In Q1 2026, I stepped into the role less of an interviewer and more of an investigator, sitting across the table from 35 portfolio management teams covering mutual funds, ETFs, and SMAs in large cap growth, large blend, and large value. Each team was asked the same eight questions — no leading prompts, no room to dodge — so the evidence was clean and comparable. As the answers piled up, patterns began to surface: repeated narratives told by different voices, subtle tells that revealed where conviction was genuine versus rehearsed. Outliers stood out like fingerprints at a crime scene — views that broke from consensus, either by design or by blind spot. By lining up these responses and weighing both what was said and what was left unsaid, I condensed the common themes driving opportunity today, while also flagging the risks lurking beneath crowded assumptions and shared beliefs. What follows is the case file.

AI, Healthcare, and Volatility: Positioning for 2026

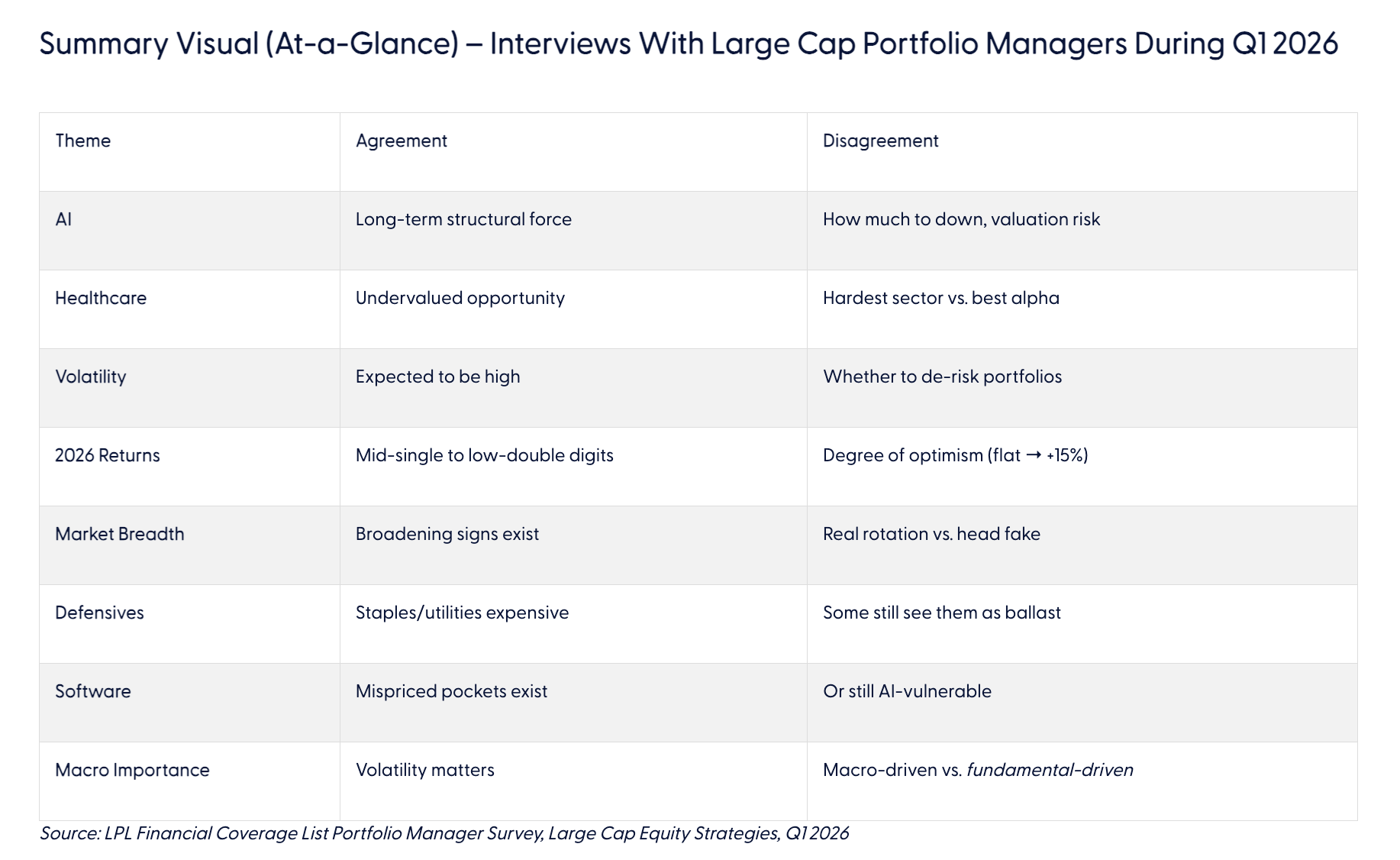

As equity markets transition into 2026, large cap equity portfolio managers share a surprisingly consistent framework — paired with sharp disagreements on where risk and opportunity sit. A survey of large growth, value, and blend managers reveals a market shifting away from simple narratives toward selectivity, fundamentals, and manager skill.

At the center of this discussion sits artificial intelligence. Nearly every manager acknowledges AI as a long‑term structural force, yet far fewer believe it remains an easy trade. At the same time, healthcare has emerged as the most consistently cited undervalued sector across investment styles, even as managers concede it remains one of the hardest areas to execute well.

What follows is a synthesis of where managers align, where tension exists, and what these dynamics suggest for equity markets heading into 2026.

AI: A Structural Force That No Longer Guarantees Returns

AI dominates nearly every strategic conversation. Managers broadly agree it represents a multi‑year earnings driver spanning software, semiconductors, industrial automation, data infrastructure, and services. The difference now lies in execution.

The earlier phase of AI investing rewarded broad exposure. We believe that phase has largely passed. Managers increasingly emphasize real earnings, sustainable demand, customer monetization, and the durability of competitive advantage. Several indicate that portions of the AI infrastructure, semiconductors, and enabling hardware have high valuations, leaving a limited margin for error.

This shift has created three emerging camps:

-

AI beneficiaries with recurring revenue and pricing power

