Key Takeaways

- Banks and chip names kicked off earnings season with robust results last week

- The S&P 500® is projected to deliver its sixth consecutive quarter of double-digit earnings growth at 13.2%, fueled largely by a powerhouse 45% expansion in the Information Technology sector.

- CEOs appear confident as the earnings season kicks off according to our latest LERI reading

The Q1 2026 earnings season has officially started, and the early results suggest a market that is largely defying the geopolitical fog we’ve discussed.

Big bank earnings last week revealed a significant bifurcation between Wall Street and Main Street, as powerhouse investment banking rebounds offset a more cautious outlook on lending. Goldman Sachs led the charge with a 48% surge in investment banking fees and a blowout $17.55 EPS1, while JPMorgan2 and Bank of America3 reported healthy consumer spending despite trimming their full-year Net Interest Income guidance. Morgan Stanley4, Citigroup5, and Wells Fargo6 also delivered solid beats, though their CEOs collectively signaled a "complex set of risks." Jamie Dimon highlighted that while the economy remains resilient, persistent inflation and geopolitical tensions make the long-term outlook harder to navigate than in previous cycles.

In the semiconductor space, TSMC and ASML served as the definitive AI bellwethers, proving that the appetite for high-end infrastructure remains insatiable. TSMC posted record Q1 revenue on the back of surging 2nm and 3nm chip demand7, while ASML raised its full-year 2026 sales guidance to as high as €40 billion, citing an "AI Supercycle" that is outpacing current tool supply.8 These results suggest that chip names are being fueled by a structural infrastructure race rather than cyclical hype, as memory makers like Samsung and SK Hynix accelerate capacity expansions to keep up. While ASML warned of a minor "air pocket" in Q2 due to timing, the overarching theme is that AI demand is providing a massive floor for the industry.

Including reports from 28 S&P 500 names last week, the blended EPS growth rate increased to 13.2% from 12.6% last week, the sixth quarter of double digits bottom-line growth. Revenue growth ticked up to 9.9% from 9.8% last week, the highest top-line growth rate since Q3 2022.9

On Deck this Week: Tech, Autos, and Economic Anchors

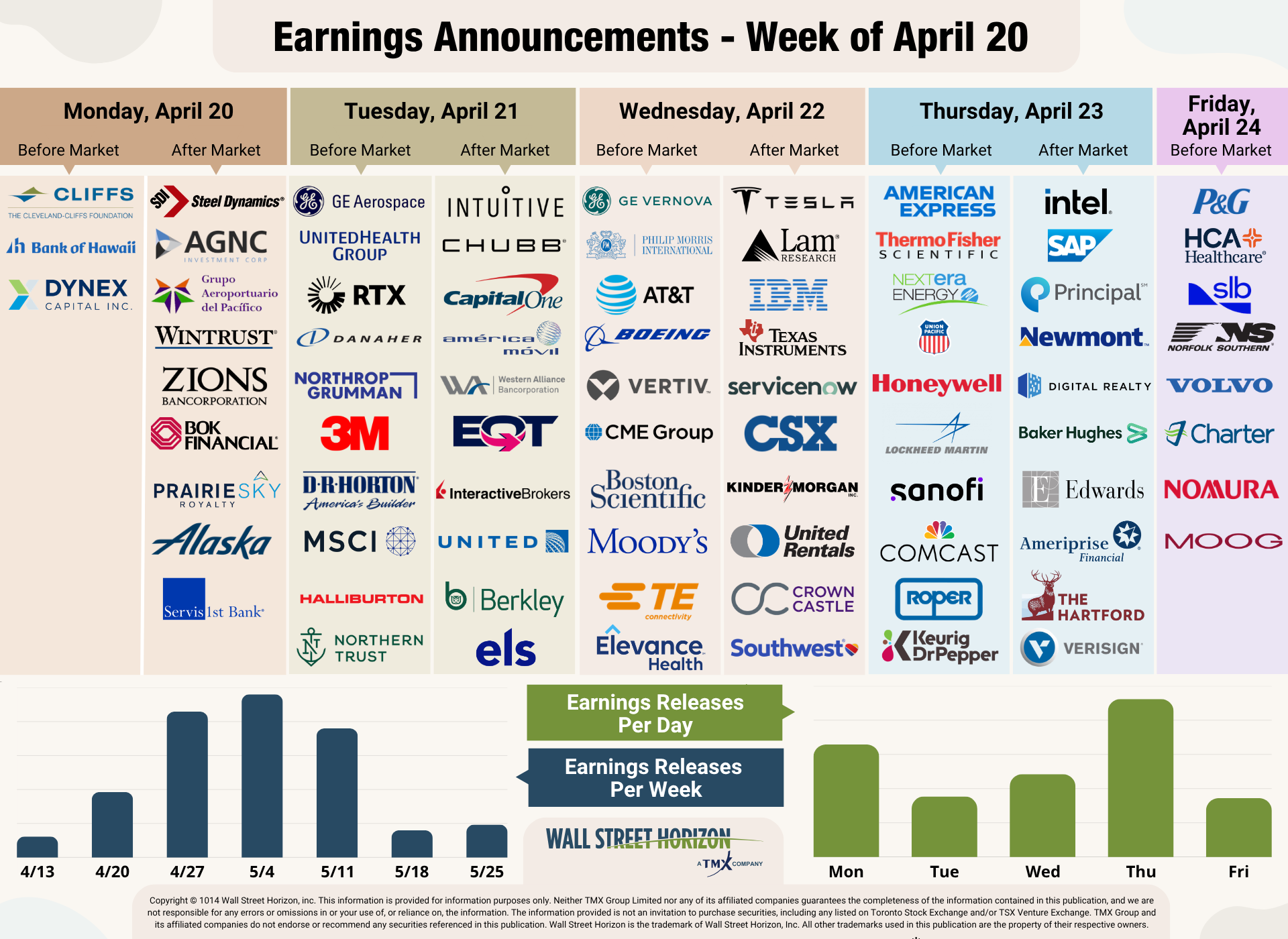

Looking ahead to next week, the spotlight shifts to the tech giants and the first look at big auto following the 2025 tariff resets. We expect high-stakes reports from Tesla, IBM, Intel and UnitedHealth, alongside industrial heavyweights like Boeing and 3M.

