Most global investors are not attuned to what can be seen on the horizon, not far from shore. After the Great Financial Crisis, Europe was slow to address the underlying capital issues. Rather than guillotining the problems, they allowed a slow bleed to take place.

Shell (SHELL NA) announced last week that they are acquiring ARC Resources (ARX CN). Arc Resources is a gas business in the Montney Region of Canada and is a name that the investors of Smead Capital Management are fairly familiar with.

Relying on the kindness of strangers has never been a good business or investment strategy, but it doesn’t mean that people don’t wish that it worked. The main issue with this hope is that it’s foolish to believe that other people’s grace and money will always be there.

There has been a lot of controversy around the Trump administration’s policy toward the Federal Reserve recently. What is less obvious to most investors is what they’re aiming to accomplish. Trump continues to talk about getting rates lower, and this has been echoed in other parts of the administration as well.

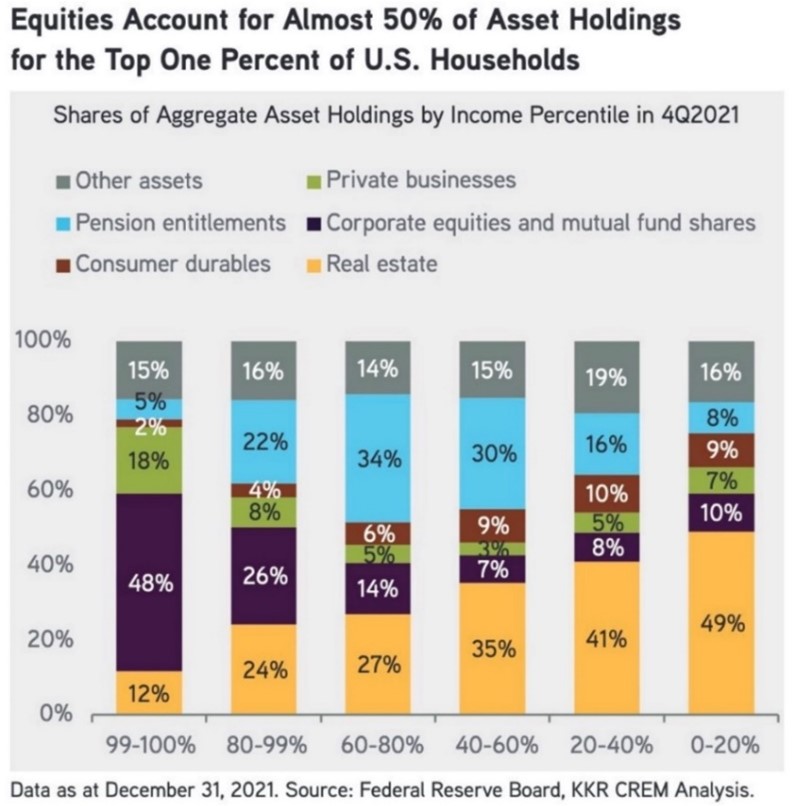

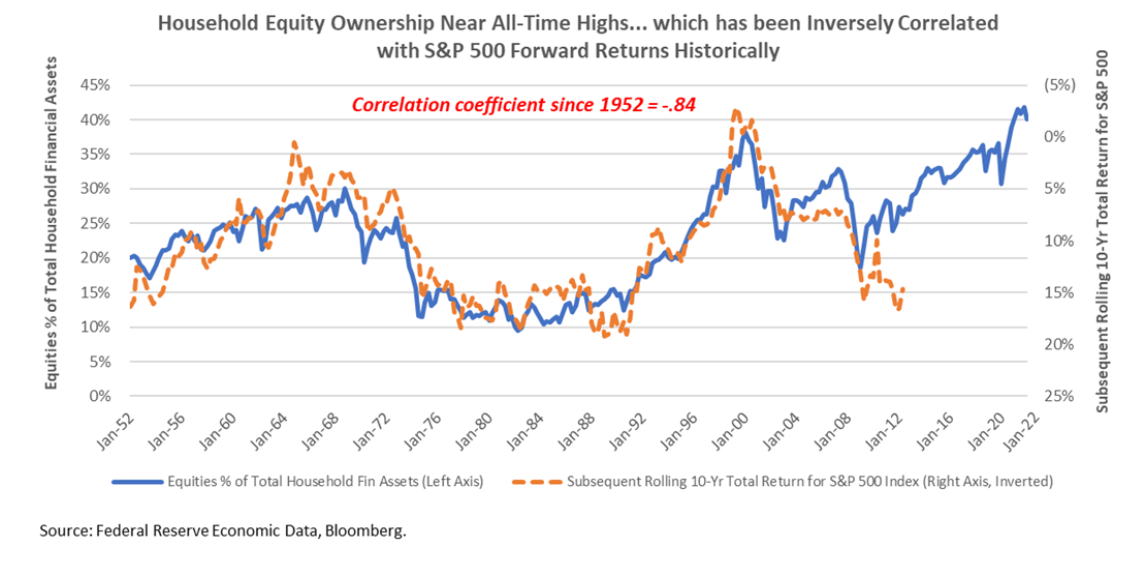

Investors have talked a lot about the Buffett indicator since the Oracle of Omaha began commenting on it. Buffett compared the market cap of the US stock market to GDP.

