Anshul Pradhan and Stephen Stanley both saw the current US bond market coming. They just don’t agree on where it’s going.

As the US economy hums along month after month, minting hundreds of thousands of new jobs and confounding experts who had warned of an imminent downturn, some on Wall Street are starting to entertain a fringe economic theory.

Most US Treasury yields climbed to new year-to-date highs, with the 2-year note’s approaching 5%, after hot retail sales data further eroded investor confidence that the Federal Reserve will start cutting interest rate cuts this year.

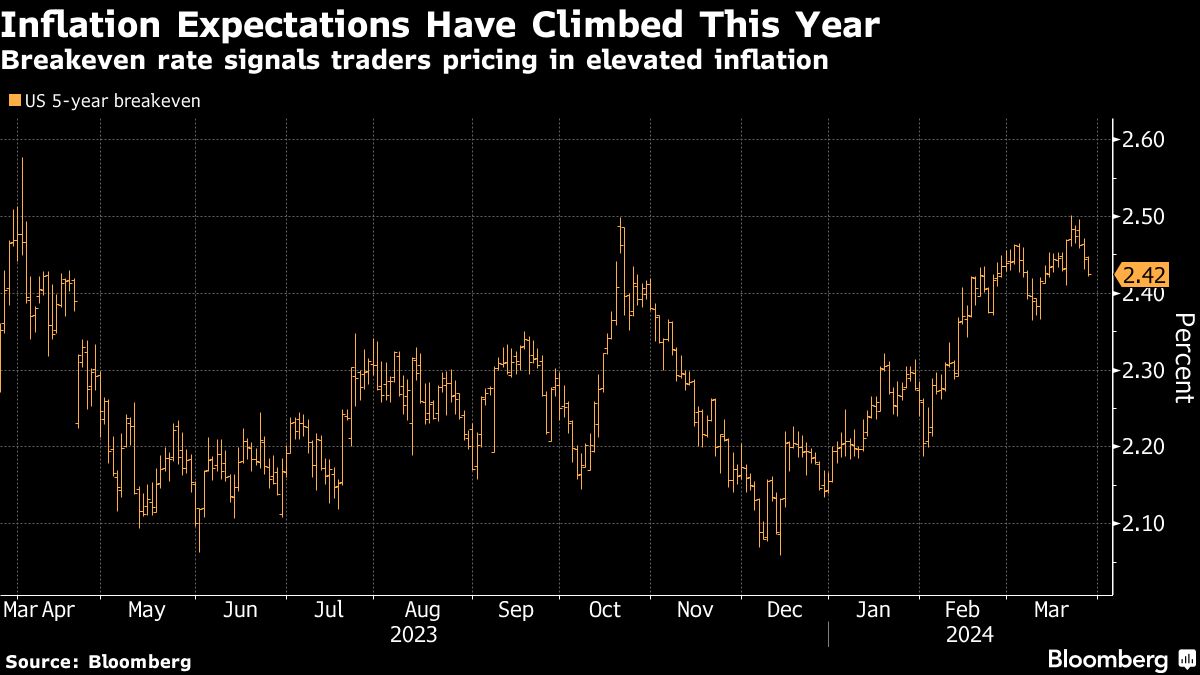

Federal Reserve Chair Jerome Powell’s increasing focus on protecting the job market is encouraging a swath of bond traders putting bets on inflation rates to remain elevated.

Bond traders have plenty on their plates the next couple days, even after they absorb a crucial US inflation reading that stands to shape expectations for Federal Reserve policy for months to come.

What was supposed to be the darling trade of 2024 has unraveled, thanks to the Federal Reserve upending predictions over how fast it would lower interest rates.

Investors are beginning to war-game how the Federal Reserve can manage a US economy that just won’t land, with some even debating whether interest-rate hikes will be needed only weeks after a steady run of reductions appeared all but certain.

Bond traders are finally heeding one of the market’s oldest lessons: Don’t fight the Fed.

Treasury yields tumbled Thursday as a second day of declines for US financial stocks led traders to price in a more rapid pace of Federal Reserve interest-rate cuts.

