Key Takeaways:

- Energy-driven inflation pressures are likely to rise near term

- We believe current conditions differ materially from the 2022 inflation surge

- Central banks may look through initial inflation increases

- Portfolio positioning should balance inflation risk with growth resilience

Inflation Pressures Build, But Starting Point Matters

Back-and-forth developments over the weekend around the Strait of Hormuz have added near-term volatility to energy markets. That uncertainty is feeding into oil prices and reinforcing questions about how persistent energy-driven inflation pressures could become, particularly if disruption risks continue to ebb and flow. Although the March U.S. core inflation data was a touch softer than consensus expectations, near-term core inflation could continue to rise amid the geopolitical tensions. While energy prices do not directly enter core inflation, second-round effects are already expected to emerge through channels such as transportation and services. For instance, many airlines have already begun raising airfare and checked baggage fees to offset higher jet fuel costs.

This indirect transmission reinforces that even targeted shocks can have wider inflation implications across the economy. But we think investors can still take some comfort in knowing that this inflation cycle might be different than the 2022 experience.

Why This Cycle Differs From 2022

The current inflation backdrop differs from the conditions that drove the 2022 surge. At that time, inflation was fueled by both supply disruptions and a strong demand rebound, alongside an overheated labor market and elevated shelter costs. These forces pushed core inflation to significantly higher levels than today. U.S. core inflation peaked at nearly 7% year-over-year in 2022, compared to a core inflation rate of 2.6% year-over-year in March 2026.

By contrast, the current inflation backdrop starts from a more balanced position. The U.S. labor market, while stabilizing, is not overheated. And in some parts of the world (e.g. Canada and the United Kingdom), the labor market might even be weaker than longer-term equilibrium levels. Meanwhile, interest rates are no longer near zero and instead sit at neutral or restrictive levels. Housing-related inflation is also more subdued, reflecting still-elevated mortgage rates.

These differences matter for how inflation evolves. Without the same combination of demand strength and structural constraints, the risk of a sustained inflation surge appears lower, even if near-term readings move higher. Of course, geopolitical uncertainty still remains elevated, and while a prolonged closure of the Strait of Hormuz is not our base case, such an outcome cannot be ruled out. For now, we think investors would benefit from staying close to strategic asset allocations, while carefully monitoring medium-term inflation developments.

Central Banks Might Not Hike Rates Immediately

Energy shocks can boost price pressures and weigh on growth. But monetary policy is a blunt tool, and cannot simultaneously address both impacts. As such, central bankers must carefully consider how to respond, taking into consideration the starting point conditions in their respective economies. In some instances, central banks may be willing to tolerate a short-term boost in inflation, if it is primarily driven by energy-related factors.

But if geopolitical tensions persist, resulting in inflationary pressures broadening out and medium-term inflation expectations rising, central banks may need to respond more actively. The path of policy therefore remains closely tied to the duration and intensity of the shock.

In the United States, the conflict in the Middle East is likely to extend the Fed’s pause on rate cuts, but unlikely to result in near-term rate hikes. As we’ve previously noted, the U.S. may be more insulated from the price impacts of the energy shock than other countries, given that today it is a net energy exporter. Given that the Federal Reserve has an explicit dual mandate of supporting economic growth while keeping prices stable, and given that interest rates in the U.S. are currently still somewhat restrictive, we think the Federal Reserve can afford to tolerate a near-term boost in inflation, eliminating the need for rate hikes.

The decision might be more challenging for other central banks. Europe has seen a spike in natural gas prices, as reserves had already been significantly drained in the aftermath of the Russia-Ukraine conflict. Consequently, the ECB may be less willing to accommodate a near-term boost in inflation compared to the Fed. While we think it’s unlikely that the ECB will raise rates at its April meeting, the prospect of a modest 25 basis point rate hike at some point this year remains on the table should the energy shock persist.

The Bank of England faces an even more challenging dilemma than the ECB. Like continental Europe, Britain is also feeling the sting of elevated natural gas prices. But the British economy is weaker than the economy in continental Europe, with the unemployment rate near its recent cyclical peak. While we cannot rule out a modest 25 basis point rate hike by the Bank of England this year, we believe that any rate hike may have to be followed by rate cuts in 2027 to re-stabilize economic growth.

In Canada, although Bank of Canada Governor Tiff Macklem has cautioned against both hiking interest rates too early or too late, we continue to believe that rate hikes in 2026 are unlikely. In recent statements, Governor Macklem has shown a willingness to focus more on medium-term inflation dynamics over near-term price pressures. In addition, Canada’s economy remains under pressure, with headline growth alternating between expansion and contraction from quarter to quarter, and the unemployment rate remaining weaker than the longer-term equilibrium.

Finally, although the Reserve Bank of Australia had been hiking interest rates even before the outbreak of the Iran war, some of the labor market indicators have weakened recently. We think it’s unlikely that the RBA will want to raise rates further, especially given interest rates are already in restrictive territory.

For portfolios, the energy shock emphasizes the importance of the incoming economic data, as different central banks could use different playbooks.