-

AI survivors capable of absorbing competition and margin pressure

-

Mispriced AI losers where fear has outpaced fundamental deterioration

The tension centers on portfolio sizing. Some managers remain heavily allocated, treating AI as the next secular growth engine. Others deliberately neutralize exposure, framing AI as one of the largest potential sources of downside if expectations compress.

The implication is not AI fatigue, but higher hurdles. Exposure alone no longer drives results — security selection does.

Read more: AI Wave Continues to Power Technology Earnings Boom

Healthcare: Broad Opportunity, Narrow Margins for Error

Across styles and mandates, healthcare stands out as the most consistently cited undervalued opportunity. Managers describe the sector as under‑owned, poorly understood, and discounted relative to earnings potential.

Key drivers include:

- Aging demographics

- Innovation across biotechnology and medical devices

- Increased M&A discipline within pharmaceuticals and services

Despite this optimism, healthcare simultaneously earns a reputation as one of the hardest sectors to win consistently. Regulatory scrutiny, binary outcomes in innovation, pricing risk, and complex reimbursement structures demand deep fundamental analysis.

Some managers cite healthcare as their best alpha‑producing sector, while others describe it as chronically frustrating. The divergence suggests healthcare may reward skilled managers, while punishing surface‑level exposure.

Market Breadth: Opportunity, With Conditions

Many managers report early signs of market broadening beyond mega‑cap technology leadership. Industrials tied to power infrastructure, aerospace, automation, and select consumer discretionary areas receive increased attention. Software segments that suffered during peak AI enthusiasm also appear on opportunity lists.

That said, conviction remains uneven. Several managers caution that leadership rotation has been episodic and fragile. Rapid reversals and crowded positioning continue to dominate trading patterns.

The prevailing takeaway is conditional optimism: new opportunities exist, but require patience and acceptance of volatility. Sustainable broadening remains unproven.

Volatility Without Capitulation

A rare consensus exists around volatility expectations. Managers broadly anticipate heightened market swings driven by geopolitics, policy uncertainty, valuation dispersion, and narrative shifts.

Yet despite this expectation, very few portfolios have moved outright defensive. Traditional risk‑off behavior, rotating heavily into low‑beta sectors, appears limited.

