California continues to demonstrate fiscal resilience, supported by strong liquidity balances and the absence of projected cash‑flow borrowing through FY 2026–27. However, Medicaid cost pressures, a progressive tax structure highly sensitive to equity market swings, and constitutional spending constraints remain key differentiators between California and other large states.

Less favorable seasonal technicals, increased focus on municipal-specific policy risks, and severe volatility spurred by higher-than-anticipated tariff increases weighed heavilyon sentiment and resulted in deeply negative total returns and significant underperformance versus Treasuries in March and early April.

Municipal bonds broke their winning streak in October, posting negative total returns alongside broader fixed income assets.

Munis cemented their best “summer” since 2010 after another month of strong performance. Some near-term caution is warranted given that September has been historically challenging. Robust issuance ahead of the election should provide opportunities in the primary market.

Municipal bonds maintained their summer strength and posted a second-consecutive month of positive performance in July.

Municipal bonds posted their strongest June performance since 2019. The asset class outperformed amid improving seasonal supply-and-demand dynamics. Looking ahead, July has historically been the strongest performing month of the year.

Municipal bonds deviated from U.S. fixed income assets and posted negative performance in May.

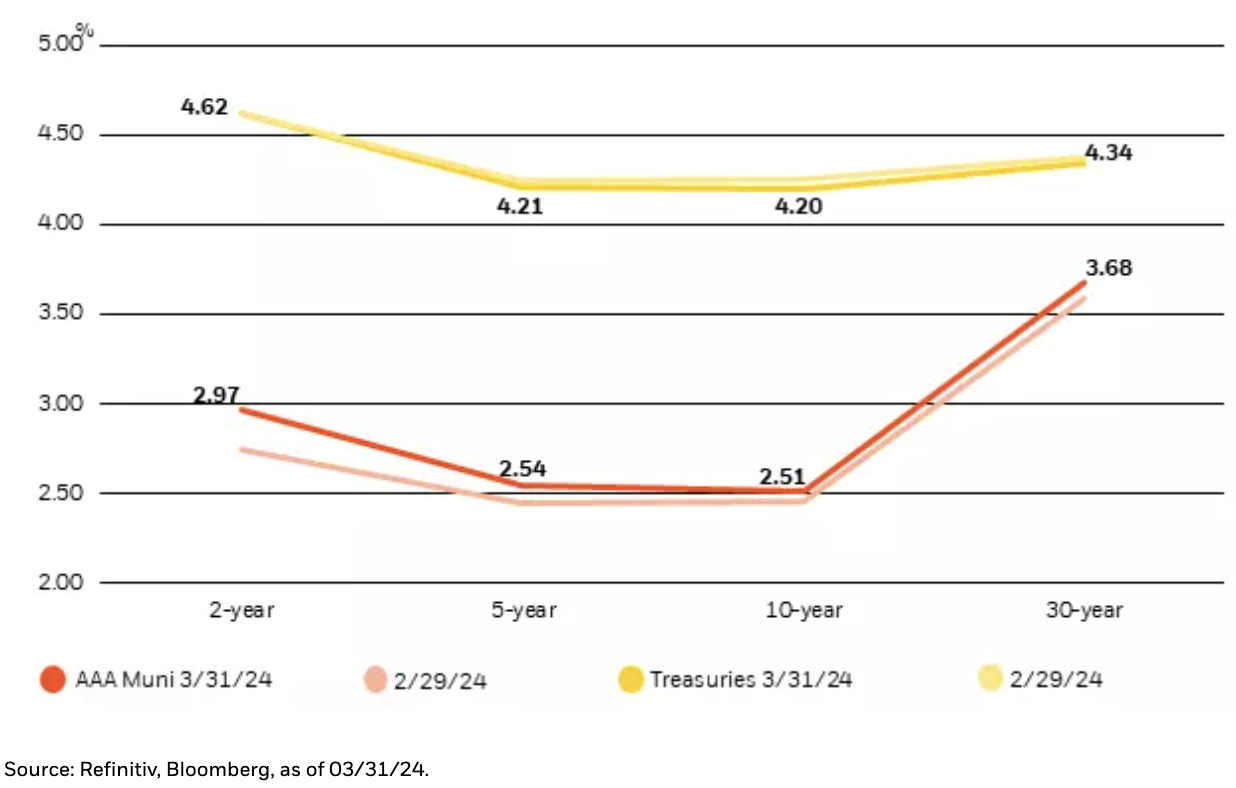

Market update from BlackRock's municipal bond team.

Municipals posted positive performance and outperformed comparable Treasuries in February. We expect supply-and-demand dynamics to turn less supportive in the coming months. After patience to start the year, we would view any material backup as an opportunity to buy.