U.S. Inflation Measures Tell Two Different Stories

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSomething unusual is happening with U.S. inflation data. While the core Consumer Price Index (CPI) has looked relatively cool recently, core Personal Consumption Expenditures (PCE) inflation has risen sharply.

The incremental widening between the two inflation measures has accelerated meaningfully over the past few months, largely driven by the rapid adoption and buildout of AI in the U.S. economy. Even without the risks introduced by the Iran conflict, the evolving trends in the inflation data would have complicated the outlook for Federal Reserve rate cuts.

Read more: Making Sense of a Cross-Asset Disconnect

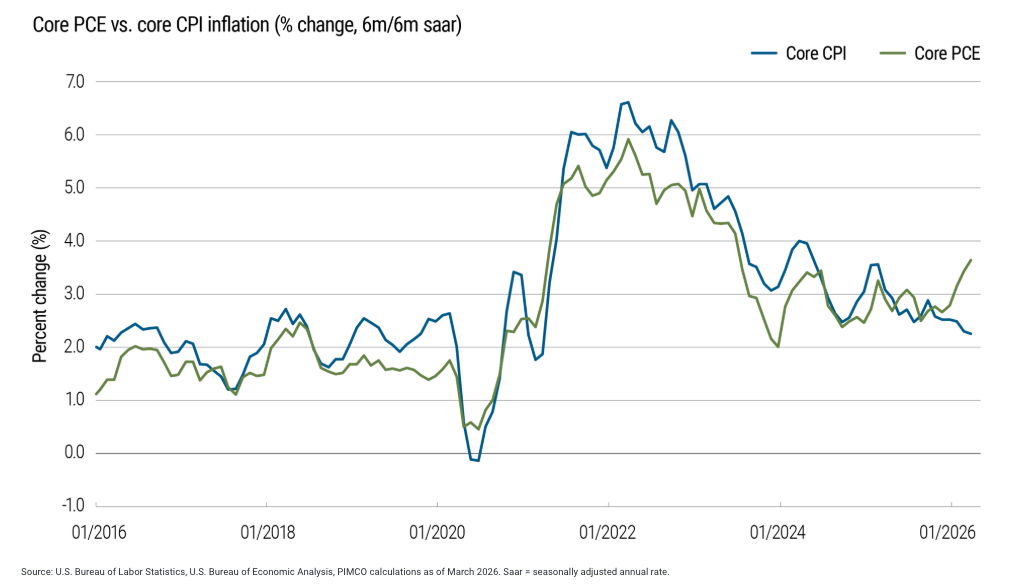

The three-month annualized pace of core PCE surged from 2.4% in November 2025 to 4.1% in February 2026. The gap between PCE and CPI year-over-year has flipped from a historically negative 30–40 basis points to positive 60 basis points – one of the largest reversals since 1985. Smoothing the data over six months still shows a significant and widening wedge between the two measures (see Figure 1).

Figure 1: Key measures of core U.S. inflation have diverged notably since late 2025

This divergence, and the factors driving it, are important because they highlight inflationary forces that aren’t fully reflected in CPI – and therefore aren’t fully visible to households, businesses, and policymakers, even though CPI numbers make headlines every month.

In particular, it appears that tariff-related cost pressures weren’t the only driver of persistent inflation in recent months. Indeed, massive demand for semiconductors, memory capacity, and other components of the AI infrastructure buildout seems to be spilling over into consumer prices, with tech products and services playing an outsize role. The energy shock, which will likely affect the cost and the availability of these components, adds a new layer of uncertainty. AI demand and energy scarcity appear to be combining to create problematic inflation in semiconductors and related components, which in turn will affect prices of related consumer goods.

To paraphrase a common saying, what you can’t measure, you can’t manage. Having two key inflation readings telling different stories complicates critical decisions for households, businesses, and policymakers. Understanding what’s driving the difference between CPI and PCE could provide some clarity even as the divergence raises new questions – especially for the U.S. Federal Reserve, whose monetary policy decisions are driven in part by a mandate to stabilize prices. The Fed has historically viewed the PCE index as its preferred inflation measure.

What generally drives the difference

Taking a step back, in the U.S., there are two primary measures of the prices consumers pay for goods and services. The Consumer Price Index (CPI), published by the Bureau of Labor Statistics, measures out-of-pocket expenses paid directly by urban households. The Personal Consumption Expenditures (PCE) price index, published by the Bureau of Economic Analysis, includes those household out-of-pocket expenses plus expenses paid on behalf of households by government programs (e.g., Medicare, Medicaid), employers, and others. Within each measure, the “core” gauge excludes volatile food and energy prices, while the “headline” gauge includes them.

Much of the source data for the PCE index comes from the CPI survey, which is why the two indices tend to move together much of the time. However, important differences in methodology can lead to periods of significant divergence, as we see today. Three specific factors help explain the gap:

- Formula differences: PCE uses a Fisher-Ideal chain-weighted formula that accounts for substitution effects (i.e., when consumers facing rising prices switch to less expensive alternatives). CPI uses a modified Laspeyres index that appears to overstate inflation in categories where consumers can substitute away.

- Consumption weights: CPI weights are updated once a year based on a consumer expenditure survey; PCE weights adjust in real time and are derived from national income accounts. And the weightings can vary significantly. Currently, shelter carries a much larger weight in CPI (around 34%) than in PCE (around 16%), while healthcare, financial services, and information and communication products and services carry larger weights in PCE.

- Net scope: PCE includes spending on behalf of consumers – for instance, employer-paid healthcare and government-funded medical services – that CPI excludes entirely. It also captures estimates of financial services costs, such as portfolio management fees, which are measured differently or omitted from CPI.

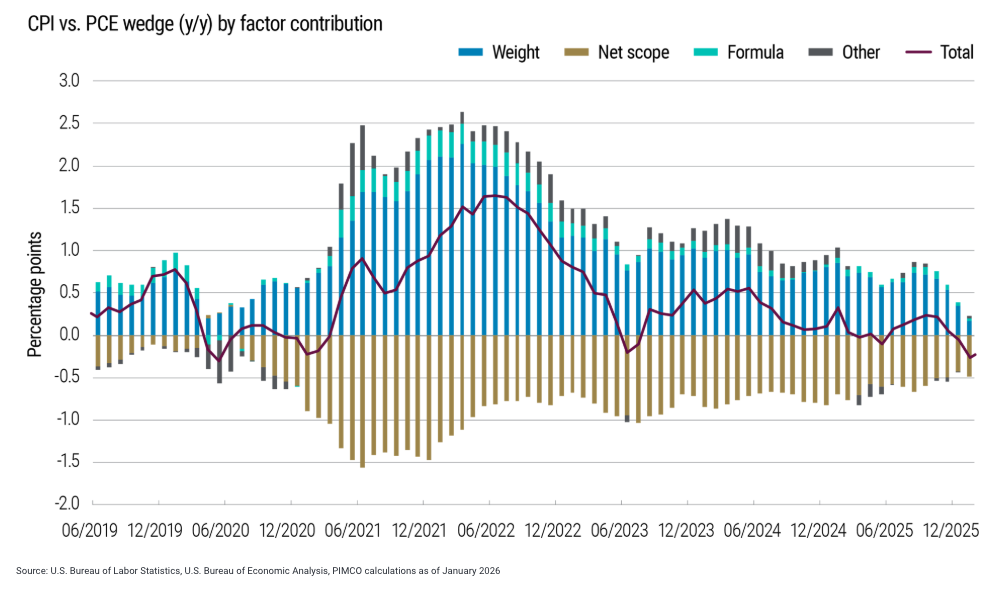

Figure 2 shows the recent contribution of each factor to changes in the “wedge” between CPI and PCE inflation.

Figure 2: Three main factors contribute to the gap between CPI and PCE

The Fed has long preferred the PCE index’s broader scope and more dynamic weighting as it provides a more comprehensive picture of the price pressures facing households and businesses. However, when the categories driving PCE higher are out of scope or underweighted in CPI, then the CPI numbers that dominate headlines – and drive the cash flows of inflation-indexed bonds – can paint a misleadingly benign picture.

What’s behind the current divergence

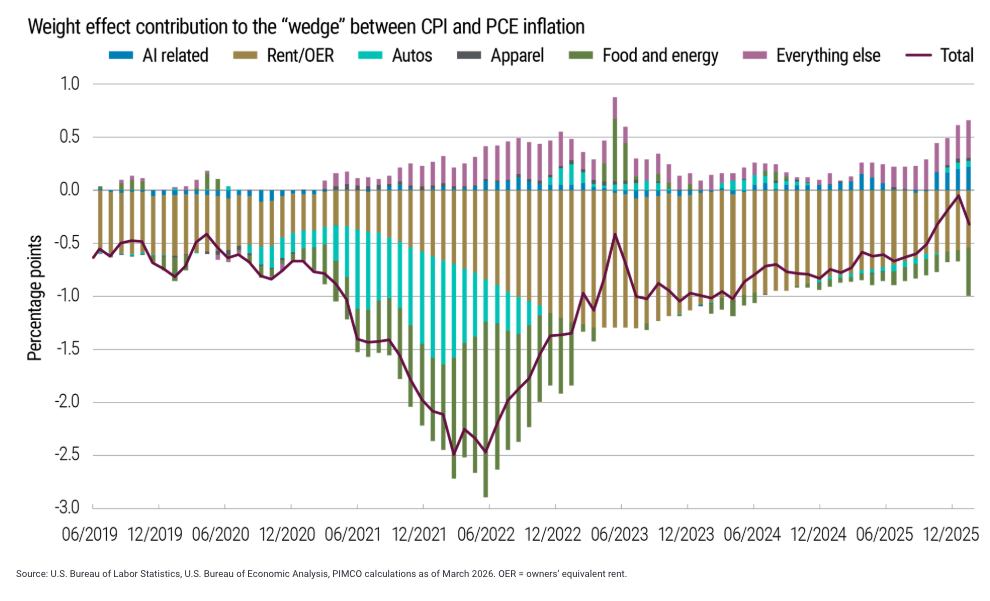

The “weight” factor is driving much of the current CPI/PCE wedge. Cost pressures related to technology (especially AI), tariffs, and some services categories are concentrated in areas with larger weights in the PCE basket (see Figure 3).

