Monthly Market Update

-

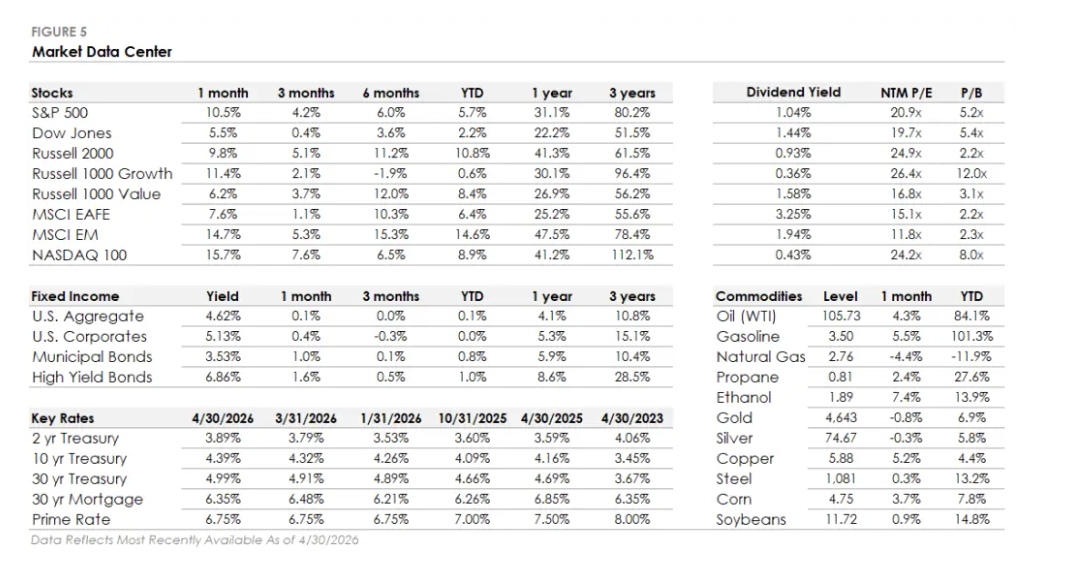

S&P 500 gained 10.5% in April, setting a new all-time high. Communication Services led all sectors, gaining 18.5%, followed by Technology (up 17.5%) and Consumer Discretionary (up 11.7%). Nine of eleven sectors gained, but eight underperformed the index as mega-cap stocks drove the bulk of returns.

-

Bonds pulled back as Treasury yields rose. The U.S. Bond Aggregate returned just 0.1%, with high-yield bonds gaining 1.6% and investment-grade returning 0.4% as credit spreads tightened across the board.

-

Emerging Markets outperformed the S&P 500, gaining 14.7% in what is shaping up to be the best stretch of absolute and relative EM performance in years. Developed Markets rose 7.6% and lagged, with Europe and Japan weighed down by sustained oil supply disruption through the Strait of Hormuz.

-

Small caps rallied: the Russell 2000 gained 9.8% and set a record of its own. The Nasdaq gained nearly 16% for the month, led by a historic semiconductor surge.

-

Consumer confidence fell to a 70-year low in the University of Michigan’s survey (the weakest reading in the survey’s history) even as equities hit new highs.

The Ceasefires Cleared the Worst-Case Scenario, but the Strait is Still Closed

The stock market’s April 206 reversal had a clear catalyst. Back-to-back ceasefires (the U.S.-Iran agreement on April 7 and the Israel-Lebanon ceasefire on April 16) removed the tail risk that had been building since late winter. The S&P 500 erased all of March’s losses and pushed to a new all-time high by month-end. The Dow surged more than 1,300 points on the day the U.S.-Iran deal was announced, its best single session in a year. The Nasdaq gained nearly 16% for the month. Credit spreads, which had been widening steadily through the conflict, reversed three months of deterioration in four weeks, and the VIX fell back to pre-conflict levels.

The complication is that the ceasefires stopped the escalation without resolving the underlying disruption. The Strait of Hormuz, which carries roughly 20% of global oil supply, remains effectively closed. Oil prices fell sharply on the ceasefire announcements (including the largest single-day decline since 2020), then climbed back above $100 per barrel. Gasoline stayed above $4 per gallon throughout April. Consumer confidence falling to a 70-year low reflects this tension: households feel the gap between equity markets at all-time highs and an economy where filling the tank costs meaningfully more than it did six months ago.

The relief was real and the market priced it in quickly. But the structural energy disruption and its knock-on effects on inflation and consumer spending haven’t been priced out yet. In our view, oil staying above $100 with the Strait of Hormuz still closed makes a meaningful consumer spending slowdown in Q2 more likely than the equity market is currently pricing in (See our recent commentary on the Strait of Hormuz: Leads, Lags and the 4:10 to Yuma).

Read more: Leads, Lags and the 4:10 to Yuma

Inside Tech’s 18% Month: Semiconductors Are Winning, Enterprise Software Is Not

Technology gained nearly 18% in April, but the range of outcomes within the sector matters more than the headline. AI is creating a sharp divide between the companies building its infrastructure and the companies it’s starting to replace.

The infrastructure side is winning decisively. Semiconductor stocks rose more than 40% over 17 consecutive trading days (the longest uninterrupted winning streak for the group dating back to the early 1990s). Semiconductor funds absorbed $5.5 billion in new investment during the month, and earnings results from major chipmakers confirmed that infrastructure spending is converting into real revenue growth. The physical backbone of AI (chips, data centers, power, and networking) is seeing demand that outpaces most analyst expectations.

Enterprise software is moving in the opposite direction. Several of the largest names in the industry have declined more than 30% this year, and the selling isn’t stopping even when companies beat earnings estimates and raise guidance. The market is beginning to price in a fundamental question: if AI agents can handle customer service, data entry, workflow management, and internal reporting, what does that mean for software businesses built on per-user-seat pricing? The market hasn’t reached a verdict, but investors are no longer dismissing the question.

We remain broadly constructive on technology over the medium term. But within the sector, semiconductors and AI infrastructure represent the clearer near-term opportunity. Enterprise software deserves more scrutiny until individual companies demonstrate how they’re adapting their business models rather than just absorbing the disruption. (For more on this see our Bloomberg interview on AI disruption in enterprise software)

What Matters Now

April demonstrated that geopolitical relief can move markets faster than most models expect. For investors who had rotated toward defensive sectors or equal-weight exposure during the rotation that started in Q1, that repositioning came at some cost in April’s recovery. The notable exception is emerging markets, which gained 14.7% and outpaced the S&P 500, and this isn’t a one-month fluke. EM is now in the middle of its best run of absolute and relative performance in years, driven by dollar weakness, commodity exposure, and improving fundamentals in several key markets. That’s a trend worth paying attention to, not just a data point to note and move past.

The concentration risk story hasn’t changed. It returned in April just as fast as it left in March, which reinforces the point from Q1: mega-cap leadership is episodic now, not structural.

The more actionable question heading into May is what sustained high oil prices and historically weak consumer confidence mean for corporate earnings. Stocks at all-time highs alongside consumers at a 70-year sentiment low is a gap that tends to resolve in one direction. Q2 reporting season is the first real test, and we will be watching consumer discretionary and retail earnings closely. That’s where the distance between market optimism and household experience will be most visible, and where the next major repricing signal is most likely to emerge.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group