Key market views

-

We lean into AI, growth, and large cap exposures, but see value as an important diversifier. Earnings in the U.S. have been steadily revised higher, even as volatility spiked and prices slid.

-

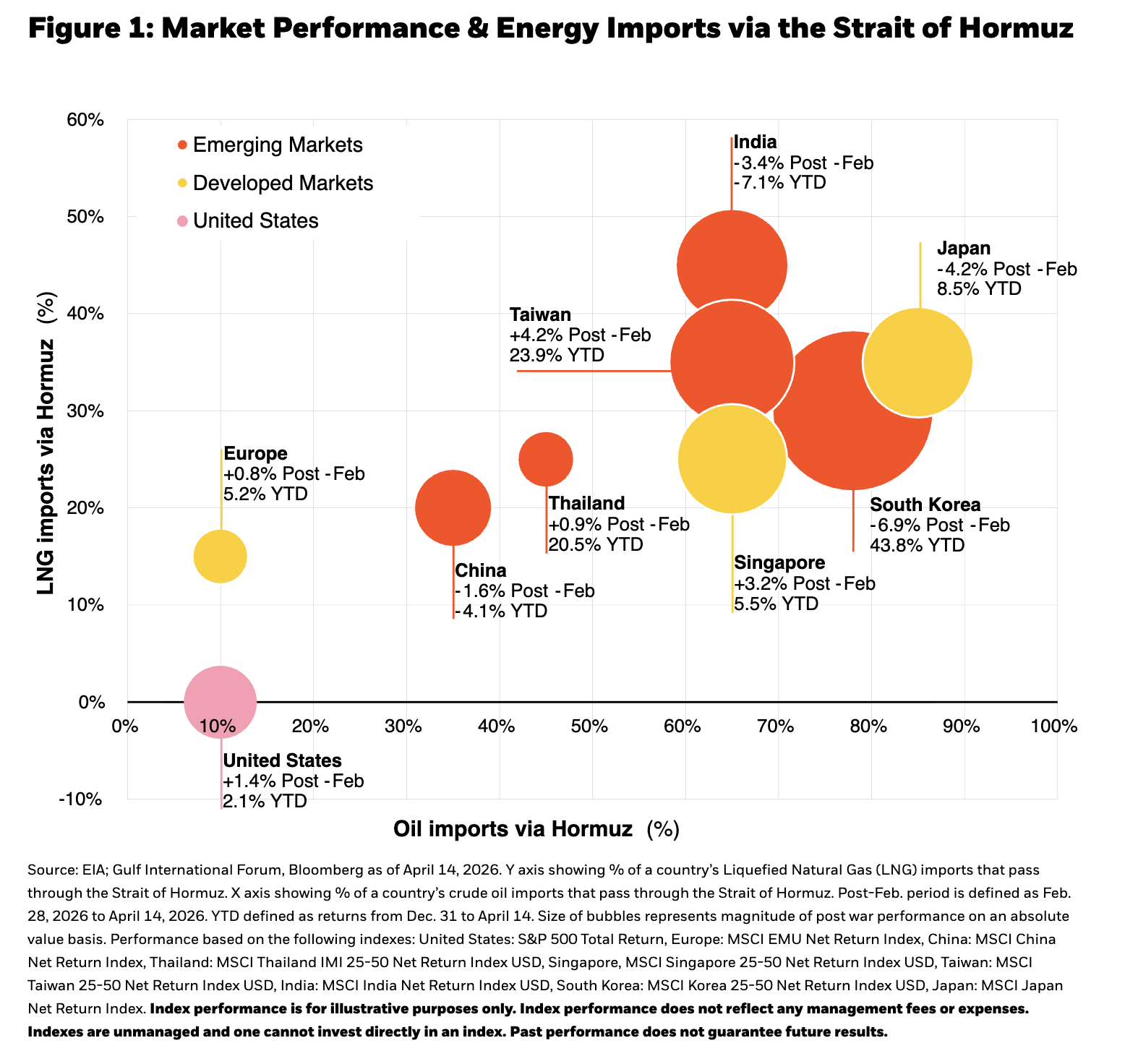

Outside the U.S., we prefer emerging over developed market equities, given the centrality of many EM countries in the ongoing AI buildout. Global themes such as energy security and infrastructure are likely to remain in focus long after conflict ends.

-

In fixed income, we prioritize income and see opportunities in securitized assets over corporate credit.

-

We favor a diversified basket of diversifiers, such as alternative asset classes and liquid alternative strategies. Traditional diversifiers such as duration and gold sold off alongside equities in March, a reminder that ballast is not one-size-fits-all.

The spring edition of our Investment Directions takes on a new look. As the weather heats up, our “summer body” of work embraces a slimmed down word count, Q&A format, and visual-first approach – better for consuming on the go, or preferably, outdoors.

That’s not to say the world is less complicated because the weather is better. The start of this year has seen the largest oil supply disruption in history. Prior to the conflict in the Middle East, the market was fretting about the death of software (the “DiSaaSter”), and other ways AI could disrupt existing business lines or generally fail to live up to hype.

While there are doubtless risks on the horizon, we also see opportunities: in the resilience of the U.S. economy, the continued strength in corporate earnings, and the relentless growth of AI and near-endless demand for compute. We retain a constructive outlook for risk assets, while building a diversified basket of diversifiers to gird portfolios against a growing array of potential shocks.

Latest in Markets: Inflation rising, Fed likely holds near-term

1. What does the conflict in the Middle East mean for the U.S. economy?

The Middle East conflict is pushing oil prices higher, but the implications for the U.S. economy - and markets - are more nuanced. The U.S. is less exposed than many peers given its role as a net energy exporter, which has helped cushion the growth impact relative to more import-dependent economies. Higher energy prices will still weigh on consumers, particularly via gasoline, but we expect that drag to be partially offset by fiscal support, including tax refunds.

Importantly, U.S. earnings have not been especially sensitive to oil unless disruptions persist. Historically, even large oil moves have tended to slow earnings growth rather than reverse it: since 1970, S&P 500 earnings have generally remained positive following oil increases of up to ~70% year-over-year, with negative outcomes concentrated in more extreme shocks - typically when oil spikes coincide with broader downturns.1

Consensus forecasts for GDP continue to average 2%, though we see some evidence of recent slowing.2 Perhaps more importantly, growth has become more reliant on a narrow set of drivers associated with AI and investment spending, which could make it more fragile. We think that backdrop supports staying invested in equities, despite headlines around inflation and growth shocks, while being more deliberate about diversification as volatility remains elevated.

At the same time, energy infrastructure disruption may cause energy prices to remain higher than levels seen at the start of the year. Higher energy prices may reinforce longer-term themes around energy security and supply resilience, which could drive increased investment in defense and infrastructure even after the conflict fades. Policymakers are likely to prioritize rebuilding and expanding strategic reserves and reducing reliance on vulnerable supply routes - potentially putting a higher floor under oil prices from here.

2. What is the outlook for inflation and the Fed?

Inflation is moderating, but the path remains uneven. Headline inflation has moved higher given energy price shocks while core inflation remains sticky around the 2.6% level – above the Fed’s target.3 While near-term pressures remain elevated, reflecting supply-side dynamics and geopolitical uncertainty, they are not driving a broad-based reacceleration in market-based measures of inflation. Indeed, there are some signs of inflation moderation: as recent CPI data show, near-term disinflation is being supported by tariff runoff in certain goods categories and continued shelter deceleration.

For the Fed, this creates a mild stagflationary trade-off. Historically, similar shocks have led to an initial focus on inflation before growth concerns dominate. However, this shock alone is unlikely to warrant further tightening. As stated at the March FOMC meeting, Federal Reserve Chair Jerome Powell believes interest rate policy is already restrictive, with the funds rate estimated at 50–75 basis points above neutral and financial conditions tighter by ~80 bps.4

We believe this leaves the Fed on pause and data-dependent for now, but likely to shift toward gradual rate cuts later if inflation continues to move toward target and growth moderates. With headline inflation expected to stay elevated in the near term, and the next move from the Fed likely a cut, we believe investors should focus on adding real rate protection to their portfolio via inflation-protected securities.

Read more here: BlackRock's Spring 2026 Investment Directions

Endnotes:

1. BlackRock, Bloomberg. Analysis of S&P 500 earnings and WTI crude oil prices from 1970 - 2022. Oil shocks defined as YoY increases in WTI prices; earnings measured as next 12-month S&P 500 EPS growth following each observation. As of March 6, 2026. Past performance does not guarantee future results.

2. Consensus forecasts based on Bloomberg survey-based estimates as of 4/14/26 for U.S. 2026 GDP growth on a quarter over quarter seasonally adjusted annual rates (QoQ SAAR) and year-over-year (YoY) measures. Forward looking estimates may not come to pass.

3. U.S. Bureau of Labor Statistics, Consumer Price Index Excluding Food and Energy. Data for March 2026 (released 4/10/26).

4. Federal Reserve Board, Laubach-Williams estimates as of April 1, 2026. A basis point is one hundredth of 1 percentage point.

Read related: Economy and Markets Likely to Prove Resilient

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© BlackRock

Read more commentaries by BlackRock