Figure 3: Different weights among sectors in the CPI and PCE baskets contribute to the gap

Accelerating technology-related inflation accounts for a meaningful portion of the recent divergence. Prices for information processing equipment – specifically gaming hardware, memory products, and computer software and accessories – have risen sharply over the past several months. AI is driving accelerating demand for chips, memory, and servers, which is spilling over into consumer product prices. Prices of imported computers and related components have surged recently, as have producer price measures along supply chains across Asia, pointing to further price increases to come.

Another contributor is the seasonal price reset in streaming services, cellphone services, and other services categories. Larger-than-usual price jumps earlier this year were concentrated in categories with larger weights in the PCE basket. Significant price adjustments in tech components and the expectation that input costs will keep rising due to the AI-related buildout could also be spilling over into consumer prices of streaming and cellphone services.

Tariff pass-through is also playing a role. Evidence suggests that tariffs have led to price increases and higher inflation in core goods.1 However, the tariff pass-through has been uneven across categories. Until recently, apparel and autos – two large categories in both indexes – showed little observable pass-through. That changed in early 2026, at least for apparel, with notable price acceleration in jewelry and women’s clothing.

Energy, AI, and possible chip shortages

What is signal versus noise? The most concerning driver of the CPI/PCE wedge (in which PCE inflation keeps ticking higher while CPI remains subdued) is the acceleration in price inflation for microchips and related products. AI-driven demand is colliding with an Iran-related supply shock, creating a compounding price dynamic that is only beginning to show up in the data.

AI-related investment has been the primary driver of overall U.S. investment spending over the past year, and investment plans from large AI hyperscalers have been upwardly revised in 2026 from an already breakneck pace. Even before the U.S.–Iran conflict began in February, strong demand for technology equipment sourced from Asian supply chains was pushing up the prices of these key components. Because these categories carry meaningfully larger weights in PCE than in CPI, the resulting pressure shows up more forcefully in the Fed’s preferred inflation gauge.

The Iran conflict is likely to compound these price effects. Chip fabrication is highly energy-intensive, and energy prices will likely continue rising as long as the turmoil around the Strait of Hormuz constrains shipping while stockpiles dwindle. Also, helium is an irreplaceable input when creating chips, and spot helium prices have doubled due to Middle East supply disruptions. Some major Asian chipmakers report their helium stockpiles may last only about six months.

This combination – strong, structurally driven demand and fragile, energy-sensitive supply chains – raises the risk that chip-related inflation becomes more persistent rather than fading quickly.

Labor markets and wages

A key question for the inflation outlook is whether these supply-side price shocks remain confined to specific categories or become the precondition for more persistent inflation pressures, which is what happened in 2022. The good news is that today’s U.S. labor market is not as tight as it was in 2021–2022. The large fiscal transfers (e.g., stimulus programs for households and businesses) and extremely tight labor conditions that amplified second-round effects after the pandemic are not present today. Indeed, labor markets today don’t appear to be a source of significant inflationary pressures. (For details, see our latest Cyclical Outlook, “Layered Uncertainty: Conflict, Credit Stress, and AI.”)

However, central banks will want to be mindful of how short-run inflation expectations can be a transmission mechanism from prices to wages. Even in a labor market that isn’t overheated, sustained increases in the prices workers and consumers see at the grocery store, at the pump, and on their devices can push short-run inflation expectations higher. Those expectations could feed into near-term wage negotiations and catch-up dynamics.

Bottom line for the Fed

All of this puts the Fed in a difficult position. The CPI/PCE divergence highlights the growing inflationary pressures tied to AI investment, chip demand, and energy-sensitive supply chains – forces that are likely structural, not transitory. If the Iran conflict persists, the pass-through to chip prices and broader goods inflation could widen the wedge further, keeping the Fed’s preferred gauge elevated even as both CPI and PCE reflect higher energy costs that are passed on to consumers across a wider array of consumer products.

At the same time, a prolonged energy disruption poses clear downside risks to global growth. Higher energy costs act as a tax on consumers and non-energy businesses worldwide, and history suggests that sustained oil price shocks of this magnitude – particularly when combined with supply chain bottlenecks – raise recession risks.

Faster AI implementation will also have offsetting effects over time. Inflationary pressures associated with stronger demand from the race to build AI infrastructure could be offset by higher productivity and moderating labor costs.

Taken together, the outlooks for inflation and growth leave the Fed facing an increasingly uncomfortable stagflationary situation. We believe the bar for rate hikes is incredibly high. However, uncomfortably hot core inflation, even if it is temporary, makes rate cuts difficult as well.

Our base case remains that the Fed’s next move is a cut, amid a stagflationary shock that raises the risk of global recession and higher unemployment. But the timing has become more uncertain.

Footnotes:

1Robert Minton, Madeleine Ray, and Mariano Somale, “Detecting Tariff Effects on Consumer Prices in Real Time – Part II.” Federal Reserve FEDS Notes (April 2026)

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosures

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author] and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits