Private Credit Jitters: Spillover into CLO ETFs?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe private credit market’s breakneck growth has hit a significant speed bump. A sharp software selloff, rising redemptions, and transparency concerns in more than $3 trillion market have rattled nerves. This has sparked a vital question: Could cracks in these opaque, illiquid markets spill over into vehicles built on daily liquidity, like CLO ETFs?

Software Sector in the Crosshairs

The primary contagion risk is sector concentration. Software and tech-enabled services represent roughly 15-20% of direct lending portfolios. A meaningful portion of these loans also resides in the Broadly Syndicated Loan (BSL) market – the bedrock of CLO ETFs – leading to a software weighting of 12–18% in typical CLO collateral pools.

iShares Expanded Tech Software Sector ETF (IGV)

Year-to-Date Performance

During the height of the recent “SaaSpocalypse,” the iShares Expanded Tech-Software Sector ETF (IGV) fell 25–30% from its peak. The fund has since recouped nearly 10% of those losses, but the shock still left credit markets unsettled. Even so, many major banks view this as a repricing rather than a systemic reset — more a shift in sentiment than a full-blown credit event. Default rates, for now, remain broadly in line with historical norms.

Flows Reflect Caution, Not Retreat

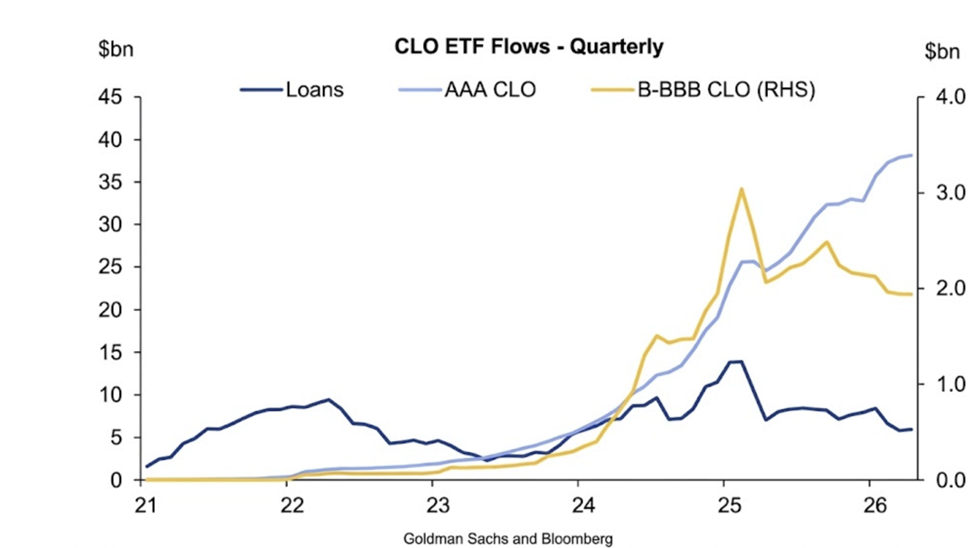

While private credit jitters have surfaced, the flow data reveals a repositioning rather than an exodus. Year-to-date, the CLO ETF category has already attracted over $6 billion in net new capital, underscoring a growing reliance on the wrapper during times of stress.

AAA-rated funds lead the charge, more than offsetting uneven flows in mezzanine tiers. April remains on pace for another $1 billion in total net inflows, signaling that investors are migrating up the quality spectrum rather than exiting the asset class.

Performance: More Dramatic Dispersion

Recent performance also reflects a stark dispersion in credit quality:

- AAA CLOs: Higher-quality tranches have remained relatively resilient – generating positive, single-digit returns with a historical default rate of zero.

- Mezzanine (BBB-B): Trading roughly flat, as income has been offset by a modest widening of spreads.

- Lower-rated tranches: Most sensitive to the private credit scare, with returns ranging from slightly negative to modestly positive.

Industry Insights: Selectivity Over Systemic Risk

John Kim, Co-founder and CEO of Reckoner Capital Management, said the real story isn’t a broad market collapse, but a fundamental repricing of risk. Reckoner recently launched a suite of both AAA-rated and mezzanine CLO ETFs that have all seen positive net inflows so far.

“The current scrutiny of private credit is less about systemic risk and more a focus on certain areas of the market, such as software, that may deliver subpar returns going forward… We have moved into an environment where collateral quality and structural seniority are the primary drivers of performance, rather than market beta,” he said, noting the loans within CLO structures predominantly sit at the top of the capital stack. “The flows we are seeing into CLO ETFs confirm that investors aren’t retreating, but they may be reallocating toward higher-quality structures.”

On the mezzanine side, Danielle Gilbert, Managing Director at Eldridge Capital Management, is also more optimistic than the headlines suggest. She argues that the “built-in” protections of the CLO vehicle are precisely what separate it from the less-regulated private credit space.

“It’s important to distinguish CLOs from the broader private credit story,” Gilbert explained. “CLOs are not immune to these dynamics, but the CLO structure seeks to impose strict rules on what managers can do within the lending box, from sector and issuer concentration limits to rating constraints.”

Gilbert points out that while software concerns are real, active management has already been at work. “Software exposure in CLO portfolios is running below the loan index because CLO managers have been actively underweighting it. We think this is active management doing its job in real time.”

As the manager of the industry’s largest pool of CLO ETF capital, John Kerschner, Global Head of Securitized Products at Janus Henderson, has seen this bifurcation firsthand. Kerschner, who oversees the $27 billion Janus Henderson AAA CLO ETF (JAAA), notes that while the “scare” initially drove a flight to quality, some investors are already hunting for value further down the capital stack.

“We’ve continued to see strong demand for high-quality CLOs,” he noted. “Interestingly, as the noise from the Iran conflict has diminished, we’ve actually seen relatively better demand down the CLO capital stack. Investors are likely looking at the greater amount of widening there and asking where can I get the most bang for my buck when the snap back happens.”

Bottom line: Rather than discouraging participation, the current environment is calling for a more selective approach. After years of chasing yield, 2026 has reset the balance—liquidity is now central to portfolio construction. CLO ETFs provide credit exposure with the flexibility to act when private markets cannot.

Join the Conversation

For a deeper dive on CLO ETFs and the potential ripple effects of private credit, I’ll be joined by Reckoner CEO John Kim at VettaFi’s upcoming Q2 Market Outlook Symposium next Thursday at 11:30 am ET.

Originally published on ETF Trends

For more news, information, and analysis, visit VettaFi | ETF Trends.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All