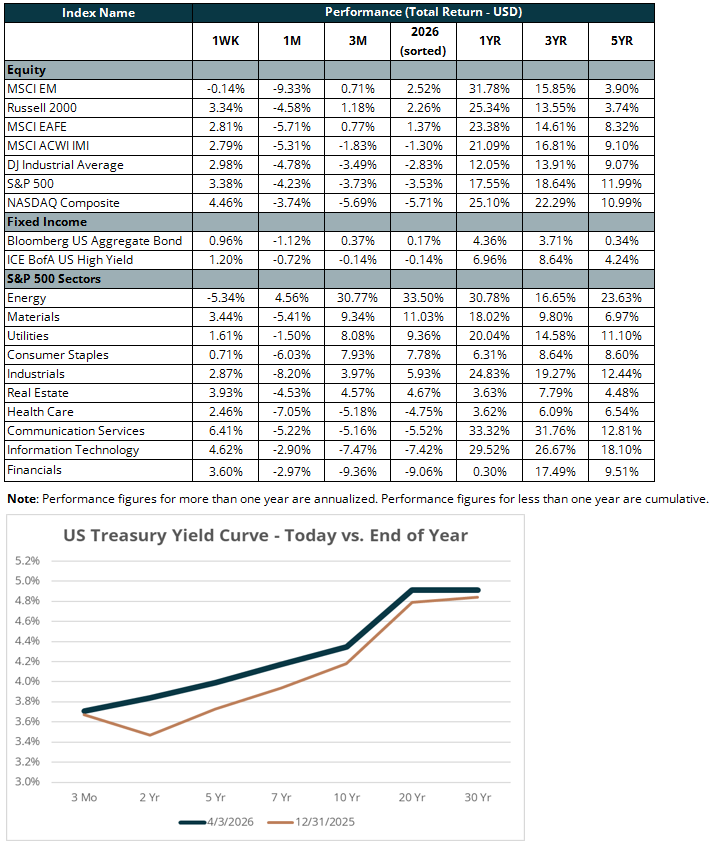

Equity markets staged a meaningful recovery last week, driven by optimism of a ceasefire in Iran. The S&P 500 returned 3.4 percent, the NASDAQ gained 4.5 percent, and the Dow Jones Industrial Average added three percent – the best weekly performance in recent memory. All three averages remain in negative territory year to date (YTD), after valuations entered the year at historically high levels.

The early optimism of Monday’s morning trading faded into a losing session, but Tuesday changed the tone entirely. An unconfirmed report suggested the Iranian President might be open to peace talks, triggering a sharp risk-on rally. Biotech and Magnificent 7 stocks surged. Oil, which might have been expected to crater on legitimate ceasefire news, fell only 0.8 percent. Energy traders were skeptical, noting the report contained little that was genuinely new, and questions continue as to whether the Iranian President holds real authority or is merely a figurehead.

Wednesday brought fresh anticipation as markets continued to rally ahead of the President’s evening address. Stock futures declined during the speech, however, as the President’s assertive tone seemed to outweigh possibilities for a ceasefire. At one point, the President promised to “send Iran back to the Stone Age where they belong.” The week’s gains ultimately held, but the whipsaw trading underscored the current fragility of the markets.

Last week marked a sharp reversal in the sector leadership that has defined much of 2026. Energy, the year’s standout performer, gave back 5.3 percent last week. Every other sector finished in positive territory, on the back of an optimistic outlook on the war in Iran. Six of the Magnificent 7 stocks posted meaningful weekly gains, with Tesla (TSLA) the lone exception. Despite this, all Mag 7 stocks remain deeply under water for the year, with Microsoft (MSFT) leading the group lower at 23 percent.

Despite negative returns YTD, forward earnings growth expectations for the S&P 500 have risen from roughly 15 percent at the start of the year to 17 per cent today. Both estimates are well above the nine percent annualized pace over the past decade. Compression of valuation multiples has driven the S&P 500’s performance this year, explaining why growth stocks (trading at elevated valuations) have sharply lagged their value counterparts (-8.7 percent vs. +3.1 percent).