Key Takeaways

-

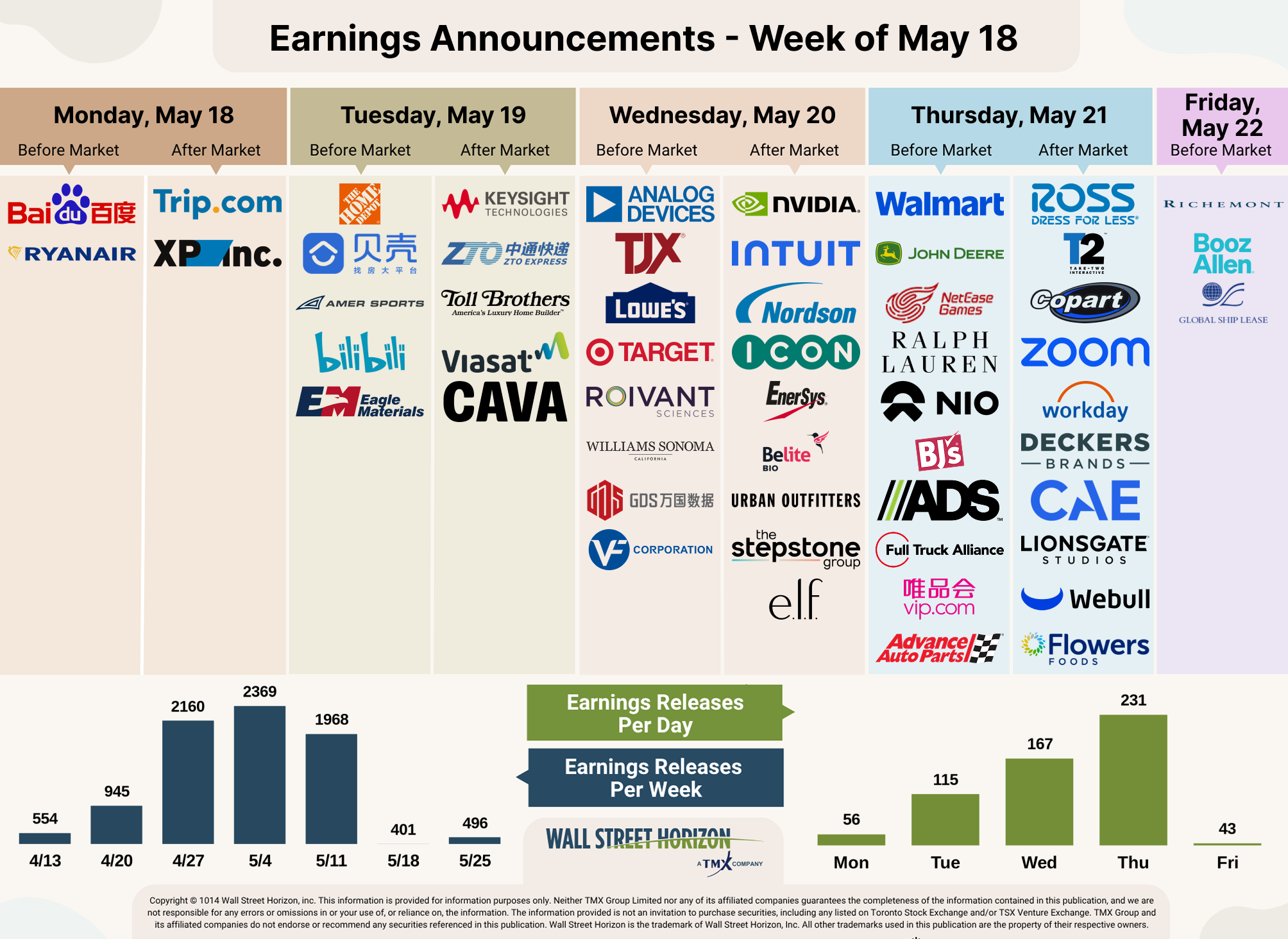

Earnings slow down from this point forward, with only 611 global companies releasing results for Q1 this week

-

All eyes will be on the retail earnings (WMT, TGT, HD, LOW, TJX, ROST) and Nvidia results

