ways to rally support

-

Start the conversation: Families can share their college savings goals with relatives and friends at gatherings or during discussions about the future, explaining how others can contribute.

-

Get creative with contributions: Instead of traditional gifts, families might suggest a "birthday contribution" tradition or a matching challenge for family and friends.

-

Educate on giving a 529 as a gift: Many 529 plan providers offer online gifting platforms where contributors can use a personalized link or code. Contributions can also be made by mailing a check directly to the plan with the beneficiary's name and account number.

As year-end approaches, it is an ideal time to consider gifts to family members, including 529 plans. We recommend consulting with a tax advisor is recommended to determine the best strategy for specific financial situations. By combining the tax advantages of a 529 plan with community support, families can create a robust college savings fund, providing a strong foundation for a child's future.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© Franklin Templeton

Read more commentaries by Franklin Templeton