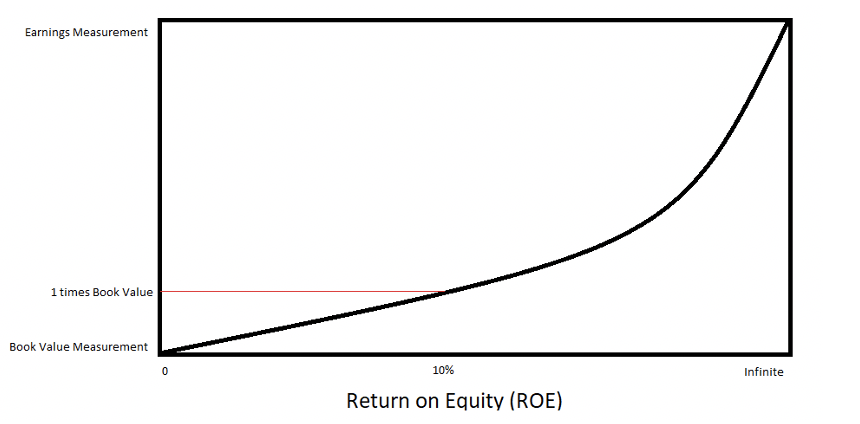

A wise man once said that generally accepted accounting principles (GAAP) is where you start. It may not be the most economic way of looking at a business for various reasons.

When you have a significant underperformance period, investors have a good reason for wondering if you’ve lost your investing mojo.

We have a truly inspiring corporate leader among the companies in our portfolio. We don’t believe the global equity markets have realized it yet.

We’d like to discuss our three worst-performing securities in the US portfolio to help our investors understand why we are sitting on our hands and allowing our discipline to proceed.

When you grow up with a father who worked in the brokerage business, you hear a lot of stories.

My colleague Will Keenan recommended an outstanding book, The Professor, the Banker, and the Suicide King, by Michael Craig. The book is a short and entertaining read of how Andy Beal played the best poker players in the world heads-up. He not only gambled toe-to-toe, but he also reminded them that they were doing what everyone should think poker is: gambling.

Many investors are bullish, or not fearful, of the future of stock returns. At Smead Capital Management, we continue to explain to our investors how poor the outcomes will be. Some ask when this view will change.

William Thorndike’s book The Outsiders has been considered a classic for some time now. His story teaches readers about the business performance of Henry Singleton, Katherine Graham, John Malone and Daniel Burke.

C.S. Lewis coined the term ‘chronological snobbery’. According to Lewis, the definition of chronological snobbery is “the uncritical acceptance of the intellectual climate of our own age and the assumption that whatever has gone out of date is on that count discredited.”

The paradox that this marriage potential created at the college was that the odds are good, but the goods are odd. This is the statement that can be made for common stock investing today.

In the early 2020s, the stock market looked much like basketball used to: a big man’s game. As examples, money management firms like Vanguard and Blackrock lumbered to higher heights of assets while the passive firms swallowed more market share.

To kick off the beginning of 2023, there continues to be a bias we see in equity investor portfolios. These portfolios have many of the traits investors see at the endpoints of the economy like software, consumer products and computer chips.

The news of the shocking OPEC+ announcement of a supply cut is saturating the minds of investors and market prognosticators.

The events that began with Thursday’s tumult in financial stocks and precipitated the FDIC takeover of Silicon Valley Bank and Signature Bank were swift.

On February 5, 2023, Charlie Munger sat down as the Chairman Emeritus of the Daily Journal Corporation (DJCO) to answer questions from shareholders and the public.

We are closing in on what we think may be the question of the decade. If a majority of stock market capitalization in the US is passive or indexed, does this cause problems for stock markets?

In 1817, David Ricardo developed his theory of comparative advantage to explain why countries engage in trade together, even when one country has an absolute advantage.

I was reminded in a recent read of Robert Hagstrom’s book, Warren Buffett: Inside the Ultimate Money Mind, how Warren Buffett and Charlie Munger define the economic earnings power of a business.