Jerome Powell delivered a clear message to traders eager for the central bank to start slashing interest rates: Not so fast.

Bond traders looking for something to jolt the $27 trillion Treasury market out of its recent rut will probably still be left waiting for answers, even after a busy week packed with a Federal Reserve meeting, the government’s quarterly debt-sale plans and a slew of economic data.

Bond traders abandoned wagers that the Federal Reserve will cut interest rates in March, pushing swap rates to levels consistent with only about 50% odds of a quarter-point reduction in the federal funds target during the first quarter.

For most of the summer, the chatter in the bond market about swelling US deficits — and the depressing effect it was having on the price of Treasuries — was incessant.

The most accurate US bond forecasters of 2023 say the strong year-end rally won’t stretch into 2024.

The world’s biggest bond market has clawed its way back after spending chunks of 2023 underwater. Now many US debt watchers see the pathway clearing for a real revival.

A prospect that might have seemed unthinkable just a couple short weeks ago is coming into view for bond traders: The potential for US Treasuries to post an annual gain for the first time since 2020.

Losses on longer-dated Treasuries are beginning to rival some of the most notorious market meltdowns in US history.

To judge by recent history, a US government shutdown won’t be a huge event for the bond market. If anything, it could even provide a little short-term relief, since Treasuries usually rally when investors need somewhere to hide.

Bond investors face the crucial decision of just how much risk to take in Treasuries with 10-year yields at the highest in more than a decade and the Federal Reserve signaling it’s almost done raising rates.

Fifty cents on the dollar is a very low price in the world of bonds. In most cases, it signals that investors believe the seller of the debt is in such financial distress that it could default.

The US bond market hasn’t flashed recession warnings so consistently for so long in at least six decades.

The world’s most powerful central bankers have vowed in unison to keep interest rates higher for longer if necessary to tame inflation.

As brutal as it’s been for US bond investors, the math is finally turning in their favor.

Across Wall Street, there’s growing relief that the Federal Reserve — at long last — may be done raising interest rates. But that doesn’t mean turbulence in the bond market will soon become a thing of the past.

