Markets have long struggled to price geopolitical risk. Part of the issue is that each flare-up tends to be viewed as a one-off volatility jolt to be weathered and then faded once there is resolution.

Today, however, geopolitical risk is no longer a series of isolated events. It’s a defining feature of a more fragmented, multipolar world (for more, see our 2025 Secular Outlook, “The Fragmentation Era”). Multinational institutions no longer function as reliably as they once did. Stability has eroded.

Perhaps more than ever, geopolitics directly shapes trade flows, supply chains, industrial policy, energy security, defense spending, fiscal policy, inflation, and growth. In other words, geopolitics is now an essential economic input. As a result, it is an increasingly important input into investment decisions as well.

Passive investment strategies were well-suited to a world of low geopolitical risk, central bank balance sheet abundance, and compressed volatility. That world is gone. In its place is an environment that distributes risk unevenly – creating distinct winners and losers across countries, sectors, and asset classes.

Navigating that dispersion requires flexibility: the ability to rotate, adjust, and exploit dislocations that a passive index, by construction, cannot. In our view, agile, multi‑sector approaches are best positioned for this environment, where it will be critically important to price risk objectively. Successful investors will need to discern across multiple sectors and security types, as well as liquidity profiles, to choose the best risk adjusted opportunities to deliver returns.

Read more: Higher Energy Costs, Weaker Tax Relief Squeeze U.S. Households

Start with the initial conditions

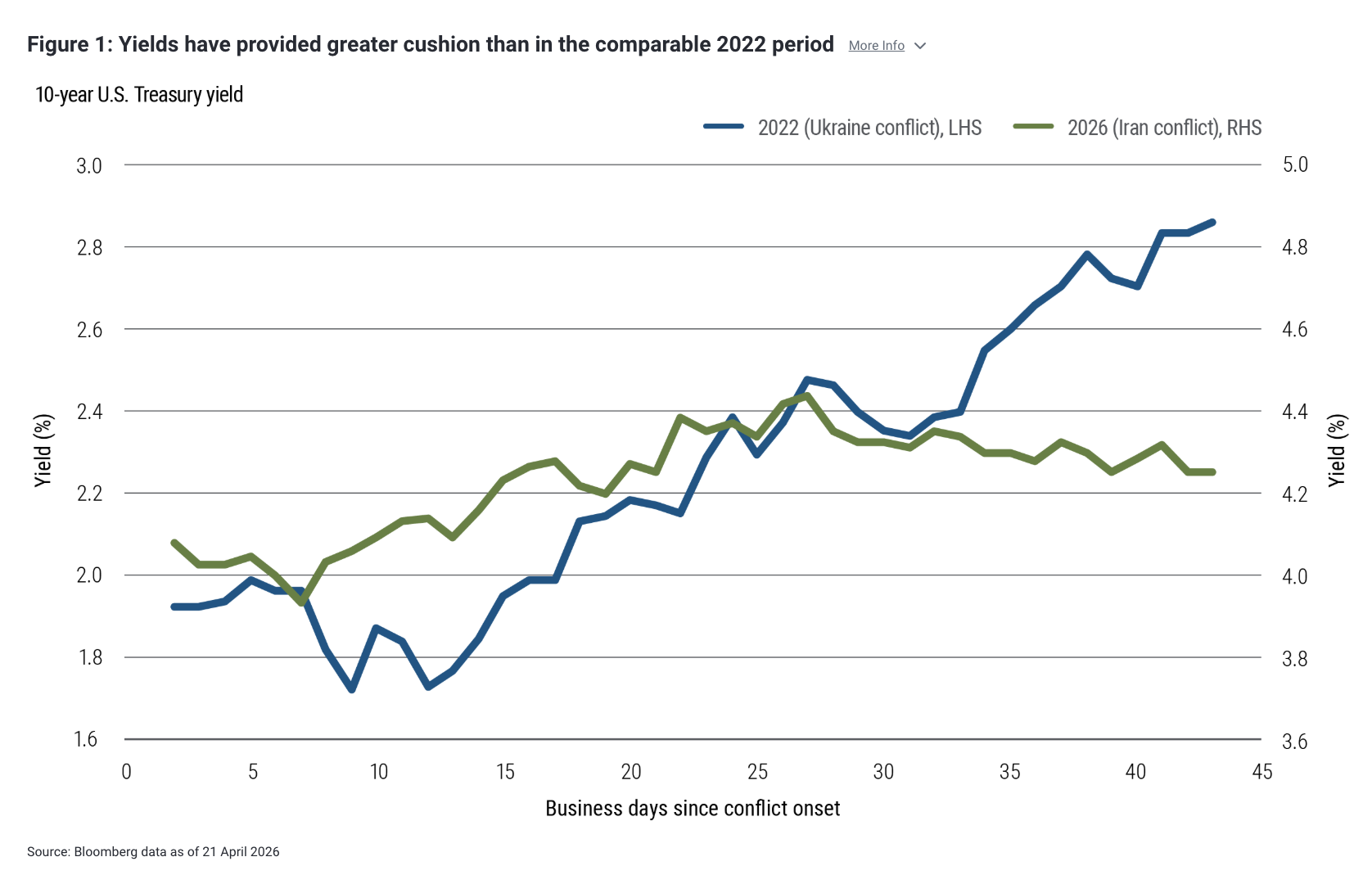

It’s tempting to view recent conflict-driven volatility through the lens of early 2022, when Russia invaded Ukraine. That year’s energy shock hit a post-pandemic global economy marked by pent-up imbalances, while bond yields were near all-time lows. As inflation surged, stocks and bonds sold off together, correlations spiked across asset classes, and diversification appeared to vanish just when it was needed.

The defining difference between then and now is the starting point of yields. Bond yields are much higher today than in 2022, providing far greater cushion for investors. As a result, even during recent stress, fixed income has demonstrated a greater ability to absorb shocks.

Lean into dispersion

Geopolitical volatility doesn’t affect all countries or asset classes equally. Broader market performance, or beta, matters less when winners and losers are increasingly distinct.

Geopolitical fragmentation rewards selectivity. This can be observed today within emerging markets, for example, where the lines of differentiation and resilience are increasingly drawn between energy exporters versus importers (for more, see our March 2026 Cyclical Outlook, “Layered Uncertainty: Conflict, Credit Stress, and AI”).

Targeted tools for inflation hedging

Since the Middle East conflict began, inflation has been a foremost market concern, highlighting the role that inflation-linked bonds can play in portfolios. For example, in the U.S., Treasury Inflation-Protected Securities (TIPS) can be an effective tool. However, they also draw occasional criticism during volatile periods: When real (inflation-adjusted) yields rise, longer-dated TIPS prices can still fall due to interest rate risk even as inflation risks increase.

Approaches that emphasize shorter-dated inflation-linked bond exposures and more targeted tools such as inflation swaps can enhance the inflation-hedging properties in portfolios. This can better isolate inflation mitigation while managing sensitivity to yield movements.

Look for opportunities in commodities

Over the past couple of months, one asset class behaved largely as theory would suggest: commodities, which have seen large price swings and often sharp gains as inflation expectations rose.

Importantly, outsize short-term volatility tends to reset risk premia, or the amount of compensation investors receive for specific risks. In commodities, this has created tremendous longer-term opportunities, particularly for investors focused on relative value – for example, across commodity curves and cross-commodity relationships – rather than directional bets.

Conclusion: Building resilience for an age of geopolitical volatility

To strengthen resilience, investors should construct portfolios to adapt to both episodic shocks as well as structural shifts in a more geopolitically driven market environment.

Over short time horizons, particularly during bouts of stress, correlations across asset classes can appear skewed and diversification may seem elusive. Yet, when portfolios are built for long-term resilience, diversification can reassert itself.

Flexible multi-sector strategies – dynamic bond funds and income-oriented portfolios – are built for precisely today’s regime. These strategies can lean into dispersion, pursue targeted inflation mitigation, and capture relative value.

This is a world that rewards the adaptive and penalizes the rigid. Flexibility isn’t just a feature of good portfolio construction today. It is the strategy.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government.

Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0420-5413826

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO