In my 45 years in the investment business, we’ve observed numerous peaks of excitement. In 1987, a bull market that started at a 1982 bottom below 800 on the Dow Jones Industrial Average (DJIA) peaked at 2,722. It then crashed 43% in 78 days.

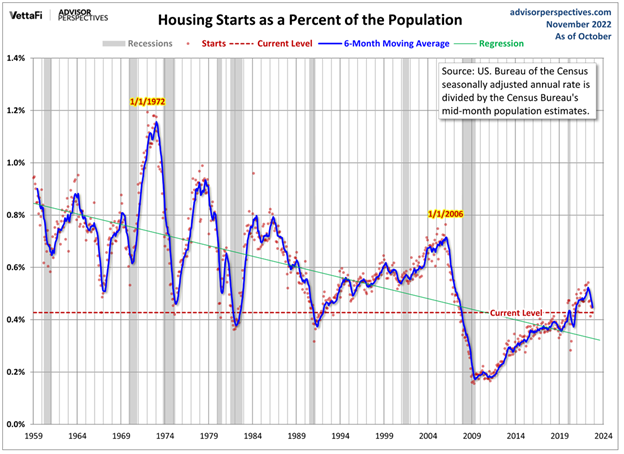

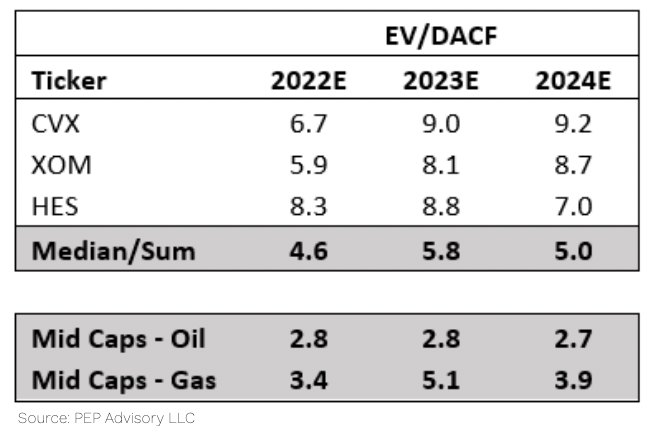

We are expecting inflation in energy prices and a decline in interest rates when the poop hits the AI mania fan. For these reasons, we are overweight in oil stocks and home builders. These industries prospered in the 1970s, once the stock market mania broke in late 1972!

There is a big difference between betting on something and investing in meritorious companies with long holding periods. Although we are no longer shareholders of Berkshire Hathaway, Warren Buffett shared some wisdom with everyone recently.

Spring training started in Arizona recently and it reminded us of the 2025 World Series. The series ended a Major League season which was delightful and instructive.

There are two sides to the current stock market. One side, ignorance avoidance, requires us to know where the money is. The other side, stock selection, is to know where the money is going.

Mark Twain said, “History never repeats itself, but it rhymes!” Time magazine just came out with its “Person of the Year.”

My first experience with a major economic/stock market bubble was the dot-com bubble of 1998-2000. Many investors forget that the Nasdaq and S&P 500 Index bubble that ended March 10, 2000, was the first bubble in a series of three bubbles.

One of the things we have in common with Warren Buffett is that we started our risk-taking career handicapping at racetracks. Buffett handicapped the horse races in Omaha, and I handicapped greyhound races near Portland at Multnomah Kennel Club in Gresham, Oregon.

As summer comes to a close and life adjusts back to normal for most of us, we thought it was a great time to get back to basics and take a look at the current U.S. stock market.

Is the U.S. economy “all twisted up in the game” with the S&P 500 Index dominated by technology/AI stocks? How much is investor confidence affecting consumer confidence? How much has the increase in financial advice and advisors been fed by the success of this stock market?

When you have a significant underperformance period, investors have a good reason for wondering if you’ve lost your investing mojo.

We have a truly inspiring corporate leader among the companies in our portfolio. We don’t believe the global equity markets have realized it yet.

Our long-time investors are probably wondering why we haven’t made any gains over the last 18 months.

In light of the announcement that Warren Buffett is stepping down, we thought it very useful to share some of the keynote talk I did at the University of Nebraska-Omaha Business School last Friday night (thanks to its wonderful director, Robert Miles).

In the Middle Ages, a common form of punishment was some form of mutilation, which included cutting off the nose of a prisoner or purposefully marring one’s own appearance before the arrival of conquering armies

Investors who have come to us in the last three to four years are probably wondering if we’ve been here before. By here, we mean a stretch of significant underperformance relative to our benchmarks. The answer is, yes. Let’s review those prior circumstances to see if we can learn something about where we might be headed.

Karen Carpenter was one the greatest singers of my lifetime. One of her biggest hits was called, “Top of the World.” The key line of the song says, “I’m on top of the world looking down on creation and the only explanation I can find, is the love that I’ve found ever since you’ve been around, you most put me at the top of the world!”

All portfolio managers practice a stock-picking discipline in which they make choices. Growth stock investors attempt to predict which companies will grow the most in the future and compare the growth they expect to what they have to pay to participate.

How does the euphoria for stocks in the days after the 1980 election contrast with today’s Trump election euphoria?

Barry Bannister, Managing Director and Chief Equity Strategist at Stifel, put out an excellent research piece on future returns based on what industry folks call the “equity risk premium.”

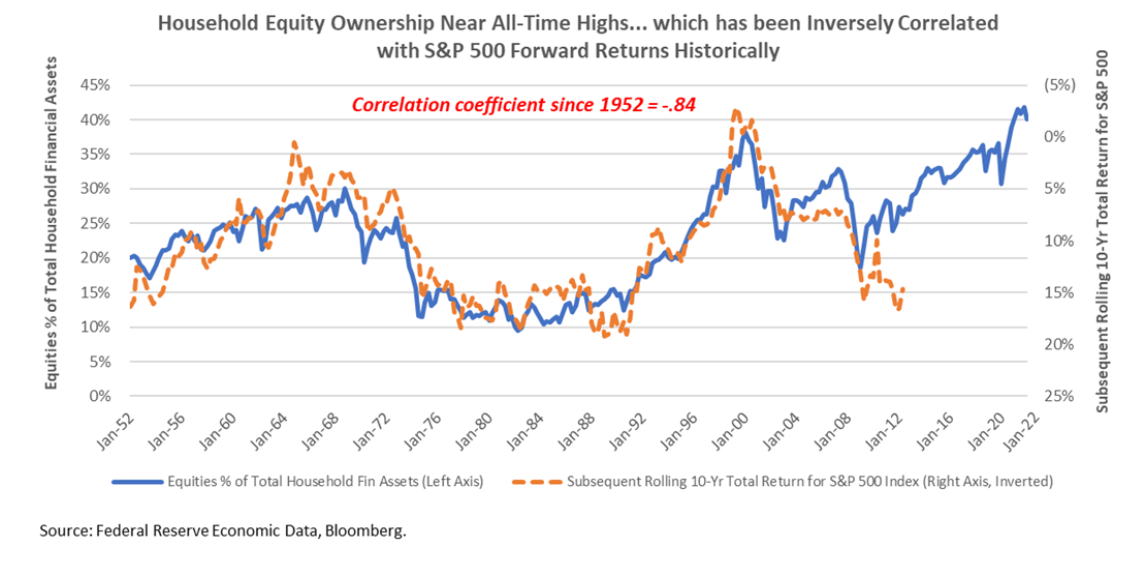

We learned a long time ago that we wanted to know what smart professional investors were doing. It’s always better to know who is smart rather than being smart yourself. Therefore, we’ve constantly kept track of insider buying, what great investors like Warren Buffett and Carlos Slim were doing, and what the most successful hedge funds were up to. A recent chart stopped us in our tracks.

We’ve always admired the great artistry of David Byrne from the Band Talking Heads. My favorite song of theirs is “Once in a Lifetime.” We think this song can tell our readers a great deal about how to look at our portfolio as we navigate an expensive and maniacal S&P 500 Index environment.

The news of Bill Walton’s death from brain cancer hit me hard. In the Portland Memorial Coliseum, there were 12,665 seats, and I had one of those top-row nose-bleed seats for the sixth game of the NBA finals in 1977.

Back in 1993, a brilliant satirist by the name of Ivan Reitman produced a movie called Dave. It was the story of a life-threatening stroke besetting the President of the United States of America.

At the Berkshire Hathaway Annual Meeting we marked what we believe is the end of an era both for Berkshire and for the S&P 500 Index.

The most interesting thing about 1968-1969 was the agreement about the stock market future between the greatest growth investor at that time, T. Rowe Price, and the greatest value investor of all time, Warren Buffett.

As a child, baseball became the core of my life. Collecting baseball cards, watching games on TV, and playing in Little League and neighborhood games absorbed my time outside of grade school. Out of this came a desire to know baseball history and become a statistics junkie.

The U.S. Federal Government has set a net zero carbon goal by 2050. Tremendous resources have been applied with borrowed money to fund these goals and subsidize money-losing green investments.

A friend of our stock picking discipline reminded us of a very important force in the stock market. It was called the 70/20/10 rule, and it was promoted by Roger Edelman, Richard Evans and Gregory Kadlec in an early 2013 Financial Analysts Journal article.

To kick off the beginning of 2023, there continues to be a bias we see in equity investor portfolios. These portfolios have many of the traits investors see at the endpoints of the economy like software, consumer products and computer chips.

