Ever since the pandemic – when surging housing demand collided with a decade of underbuilding – housing affordability has become an increasingly important political issue and a larger focus for policymakers.

The dearth of homes for sale has underpinned the housing market’s surprising resilience and may further lift home prices despite reduced affordability.

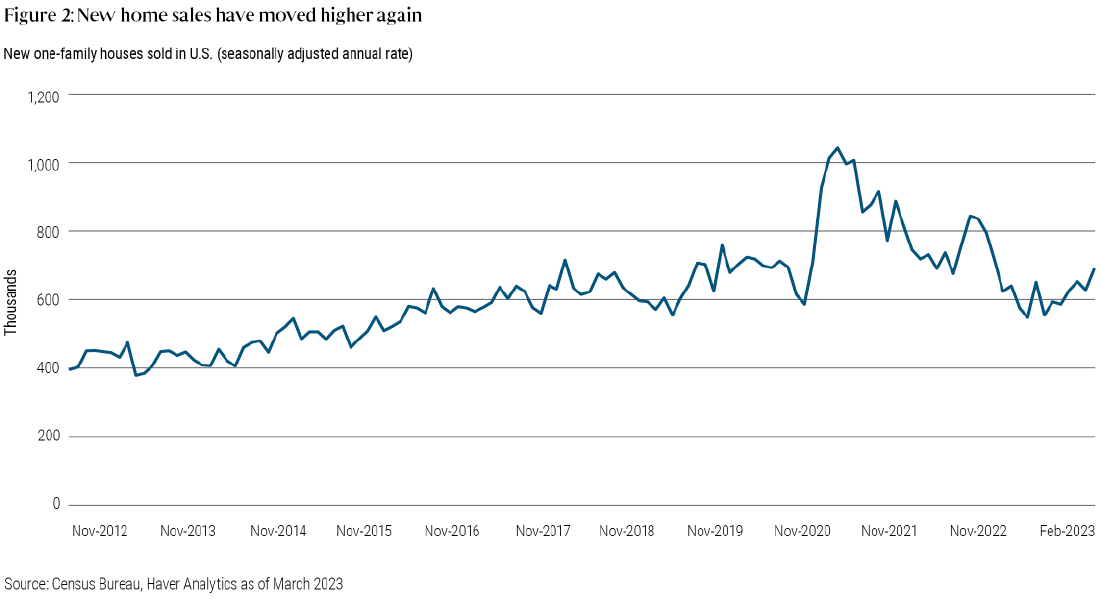

Although affordability remains an obstacle, recent data offer reasons to be more constructive as broader conditions still appear supportive of home prices.

Home price fundamentals suggest appreciation will slow but remain resilient.

We believe the Fed’s mortgage purchase program is helping to bolster economic activity, and accomplishing more than Treasury purchases alone.

The Fed has moved aggressively to stabilize core assets, including mortgages. Yet several market indicators are still concerning.

The Fed could give the economy a powerful boost by maintaining the mix of assets on its balance sheet.

The Fed has another lever to pull to ease monetary policy, one that could increase savings rates and create more disposable income.

Even as the probability of a recession in the near-term remains low, we believe investors should look to sectors that are likely to be resilient in periods of higher volatility.

Many of us who grew up as children of children of the Great Depression may recall our parents imploring us to “Stop throwing good money after bad!” in any number of situations, even if we didn’t always heed their wisdom.

The topic of housing finance reform has come in and out of focus on Capitol Hill since Fannie Mae and Freddie Mac (the government-sponsored enterprises, or GSEs) were taken into conservatorship back in 2008.

Fixed income exchange-traded funds (ETFs) saw a record $126 billion of inflows in 2017, bringing the overall market to nearly $600 billion. The majority of these flows, as well as existing assets under management, are in passive bond ETFs. But are passive, index-tracking approaches the best way to harness the fixed income opportunity set?

Policymakers in Washington have recently expressed growing concerns about the (planned) dwindling of capital levels at Fannie Mae and Freddie Mac – the two government-sponsored enterprises (GSEs) that help finance the vast majority of U.S. mortgages.

Why is the U.S. housing sector diminishing when demand for housing remains robust?

Market participants increasingly expect the Federal Reserve to begin unwinding its balance sheet during the second half of 2017, and many have speculated that the agency mortgage-backed securities (MBS) market – and the U.S. housing market more broadly – could suffer as a result.

The Federal Housing Finance Agency’s proposal to increase liquidity and reduce costs to taxpayers could actually lead to reduced liquidity and higher mortgage rates.