Instead, managers redefine defense through:

- Earnings durability

- Balance sheet strength

- Cash flow consistency

- Quality of business models

Volatility is treated less as a signal to retreat and more as a condition to navigate.

Traditional Defensives Face New Scrutiny

Historically defensive sectors such as staples and utilities received widespread skepticism. Multiple managers describe these areas as crowded, expensive, and vulnerable if leadership rotates or yields move.

High‑quality compounders, once perceived as capital‑preservation vehicles, also attract valuation concerns. In several cases, managers argue these stocks now carry asymmetrical downside due to stretched expectations.

A minority still view traditional defensives as stabilizers, particularly in uncertain macro environments, but this is no longer the dominant stance.

Software: Opportunity or Structural Risk?

Software divides opinion as sharply as AI itself.

One group argues that broad selling pressure has created mispriced opportunities. In this framework, fears of AI‑driven disruption overshot reality, and select companies retain strong customer relationships, sticky revenue, and pricing power.

Others maintain deep caution. They cite risks of commoditization, new competitive entrants, and overestimated addressable markets.

Software increasingly behaves less like a monolith and more like a case by case exercise — forcing differentiation rather than blanket exposure.

2026 Equity Return Expectations: Moderation Reigns

Despite differences in narrative emphasis, most managers converge on a moderate return outlook for 2026.

Typical expectations cluster in the mid-single to low double digits, with returns driven primarily by earnings growth rather than valuation expansion. A minority project flat outcomes, while a smaller bullish group targets double‑digit results.

The common denominator is realism. Few expect a repeat of momentum‑driven expansions. Discipline, patience, and earnings delivery dominate expectations.

Stock Picker’s Market or Macro Market?

A final tension cuts across all discussions: the weight of macro versus fundamentals.

Growth‑oriented managers emphasize bottom‑up execution, arguing company‑specific outcomes will matter more than interest rates or policy headlines. Several value‑oriented perspectives lean more heavily on geopolitical risk, tariffs, and policy volatility.

This divide influences portfolio construction and risk tolerance, shaping positioning more than any single sector call.

What This Means for Allocators

The survey suggests a market where manager differentiation matters more than style labels.

Consensus exists around structural forces, earnings discipline, and volatility. Disagreement centers on positioning, sizing, and conviction. The absence of universally “safe” sectors reinforces the importance of process, skill, and risk awareness.

As markets move into 2026, success may depend not on buying the right theme but on navigating the tensions within it.

Summary Tension Map

Methodology: Identifying Key Risks and Opportunities

To identify the most prominent risks and opportunity sets across our firm’s internal Coverage List, we conducted structured interviews with 35 portfolio management teams spanning mutual funds, ETFs, and SMAs. Each team was asked the same eight survey questions, ensuring consistency of inputs and comparability across strategies, vehicles, and investment styles.

Responses were first reviewed and normalized to account for differences in terminology and communication styles. Qualitative answers were then coded into thematic categories, allowing us to assess areas of convergence and divergence across managers. Themes that appeared repeatedly across multiple teams, particularly when supported by strong convictions or detailed rationale, were categorized as common views. Conversely, perspectives that meaningfully deviated from the broader sample, either in direction, magnitude, or underlying assumptions, were flagged as outliers.

To differentiate risks from opportunities, each theme was evaluated through a forward‑looking lens, considering how widely held assumptions, positioning, or macro and fundamental dependencies could influence future outcomes. Particular attention was paid to areas where consensus appeared strong but underlying conditions could change, as these scenarios may introduce asymmetric risk. Similarly, underappreciated or less crowded views — especially those supported by clear catalysts or structural trends — were evaluated as potential sources of opportunity.

This process resulted in a consolidated framework that reflects not only what portfolio managers are collectively emphasizing today, but also where expectations may be stretched, narratives overly aligned, or convictions unevenly distributed. This report summarizes the key insights derived from this analysis, organized around the eight survey questions.

Scott is the leader of the equity product research team and covers U.S. large cap equity managers, derivative income managers, and is a key contributor to the LPL Research centrally managed portfolios.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1097066

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial