In the first few days of June, we are seeing a bit of a consolidation in markets after a blistering two-month run in all things tech and semiconductor related.

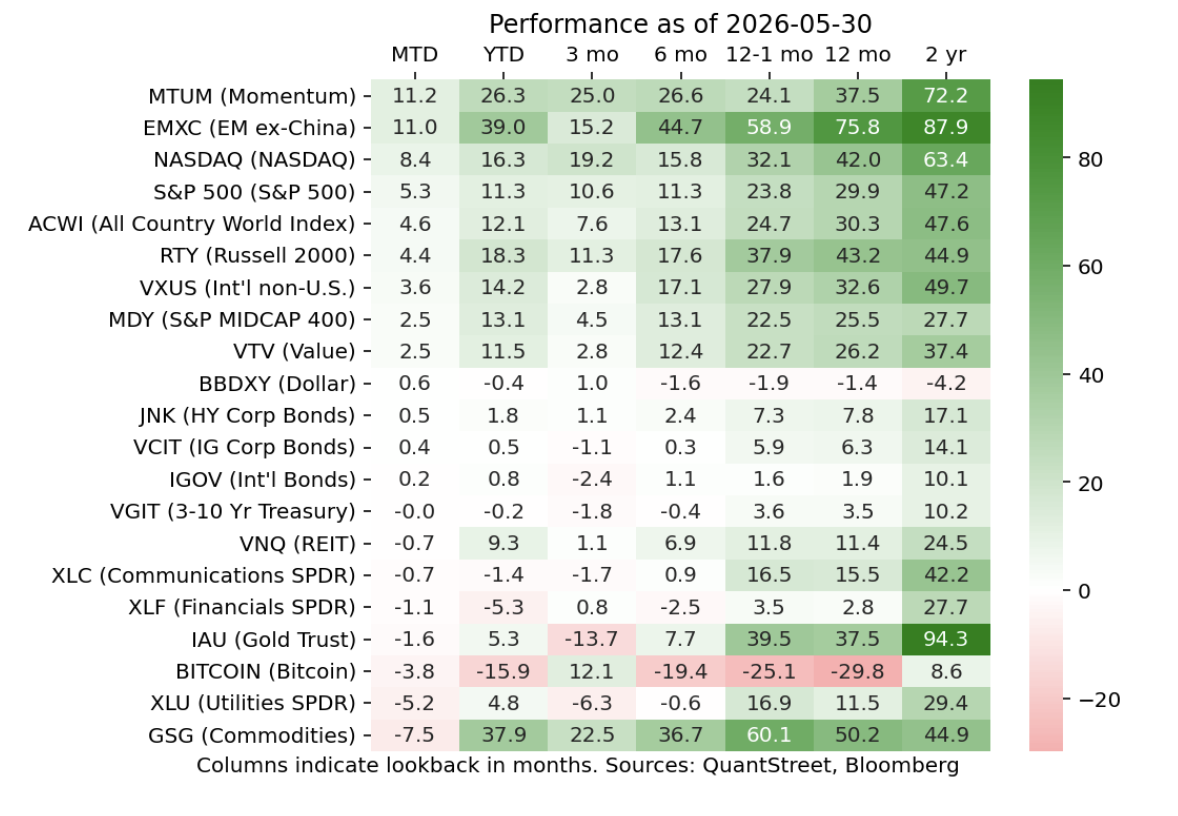

The above table shows just how far the AI trade has gone across different segments of global markets. Nasdaq was up 8.4% in May, which was on top of its 15.3% return in April. In dollar terms, Taiwan’s and Korea’s stock markets are up an almost unimaginable 106% and 220% over the last year. And many believe these run-ups are justified based on an insatiable global demand for processor and memory chips. While Taiwan’s forward price-to-earnings (PE) ratio has risen (but only to just under 17x according to Bloomberg), Korea’s forward PE multiple actually contracted over the last year (and now sits at around 7x). Ergo, prices went up, but earnings expectations went up more.

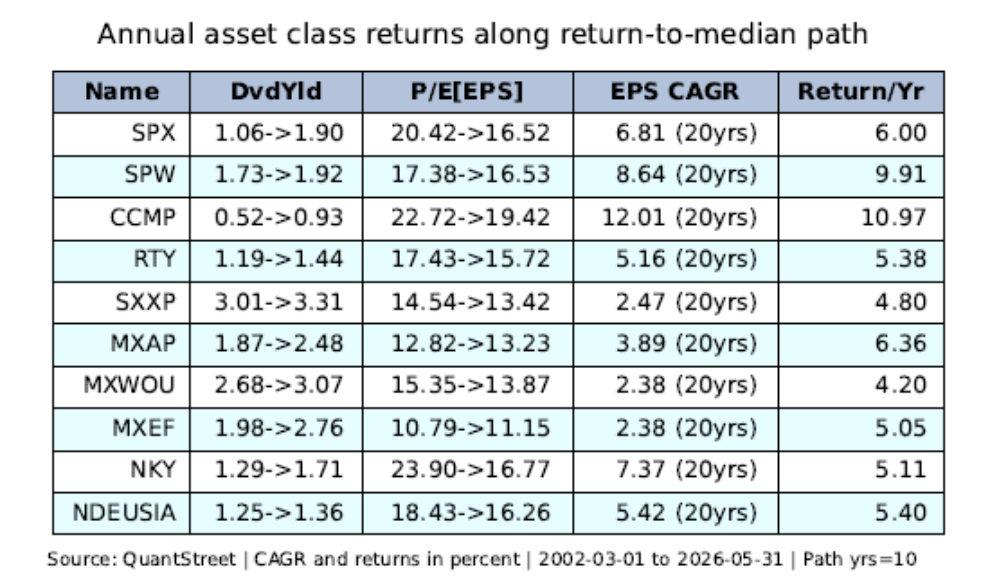

Based on our reversion-to-the-long-run analysis (see original Substack post), despite the lofty current valuations, the S&P 500 (SPX) is slated to return 6% per year over the next decade, which is ahead of the 4.8% forecast for European stocks (SXXP) and the 4.2% forecast for international stocks ex-US (MXWOU). Based on our methodology, if the market believes S&P 500 earnings growth will run at 9-10% over the next decade (analysts are forecasting earnings growth in the mid-teens for the year ahead) and forward PEs contract to 19-20 (as opposed to 16.5), then the S&P 500 could generate annual returns in the 10% range over the coming decade. (Keep in mind, these are all just back-of-the-envelope forecasts of broad market indices and future returns could be much worse.)

To believe stocks globally will earn even high-single digit returns in the coming decade, you would need to believe that this decade will be characterized by very robust earnings growth. We happen to believe this will be the case. But, of course, only time will tell.