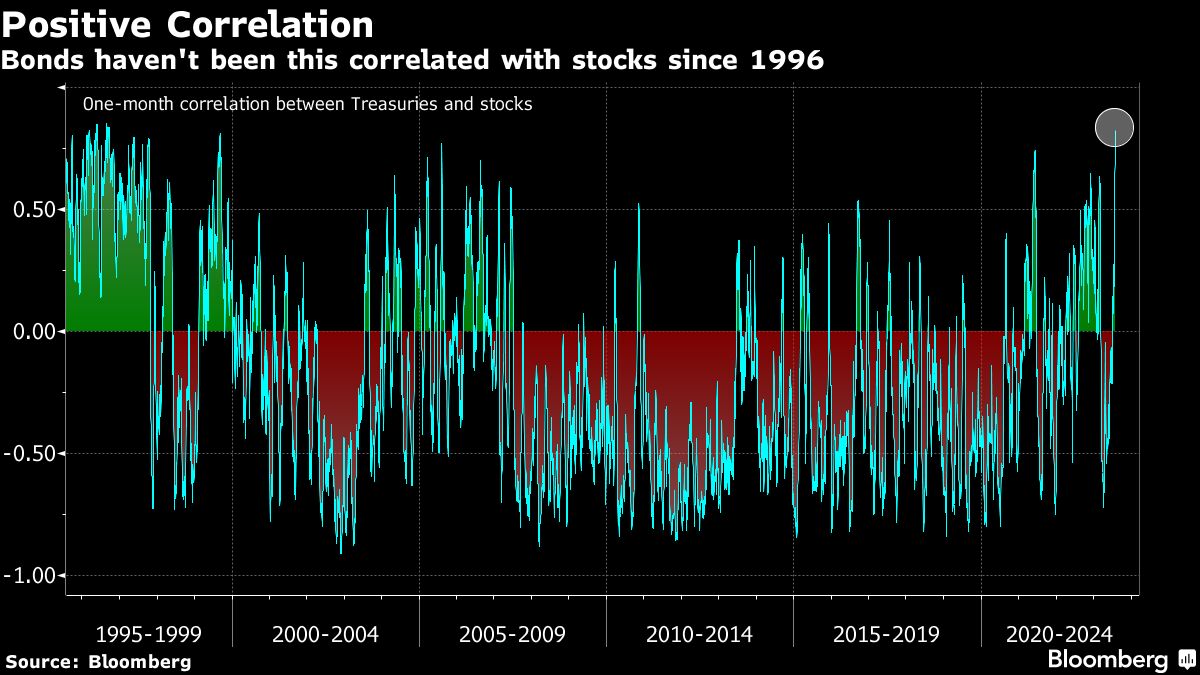

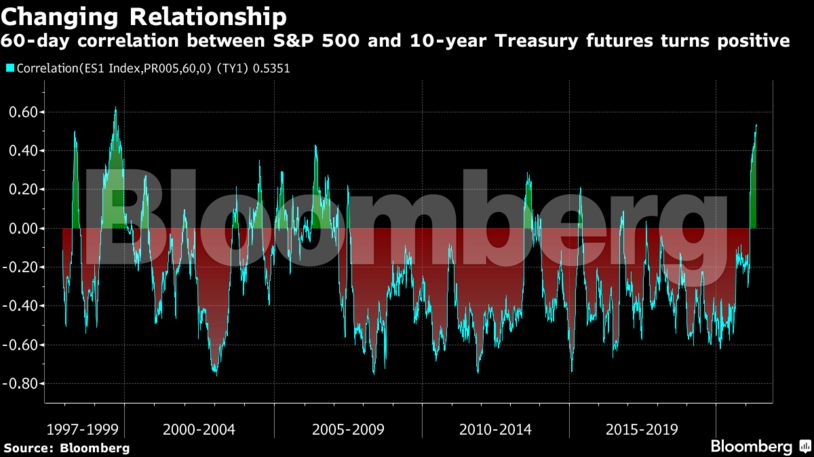

Historically, Treasuries tend to rally when stocks are tumbling, meaning they are negatively correlated. The idea is a cornerstone of the popular 60/40 strategy that uses an allocation to bonds as well as stocks to reduce the volatility of the overall portfolio.

In what was a brutal 2022 for investors, there was at least one sure-fire, money-making proposition for much of the year.

Listen to Wall Street’s top economists and you’ll hear the same message again and again: The risk of a recession is fading fast. And yet, in the bond market, the traditional warning that a downturn is near — an inversion of the yield curve — keeps getting louder.

While the deeply inverted yield curve has stoked anxiety among investors about the prospect of a recession, Goldman Sachs Group Inc. has a different message: stop worrying about it.

Investors loading up on long-term bonds have a history at their back.

The bond market’s re-energized bulls may want to dial down their excitement because their fortunes hinge on whether an abstract, almost elusive number, is as low as they assume.

Some of the biggest bond managers are sticking to their bullish view on the market for US government debt, even as that trade looks riskier by the day.

William Eigen isn’t about to apologize for his bond fund’s performance this year. Yes, his $8.7 billion JPMorgan Strategic Income Opportunities Fund is trailing about 60% of its peers after trouncing nearly every one of them last year.

The once-hot Wall Street trades of 2023 are all falling apart, in a fresh blow to market pros blindsided again and again ever since the pandemic broke out.

Bill Gross, the former chief investment officer of Pacific Investment Management Co., recommended buying short-term Treasury bills, expecting the debt-ceiling issue eventually gets resolved.

When March’s bank failures ignited a historic bond rally, few, if any, made more money than Josh Barrickman. His army of funds gained roughly $26 billion, the equivalent of more than $1 billion in paper profits every single trading session.

This year’s top US bond managers agree that Federal Reserve interest-rate cuts are inevitable this year. The main debate they see is how deep the economic pain gets.

Daniel Ivascyn rode one big trade all the way to the top of the bond-market universe: speculative mortgage debt that he scooped up on the cheap in the wake of the great financial crisis.

The bond market humbled Wall Street’s best and brightest in 2022.

Bill Gross pioneered the “total return” strategy in the 1980s that revolutionized the once-sleepy bond market.

Ray Dalio came out with a gloomy prediction for stocks and the economy after a hotter-than-expected inflation print rattled financial markets around the globe this week.

Bond bulls, while savoring a stellar rebound in returns fueled by growing recession fears, are braced for potential setbacks.

Signs of a rapidly deteriorating US economic outlook have spurred bond traders to pencil in a complete policy turnaround by the Federal Reserve in the coming year, with interest-rate cuts in the middle of 2023.

There are no shortage of bears making similar claims these days. Between the Russia-Ukraine war, the aggressive tightening by the Federal Reserve, soaring inflation and Covid lockdowns in China, there are plenty things to worry about. The S&P 500 has already lost 12% this year, while the Nasdaq Composite cratered into a bear market after sliding more than 20% from its peak in November. Key bond benchmarks are down more than 10%.

The bond market is dialing back expectations for how quickly and steeply the Federal Reserve will raise interest rates as Russia’s war in Ukraine threatens to exert a drag on global economic growth.

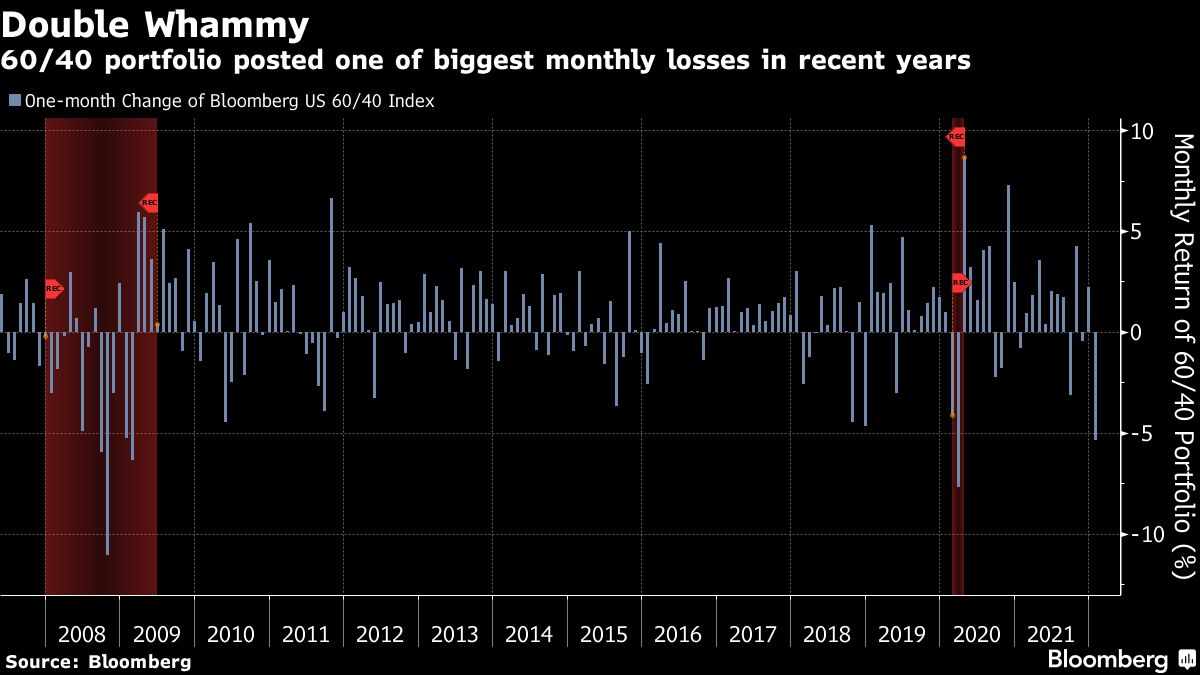

A bedrock of long-term investing, a portfolio split 60/40 between equities and high-quality bonds, is set for its worst monthly slide since the market meltdown in the early days of the pandemic.

Bonds aren’t working as a safe haven like they used to.