On the economic front, all eyes will be on Retail sales out Tuesday, April 21 and University of Michigan’s Survey of Consumers out on Friday, April 24.

Read more: Double-Digit Growth and the Visibility Gap

Source: Wall Street Horizon

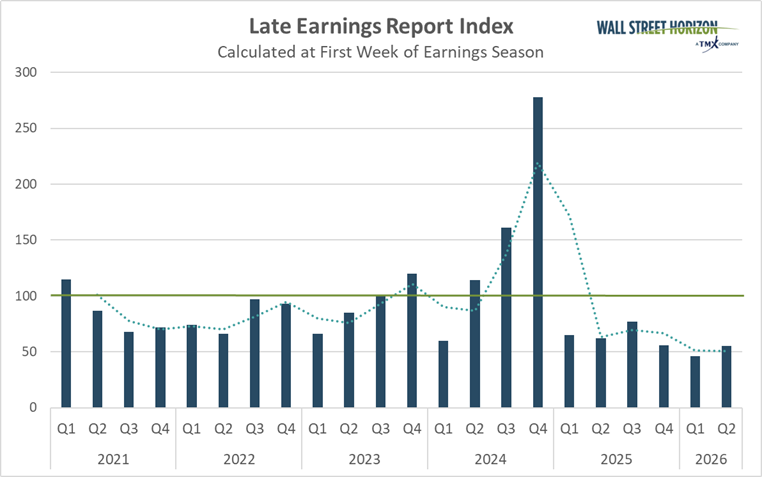

CEOs Signaling Confidence in 2026

After rising to its highest level in four years during the last quarter of 2024, the Late Earnings Report Index, our proprietary measure of CEO uncertainty, has now recorded six consecutive quarterly readings below the historical benchmark as companies prepare to report their Q1 results.

The LERI tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, and anything above that indicates that companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests that companies feel they have a pretty good handle on the near-term.

The official pre-peak season LERI reading for Q1 earnings (reported in Q2) stands at 55, the lowest Q2 LERI ever recorded in our eight years of data. This is well below the baseline reading, suggesting when companies announced their earnings dates they were feeling more certain about economic conditions. As of April 14, there were 34 late outliers and 56 early outliers.

Source: Wall Street Horizon

Q1 2026 Earnings Wave

The peak weeks of the Q1 earnings season are expected to fall between April 27 - May 15, with each week expected to see over 2,500 reports. Currently, May 7 is predicted to be the most active day with 1,156 companies anticipated to report. Thus far, only 58% of companies have confirmed their earnings date (out of our universe of 11,000+ global names). The remaining dates are estimated based on historical reporting data.

Source: Wall Street Horizon

The Bottom Line

The takeaway these early weeks of Q2 is that corporate performance is now serving as the definitive anchor for a market previously adrift in macro uncertainty. While geopolitical volatility and oil projections have dominated the headlines, investors are increasingly looking to the actual results from U.S. corporations to validate the soft landing narrative. With early earnings reports confirming that the engine of the U.S. economy remains robust, the low LERI reading of 55 acts as a vital cross-check, suggesting that management teams aren't just surviving the noise but are operating with a high level of visibility. As we head into the heart of the reporting wave, these earnings will act as the ultimate reality check, determining whether corporate resilience can continue to outpace global tensions.

1 Goldman Sachs First Quarter 2026 Earnings Results, April 13, 2026, https://www.goldmansachs.com

2 JPMorgan Chase First Quarter 2026 Earnings Results, April 14, 2026, https://www.jpmorganchase.com

3 Bank of America First Quarter 2026 Earnings Results, April 16, 2026, https://d1io3yog0oux5.cloudfront.net

4 Morgan Stanley First Quarter 2026 Earnings Results, April 15, 2026, https://www.morganstanley.com

5 Citigroup First Quarter 2026 Earnings Results, April 14, 2026, https://www.citigroup.com

6 Wells Fargo First Quarter 2026 Earnings Results, April 14, 2026, https://www.wellsfargo.com

7 TSMC First Quarter 2026 Earnings Results, April 16, 2026, https://pr.tsmc.com

8 ASML First Quarter 2026 Earnings Results, April 15, 2026, https://ourbrand.asml.com

9 FactSet Earnings Insight, John Butters, April 17, 2026, https://advantage.factset.com

Copyright © 2026 Wall Street Horizon, Inc. All rights reserved. Do not copy, distribute, sell or modify this document without Wall Street Horizon's prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities, including any listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. This publication shall not constitute an offer to sell or the solicitation of an offer to buy, nor may there be any sale of any securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, and TSX Venture Exchange are the trademarks of TSX Inc. and are used under license. Wall Street Horizon is the trademark of Wall Street Horizon, Inc. All other trademarks used in this publication are the property of their respective owners.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Wall Street Horizon

Read more commentaries by Wall Street Horizon