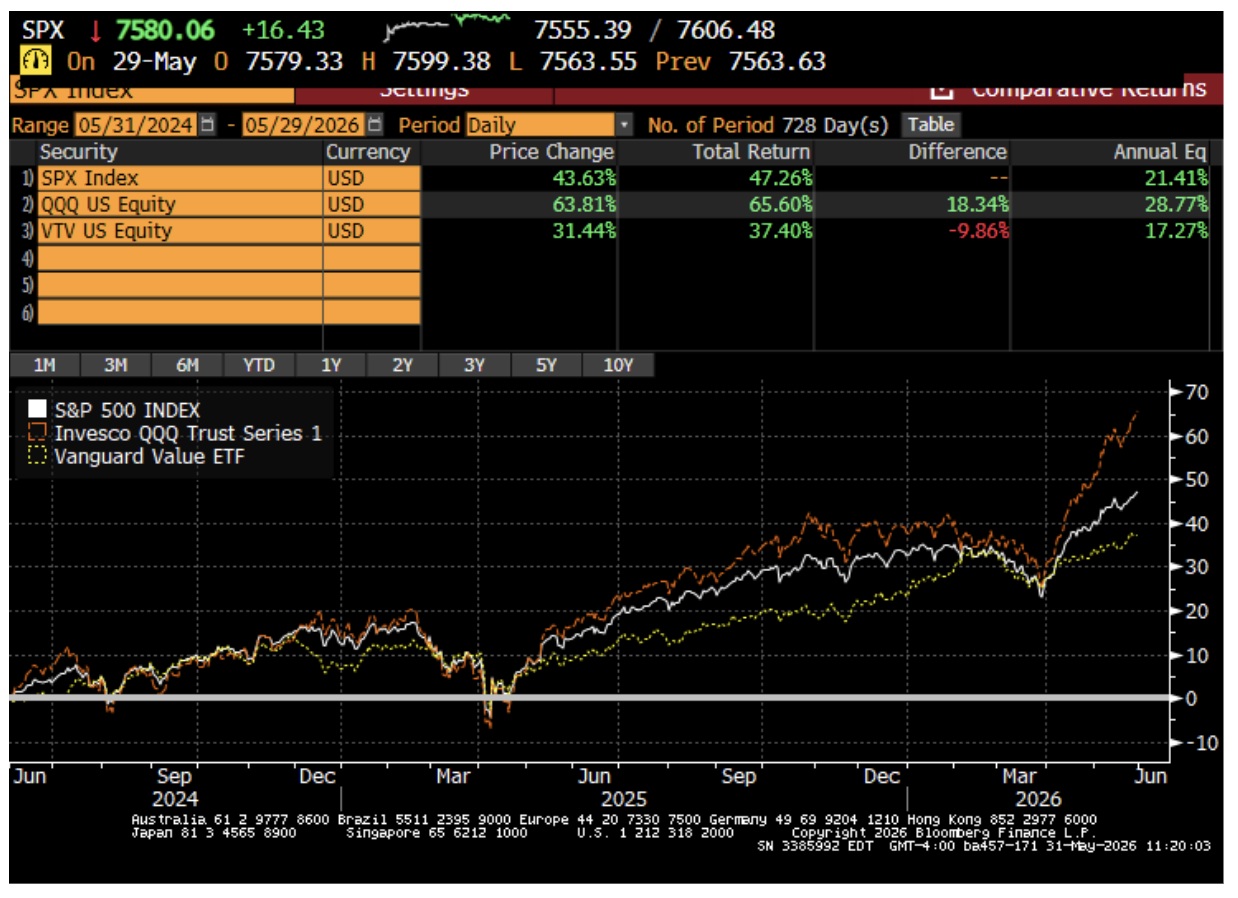

This month, our portfolio process suggests an increased allocation to value stocks, which we implement using Vanguard’s VTV ETF. (Why VTV? Because we see it as the best-in-class value exposure given its liquidity and expense ratio. If anyone has other thoughts about a more liquid and cost-effective way to gain value exposure, we’d love to hear from you.) To get a sense of what you get in VTV, the table below shows the largest single name exposures in the ETF’s stock basket. There are lots of banks, industrials, energy, and consumer companies. Not that any company is unaffected by AI (e.g., JPMorgan, the top name in the index, has invested very heavily in its AI infrastructure), but these are “old economy” companies and, notably, are not the Mag 7 + SpaceX and its ilk that have driven the market higher over the last few years.

Also notable is that VTV is less volatile than its S&P 500 and Nasdaq cousins. It hasn’t run up as much as they have (see next chart), but also has had a smoother return series and our machine learning forecasting model is quite sanguine on value’s prospects at the moment, especially relative to its somewhat grumpy outlook on the Nasdaq. (Another disclaimer: The model changes its mind rather often and quickly, so this assessment may change over the next few weeks. The model’s views may be wrong and should not be interpreted as a guarantee of future performance.)

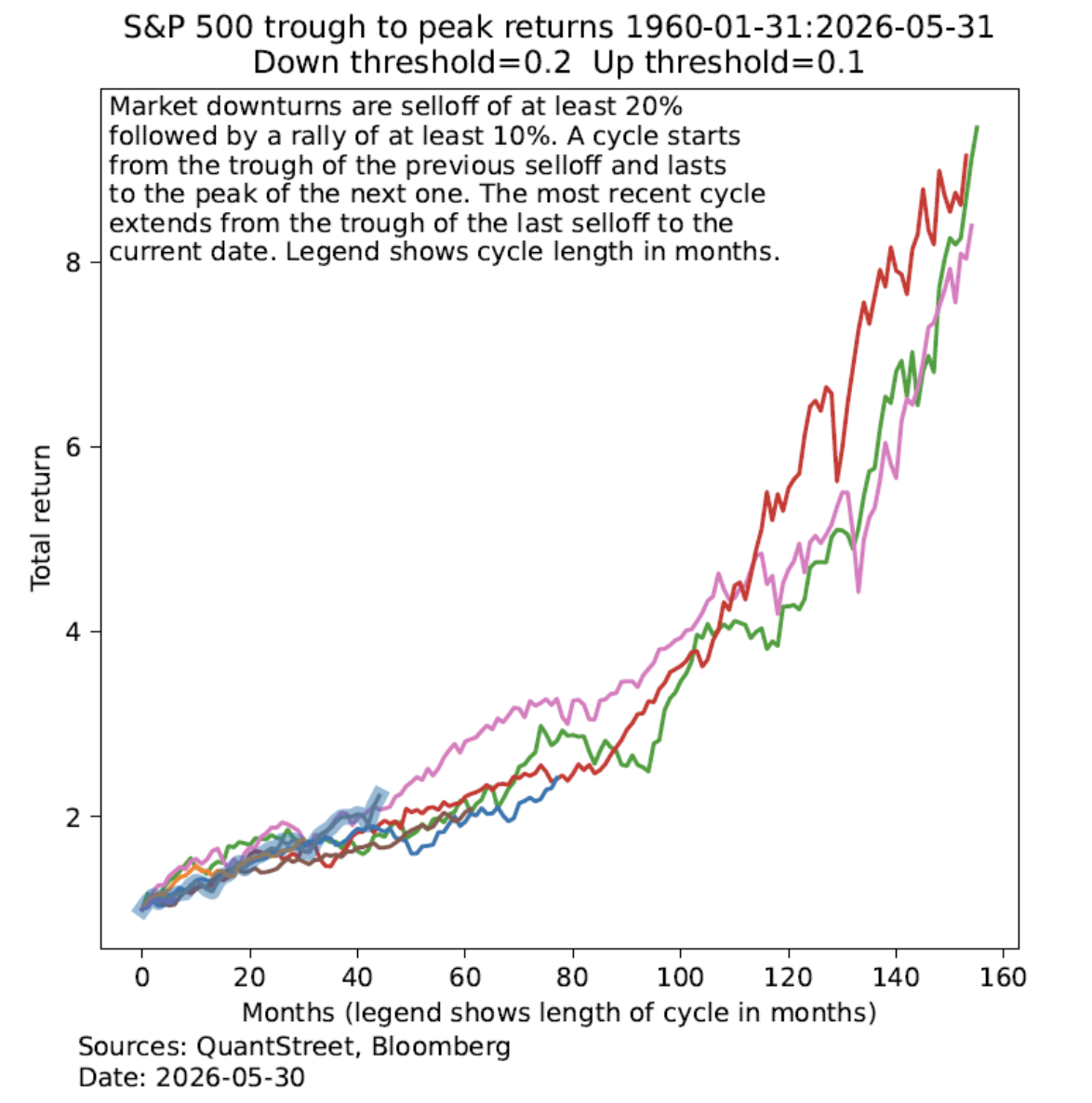

Finally on the subject of short-termism in markets, the next chart shows how the current bull run lines up with past bull cycles in the market. We define a bull run as starting from a local market trough followed by a subsequent market appreciation without ever suffering a drawdown of more than 20% (using month-end prices). Based on this metric, we are now in month 45 of the most recent bull market (shaded line in chart). Historically there have been five bull markets longer than the present one, with three of them lasting close to 13 years.

Given the transformational impact of AI on our economy and the world more broadly (with commensurate risks, of course), it is conceivable that we are yet in the early to middle innings of what will prove to be another (perhaps record setting) bull market. Again, only time will tell, but the big picture view suggests the rally of the last few years might yet have legs.

Looking more broadly at the economy: consumer and business leverage in the US are okay, banks are well capitalized, private credit has issues but apparently these are not systemic in nature (according to the PE firms themselves and I am aware of the incentive problem involved here), there is a massive boom to build out AI and supporting infrastructure, defense spending is headed way up, AI seems to be helping not hurting entry-level jobs, and the Fed will face political pressure to be accommodative.

In light of all this, our own view is that markets remain well positioned to continue to rally over the medium term, though given their stratospheric rise of late, a bit of a pullback might be in order in the short term.

Working with QuantStreet

QuantStreet offers financial planning, wealth management, model portfolios, portfolio analytics, and a platform for advisors looking to gain independence. The firm’s investment approach is systematic, data-driven, and shaped by years of investing experience. To work with or learn more about QuantStreet, join our mailing list or contact us at [email protected]. Also, please sign up for our Substack.

QuantStreet is a registered investment advisor. Registration does not imply a certain level of skill or training. All financial forecasts are fraught with risk and uncertainty. Our views may prove incorrect and market outcomes may be materially worse than we anticipate. Please see our full disclosure about the limitations of forward-looking statements and the risks of investing at https://quantstreetcapital.com/blog_disclosure/.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.