-

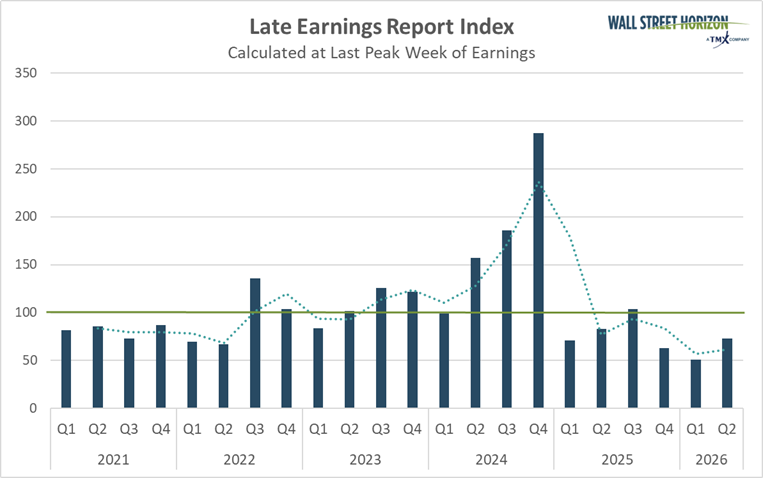

Corporate uncertainty reaches its highest level in three quarters after a record low in Q1

-

Potential earnings surprises this week: Hasbro (HAS), WalMart (WMT), Ulta Beauty (ULTA), Palo Alto Networks, Medtronic (MDT), Intuit (INTU) and Accenture (ACN)

The Breaking Point? April’s Energy Spike Erodes Purchasing Power

Last week, macro data revealed a US consumer that continues to be pinched. April CPI rose 3.7% YoY, marking a nearly three-year high,1 while PPI surged 6.0% YoY2, largely driven by an energy shock that has kept retail gasoline above $4.50 a gallon and crude prices stuck north of $100 a barrel.

This sting at the pump directly eroded consumer spending power, as April Retail Sales slowed to 0.5%, below expectations for 0.6% and down from March’s 1.6%. This has raised fears among economists that the consumer has reached a breaking point and that stagflationary pressures are threatening a soft landing.3 Because core inflation remains so sticky, the Federal Reserve is now widely expected to keep interest rates at current levels for longer. According to the CME Group’s FedWatch tool, there is now a greater probability of a rate hike at the December meeting than there is a rate cut.4

Next Week’s Watchlist: The Retail Earnings Parade and the AI Infrastructure Play

Against this challenging macro backdrop, a stark divergence is expected as major retailers report earnings next week. Discounters are projected to perform well, with Walmart (WMT) expected to outpace Target (TGT) by gaining market share from high-income households trading down for groceries, while Target remains more vulnerable due to its heavier mix of discretionary goods.

Meanwhile, home improvement giants Home Depot (HD) and Lowe’s (LOW) continue to battle a frozen housing market weighed down by high mortgage rates, leaving them reliant on spring seasonality and "pro" contractor sales to stabilize revenue. Conversely, off-price darlings TJX Companies (TJX) and Ross Stores (ROST) remain the bright spots of this high-inflation environment as shoppers hunt for bargains.

The high-stakes AI infrastructure trade hits a critical juncture next week as market bellwether Nvidia (NVDA) reports earnings, just as rival chipmaker Cerebra hits Nasdaq last week in the one of the biggest tech IPOs since Uber in 2019. Ahead of Nvidia's report, the bar is set exceptionally high following strong earnings from peers like Broadcom and Marvell, with investors hunting for a massive forward revenue guide now that Blackwell NVL72 supercomputers are in full-scale production. All eyes will be on data center revenue which hit a record of $62.3B last quarter and advanced 75% YoY driven by AI chip demand from hyperscalers.

Read more: Mid-Quarter Investor Conference Calendar: New Leaders, Same Trends, Big Profits

Looking to challenge this dominance, Cerebras made its public debut on Thursday, opening at $350 after selling shares at $185, well above the company’s expected range. That values the chipmaker at over $100B.5 While Cerebras has built its reputation on dedicated, wafer-scale chips optimized for real-time AI inference, competition is heating up fast as Nvidia counters by folding Groq inference tech into its upcoming Rubin chips.

Including the 11 S&P 500® companies that reported last week, EPS growth stands at 27.7% for Q1 2026, unchanged from the prior week. This is on target to be the highest quarterly earnings growth rate for the index in a little over four years (Q4 2021 reported 32% growth). Revenue growth currently stands at 11.4%, up from 11.3% in the prior week. This could be the highest revenue growth rate since Q2 2022.6

Source: Wall Street Horizon

Corporate Confidence Still Strong but Lower than Recent Quarters

The Late Earnings Report Index, our proprietary measure of CEO uncertainty, recorded its highest post-peak earnings season number in three quarters, but still below the long-run benchmark.

The LERI tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, and anything above that indicates that companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests that companies feel they have a pretty good handle on the near-term.

The official post-peak season LERI reading for Q2 stands at 73, below the baseline reading, but higher than the 53 posted in Q1 and 63 posted in Q4. This suggests companies are feeling slightly less certain about economic conditions than they were in Q4 2025 and Q1 2026, perhaps spurred by the black swan event of the Iran War which began in late February. As of May 12, there were 91 late outliers and 113 early outliers.

Source: Wall Street Horizon

Potential Surprises Through the End of the Q1 Season

Academic research shows that when a company confirms a quarterly earnings date that is later than when they have historically reported, it’s typically a sign that the company will share bad news on their upcoming call, while moving a release date earlier suggests the opposite.7

In the last few weeks of the first quarter earnings season we get results from a number of large companies on major indexes that have pushed their Q1 2026 earnings dates outside of their historical norms. Seven companies within the S&P 500 confirmed outlier earnings dates through June 18. Hasbro (HAS), WalMart (WMT), Ulta Beauty (ULTA), Palo Alto Networks (PANW) and Medtronic (MDT) are later than usual and therefore have negative DateBreaks Factors.* Meanwhile Intuit (INTU) and Accenture (ACN) are reporting earlier than usual.

* Wall Street Horizon DateBreaks Factor: statistical measurement of how an earnings date (confirmed or revised) compares to the reporting company's 5-year trend for the same quarter. Negative means the earnings date is confirmed to be later than historical average while Positive is earlier.

Q1 2026 Earnings Wave

With peak earnings season officially in the rearview mirror, fewer companies will release this report this week. In our universe of 11,000 global companies, only 611 will report Q1 2026 results. Thus far, 94% of companies have confirmed their earnings date and 82% have reported.

Source: Wall Street Horizon

The Bottom Line

While the S&P 500 is pacing toward its strongest earnings growth in four years, a rising LERI reading suggests that energy shocks and higher-for-longer rates may be denting corporate confidence. Upcoming retail earnings will reveal if the consumer has officially hit a breaking point, while Nvidia’s results and Cerebras’ explosive debut will test whether the AI boom can continue to carry a market increasingly threatened by stagflation. Robust fundamentals are currently holding the line, but the headwinds that could prevent a soft landing through 2026 are beginning to mount.

1 CONSUMER PRICE INDEX – APRIL 2026, Bureau of Labor Statistics, May 12, 2026, https://www.bls.gov

2 PRODUCER PRICE INDEXES – APRIL 2026, Bureau of Labor Statistics, May 13, 2026, https://www.bls.gov

3 Advance Monthly Sales for Retail and Food Services, US Census Bureau, May 14, 2026, https://www.census.gov

4 CME Group FedWatch, https://www.cmegroup.com

5 “Cerebras Stock Jumps 68% After Blockbuster IPO. CEO Sees Bigger Things Ahead.” Barron’s, Adam Levine, May 14, 2026, https://www.barrons.com

6 FactSet Earnings Insight, John Butters, May 15, 2026, https://advantage.factset.com

7 Time Will Tell: Information in the Timing of Scheduled Earnings News, Journal of Financial and Quantitative Analysis, Eric C. So, Travis L. Johnson, Dec, 2018, https://papers.ssrn.com

Copyright © 2026 Wall Street Horizon, Inc. All rights reserved. Do not copy, distribute, sell or modify this document without Wall Street Horizon's prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities, including any listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. This publication shall not constitute an offer to sell or the solicitation of an offer to buy, nor may there be any sale of any securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, and TSX Venture Exchange are the trademarks of TSX Inc. and are used under license. Wall Street Horizon is the trademark of Wall Street Horizon, Inc. All other trademarks used in this publication are the property of their respective owners.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Wall Street Horizon

Read more commentaries by Wall Street Horizon