In the 1994 comedy film, Ace Ventura: Pet Detective, Lt. Einhorn is the female leading the Miami police’s investigation of the disappearance of the Miami Dolphin’s mascot, Snowflake.

If you were walking down the street and saw a $100 bill just sitting near the curb, would you pick it up?

The investors of Smead Capital Management have been hearing us talk about ‘First World Problems’ recently.

While reading Jeff Nussbaum’s new book Undelivered, I came across the story of Boston’s Mayor Kevin White and the 1974 busing of Boston public school students.

As we’ve hit the halftime mark for the investment year 2022, we are faced with a daunting two-headed monster.

Chairman and largest shareholder, Harold Hamm, is trying to own our shares of Continental Resources (CLR US) at a price of $70.

Academics argue that there are three proven factors of investing: Value, quality and momentum.

The future is always unknown.

Moving forward beyond the pandemic of 2020, the theme the world woke up to is that people want more…more home, more land, more entertainment, more goods.

The news of Berkshire Hathaway’s purchases in Occidental Petroleum (OXY) has been seismic in our minds, but to most investors it has been but a whimper

In an upcoming episode of A Book With Legs podcast, we interviewed Robert Hagstrom on his book, Investing: The Last Liberal Art.

A couple of weeks ago, we gave a presentation at the first annual Smead Investor Conference near our headquarters in Phoenix.

Ben Graham is ascribed as being the father of value investing.

The beginning to 2022 has been dark to say the least.

In the depths of the lockdowns in March and April, we were together at home, day after day. The U.S. Federal Reserve Board pumped large amounts of liquidity in our economic system. The U.S. Federal Government followed by providing large amounts of fiscal stimulus in PPP loans...

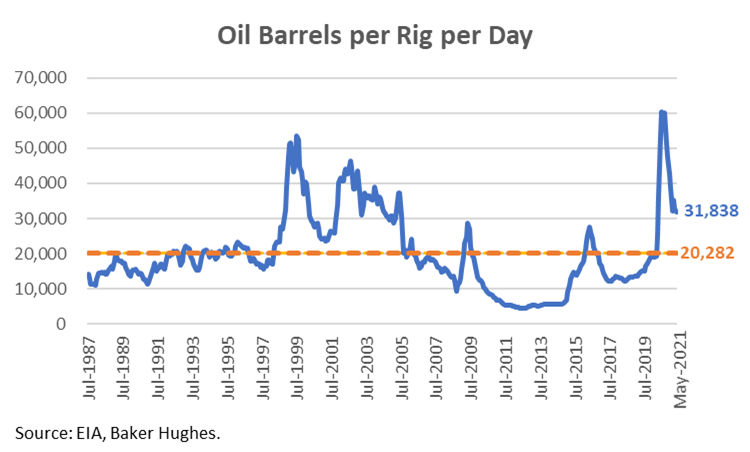

In 2014, famed UK stock picker Terry Smith wrote a piece, titled Shale: Miracle, Revolution or Bandwagon?, in most ways mocking investors excitement in the oil and gas business in the United States of America.

Today’s atmosphere is one that we rarely see as investors. This is not like junk bonds in the 1980’s or the run up in Valeant Pharmaceuticals and the other generic drug companies in the 2010’s. There is not a narrow way of looking at today. It is broad.

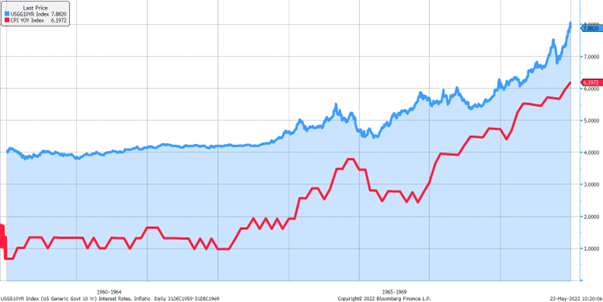

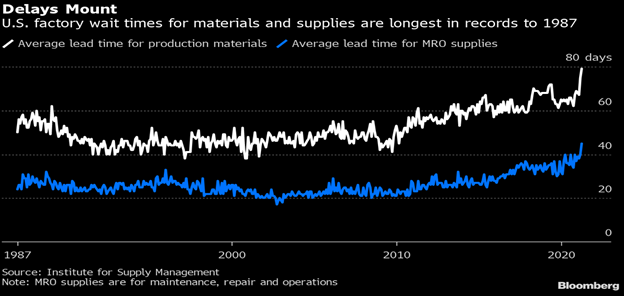

The media and the economics profession are treating inflation like it is a friendly puppy dog. They think you can take it out of its pen and play with it for a while. The popular theory is that you bring it out in a severe dip in economic activity and when the economy gets back on its feet, you kindly ask inflation to crawl back into its pen like any good puppy dog would do.

The talk of inflation today looks much like housing did in 2007. Evidence is mounting everywhere that this is a real long-term problem that is only getting worse. You can read this in the media, but yet security prices don’t reflect how damaging this may be.

Investors often ask our team at Smead Capital Management what we spend our time on. We believe reading is the best use of our time to learn and think about the way that we can profitably apply capital for our investors.

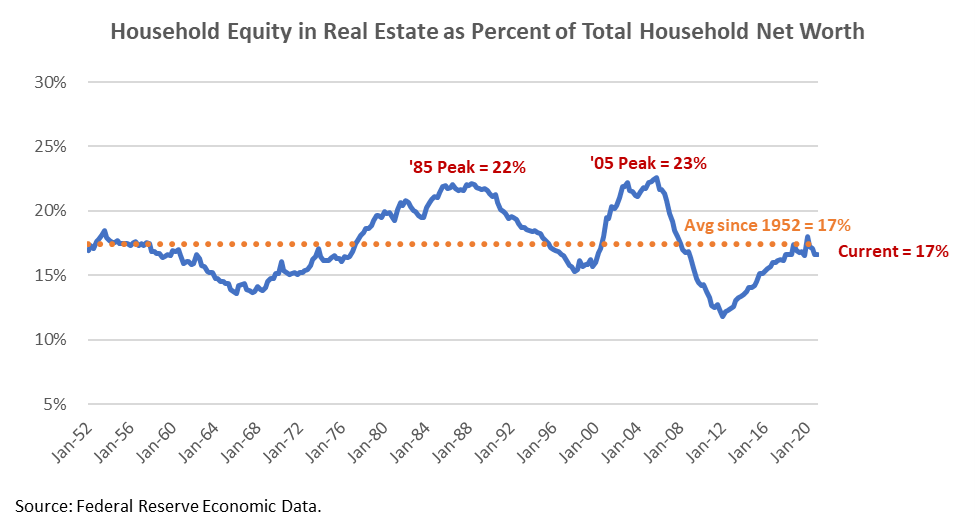

We have been in many discussions with our investors, people in the media and the investment management industry on where housing is today.

On the insistence from a friend and a colleague, I watched the movie There Will Be Blood over the weekend.

At a minimum, the latter part of 2020 and the first half of 2021 will go down as one of the strangest psychological times for common stock investors.

Halfway through the year 2021, we must be reminded to “not confuse brains with a bull market.”

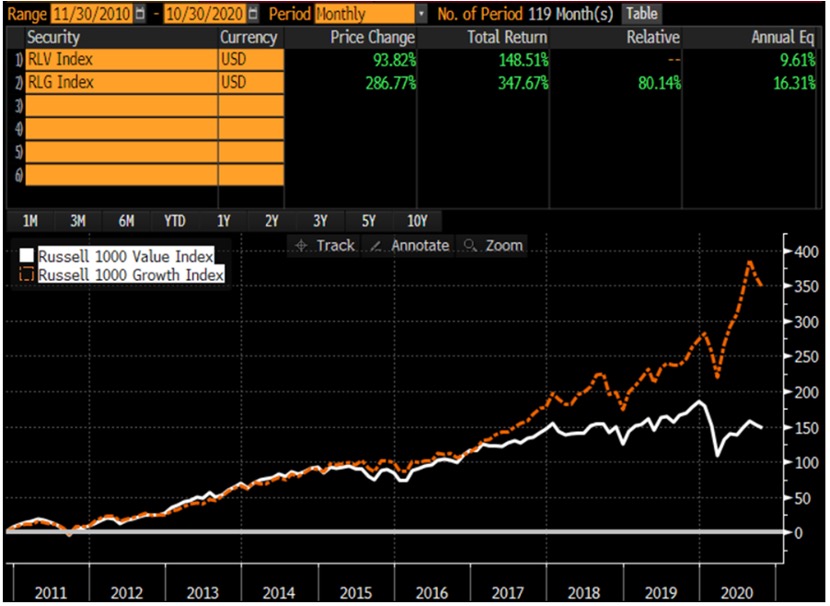

Most millennials have never seen an era where value has done well.

My recent reads have been stuck in the 1960’s, including Adam Smith’s The Money Game and Andrew Knowton’s Shaking the Money Tree.

To say that we were surprised by some of the discussion at the Berkshire Hathaway Annual Meeting would be an understatement. The conversation Warren Buffett and Charlie Munger leaned into on inflation was possibly the most interesting. Warren and Charlie gave large credit to Larry Summers for his willingness to stand alone on the effects of today’s fiscal and monetary policy on prices. We thought this was an ideal time review Buffett and Munger’s discussion and see what conclusions we could draw.