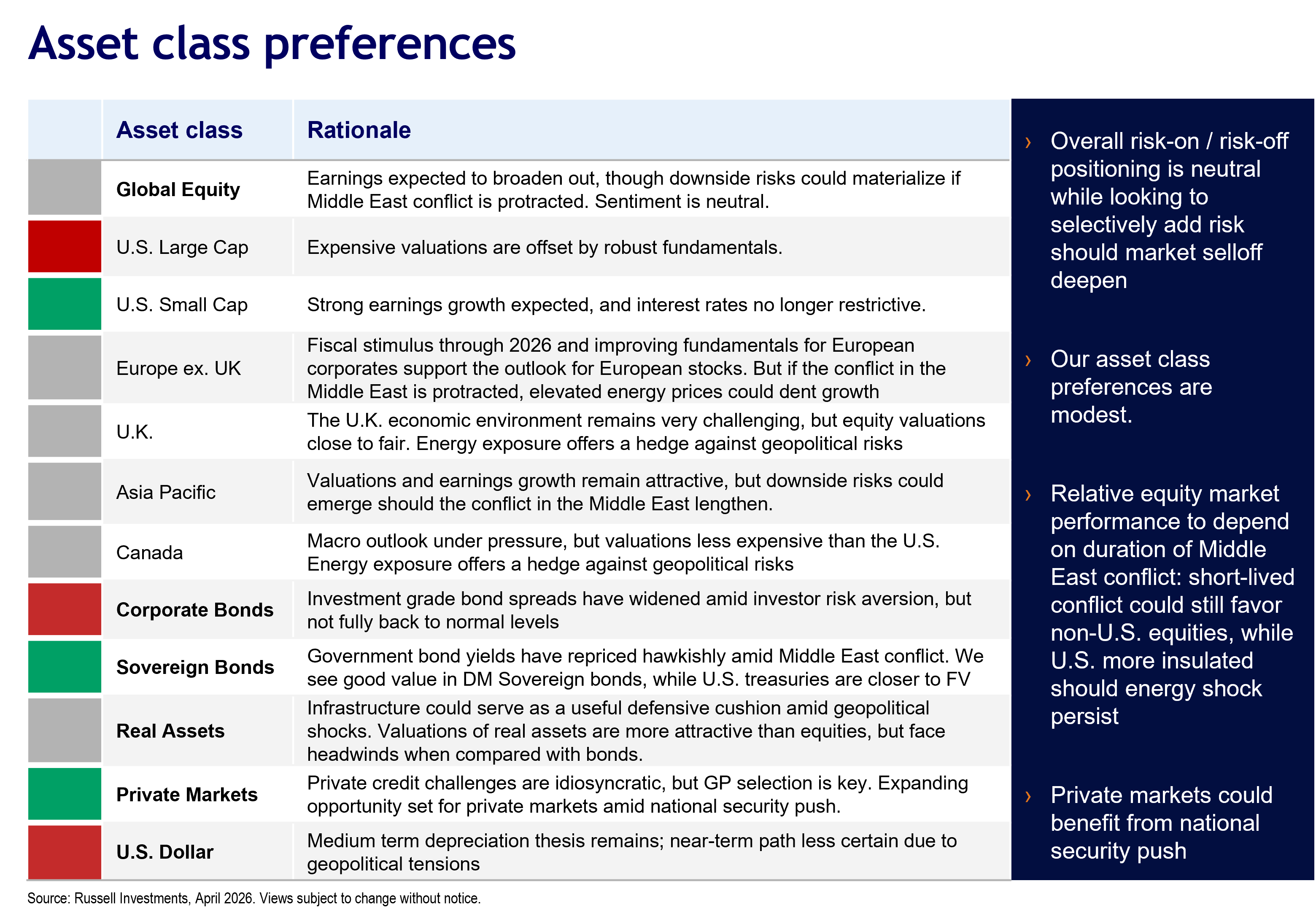

Inflation Impact Across Asset Classes

The inflation impulse from higher energy prices is uneven across asset classes, as reflected in current positioning. Large energy consumption regions (such as Emerging Markets) could see a larger impact from the energy shock. Meanwhile, markets with embedded energy exposure (such as the UK and Canada) could see higher energy sector earnings offset weaker earnings from the consumer discretionary sector. In the U.S., consumption as a share of total personal spending has decreased compared to the 1970s. This could enable its economy to be resilient even if energy prices are somewhat elevated.

In fixed income, sovereign yields have already adjusted higher than pre-war levels, creating opportunities in some regions. Meanwhile, credit spreads have widened but do not yet reflect a full inflation shock. Infrastructure stands out as a more direct beneficiary, given its link to inflation-sensitive revenues and defensive characteristics.

One key challenge for investors’ asset allocation is that starting conditions also have to be taken into consideration. For instance, even though emerging market equities might be more sensitive to energy prices than U.S. equities, emerging markets are currently trading at a significant valuation discount to U.S. equities. How things “net out” could depend largely on the length of the energy shock. For portfolios, this heightened uncertainty supports maintaining diversified exposures with selective tilts rather than broad repositioning.

Investor Implications

We continue to see value in maintaining balanced exposure to growth and inflation-sensitive assets, recognizing that inflation may rise in the near-term but is unlikely to mirror 2022 dynamics. The recent hawkish repricing in bond yields may potentially be over-done, creating some attractive valuations in non-U.S. government bonds. In addition, including an allocation to assets like infrastructure could help make the portfolio more resilient to both upside inflation risks and downside growth risks.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Diversification and strategic asset allocation do not assure a profit or guarantee against loss in declining markets.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The Russell Investments logo is a trademark and service mark of Russell Investments

The information, analyses and opinions set forth herein are intended to serve as general information only and should not be relied upon by any individual or entity as advice or recommendations specific to that individual entity. Anyone using this material should consult with their own attorney, accountant, financial or tax adviser or consultants on whom they rely for investment advice specific to their own circumstances.

Products and services described on this website are intended for United States residents only. Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained on this website should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Persons outside the United States may find more information about products and services available within their jurisdictions by going to Russell Investments' Worldwide site.

Russell Investments is committed to ensuring digital accessibility for people with disabilities. We are continually improving the user experience for everyone, and applying the relevant accessibility standards.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management, L.P., with a significant minority stake held by funds managed by Reverence Capital Partners, L.P. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

© Russell Investments Group, LLC. 1995-2026. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

© Russell Investments

Read more commentaries by Russell Investments