What must happen to make these stocks attractive to investors like us?

There were many good things to think about from Warren Buffett’s letter to shareholders which came out recently. In this piece, we’d like to drill down on two subjects that Buffett highlighted.

As a young stockbroker in the 1980s, I was very enamored with T. Boone Pickens.

A recession is two consecutive quarters of economic contraction.

In 1817, David Ricardo developed his theory of comparative advantage to explain why countries engage in trade together, even when one country has an absolute advantage.

As we start the year 2023, we are reminded of the profound poetry from the band, Echosmith, in the song, “Cool Kids.” It can teach us about what it takes to succeed in long-duration common stock investing currently.

As we’ve hit the halftime mark for the investment year 2022, we are faced with a daunting two-headed monster.

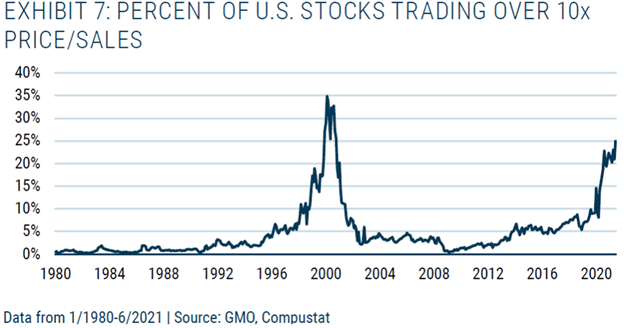

Totally Addressable Markets (TAM) are at the heart of what Charlie Munger calls the biggest euphoria episode he has ever seen in his career. We believe that the coming stock market failure emanating from the over-pricing of the U.S. stock market is closely tied to TAM.

Warren Buffett released his 2021 Berkshire Hathaway Annual Letter on Saturday, February 26, 2022. He seemed to want to talk about almost anything besides the stock market.

We have been reading a book written by David Carey and John Morris called King of Capital. It is the story of the Blackstone company and its key founder, Stephen Schwarzman. An economic history from the 1980s through today is included and lays out some excellent reminders of certain disciplines which can create wealth in picking public companies to invest in.

Overall common stock index performance can be a very confusing thing to most investors. From a cyclical standpoint, the history of stock price performance in the U.S. is closely associated with the Federal Reserve Board. When the Federal Reserve Board reverses an accommodative interest rate policy, it is affectionately referred to as “pulling the punch bowl.”

Warren Buffett and Charlie Munger always refer to Aesop as the originator of investment logic. His first dictum was “a bird in the hand is worth two in the bush.” His second dictum was the fable of the “Tortoise and the Hare.”

At Smead Capital Management, we practice our discipline of picking and owning stocks which meet our eight criteria in both favorable and unfavorable environments. The current “blithe spirits” were brought to mind in a movie of the same name.

During our quarterly webcast last week (October 21, 2021), someone asked us a great question. They asked, “Does the ten-year Treasury bond rate at 1.65% and an inflation rate of 5% teach us that inflation will be transitory?” It is an important question because the majority of economists and market strategists are betting that inflation is transitory.

We have argued for years that the biggest mistake being made by Berkshire Hathaway was not giving shareholders access to the thoughts and investment discipline of their two talented stock pickers, Ted Weschler and Todd Combs. After all, Buffett calls the shareholders “partners” and has not allowed his partners to understand anything about the strategies and results of upwards of $30 billion of shareholder capital.

The Berkshire Hathaway Annual Meeting was a mixture of caution, wisdom and honesty.

Now that the leaders of the most popular tech companies are going into outer space, we thought it appropriate to consider the return implications of this urge to “explore strange new worlds.”

Even before the war is over, the winning side needs to consider how to “win the peace” which will follow.

Dumb and Dumber was a 1994 movie which tells the story of Lloyd Christmas (Jim Carrey) and Harry Dunne (Jeff Daniels)

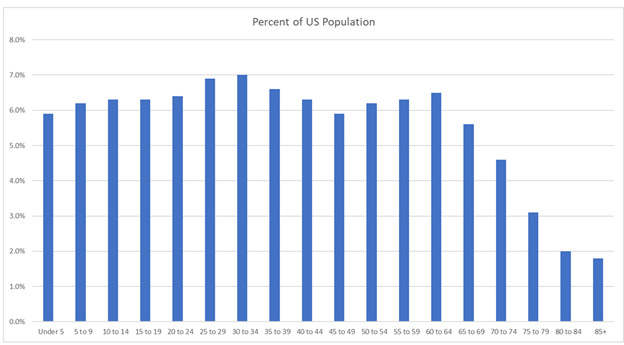

My generation, millennials (those born from 1980 to 2000), have been noted for much of the last 10 years to be a risk averse group.