Three powerful forces have unleashed a volatility storm in stock markets this year.

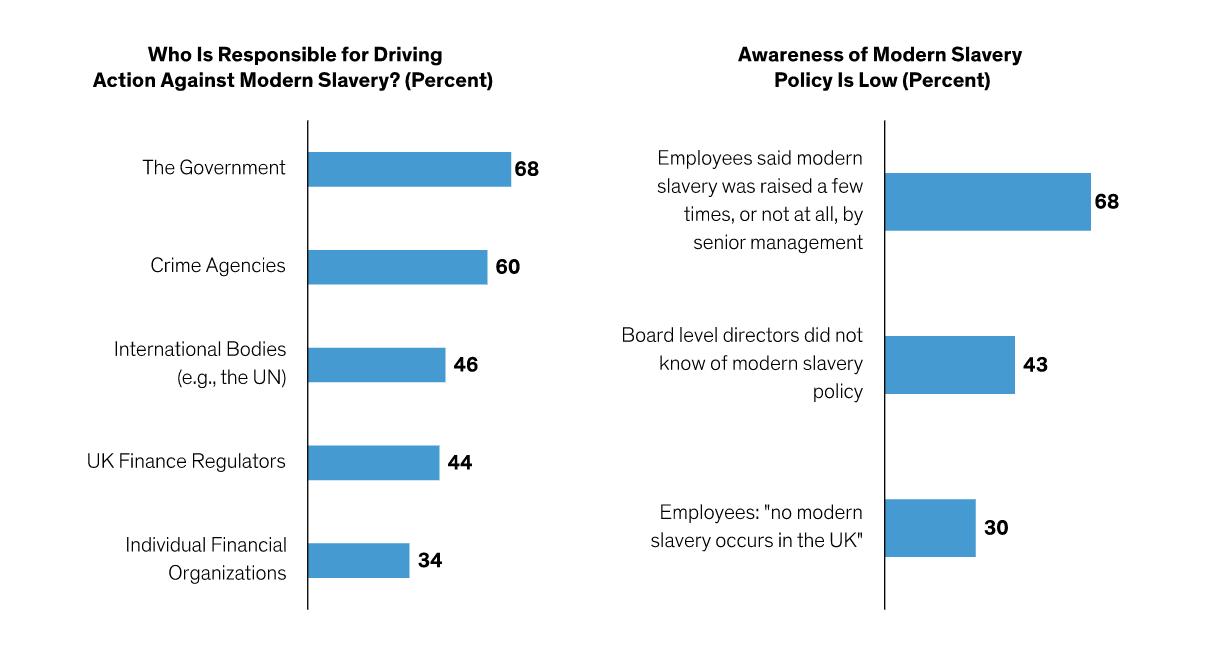

Modern slavery is a lucrative business that can’t exist without the financial system.

An unfriendly macro and market landscape is making life harder for investors today, with traditional core bonds coming up short on income. In our view, focusing on generating efficient income is an effective approach to tackling the challenge of mixing the key building blocks of rates, credit and growth.

With the world facing inflationary and geopolitical hurdles, economic growth is poised to slow. In this environment, investors in growth stocks must identify companies with the right features to overcome headwinds to earnings.

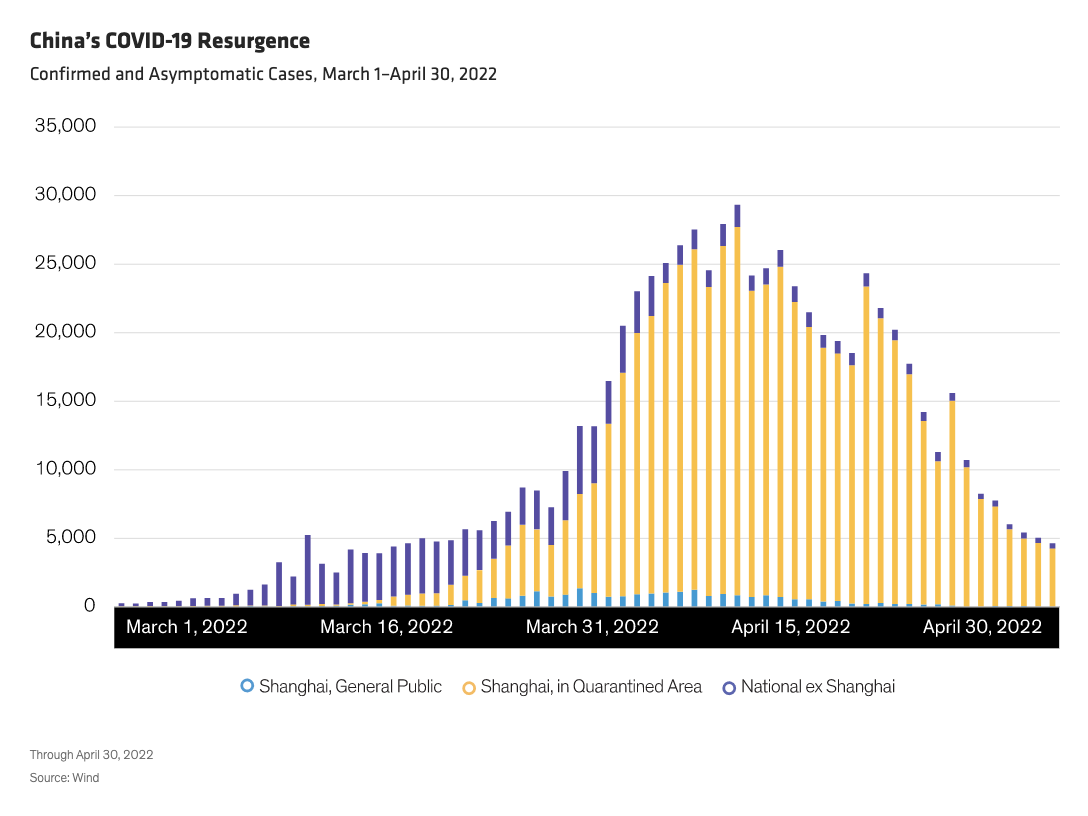

COVID-19’s resurgence in China has cast doubt over the government’s ability to meet its 2022 growth target of around 5.5%, which officials affirmed in March, before the scale of the latest outbreak became clear.

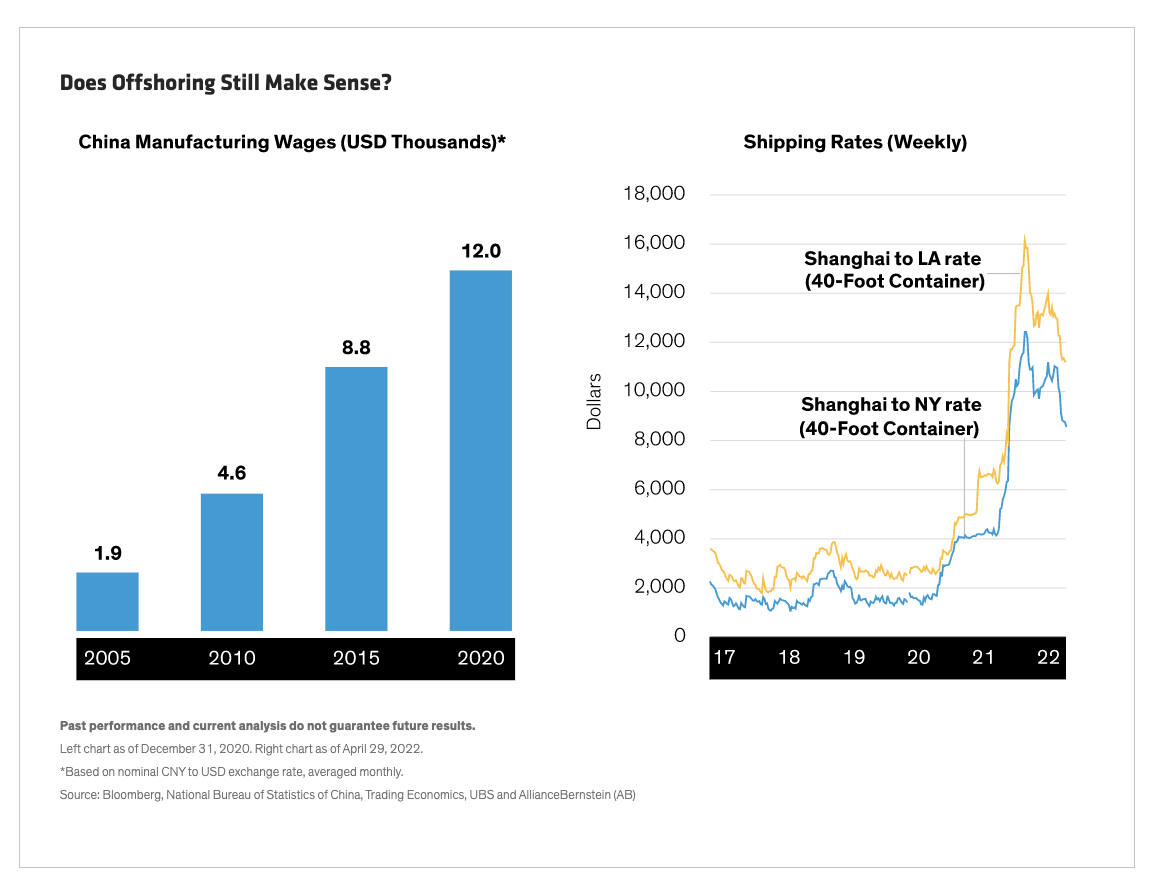

Many companies are rethinking supply chains amid disruptions from the war in Ukraine and the pandemic.

As of this writing, Russian forces are reorganizing in eastern Ukraine, and fighting is well into its second month. Supply chain disruptions continue, gas prices are reaching all-time highs, inflation has become a constant concern, and some analysts are predicting that the Fed will aggressively raise rates.

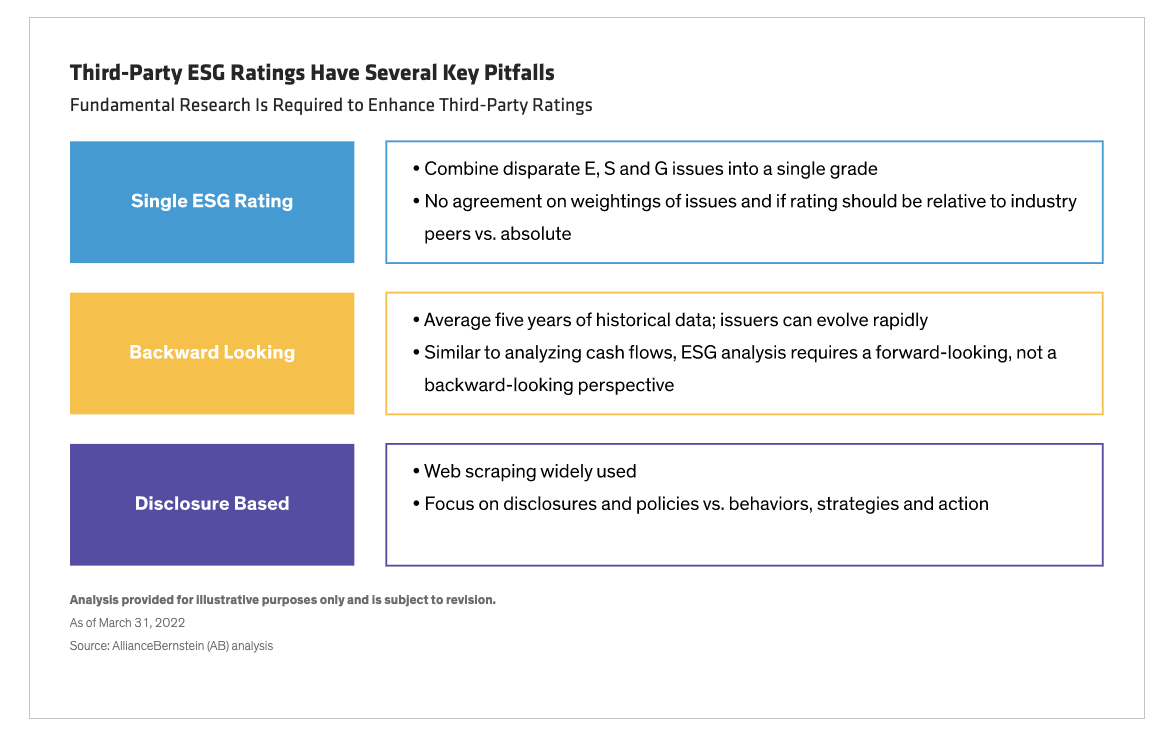

Environmental, social and governance (ESG) ratings are a popular way to search for companies that meet specific criteria in a responsible investing agenda.

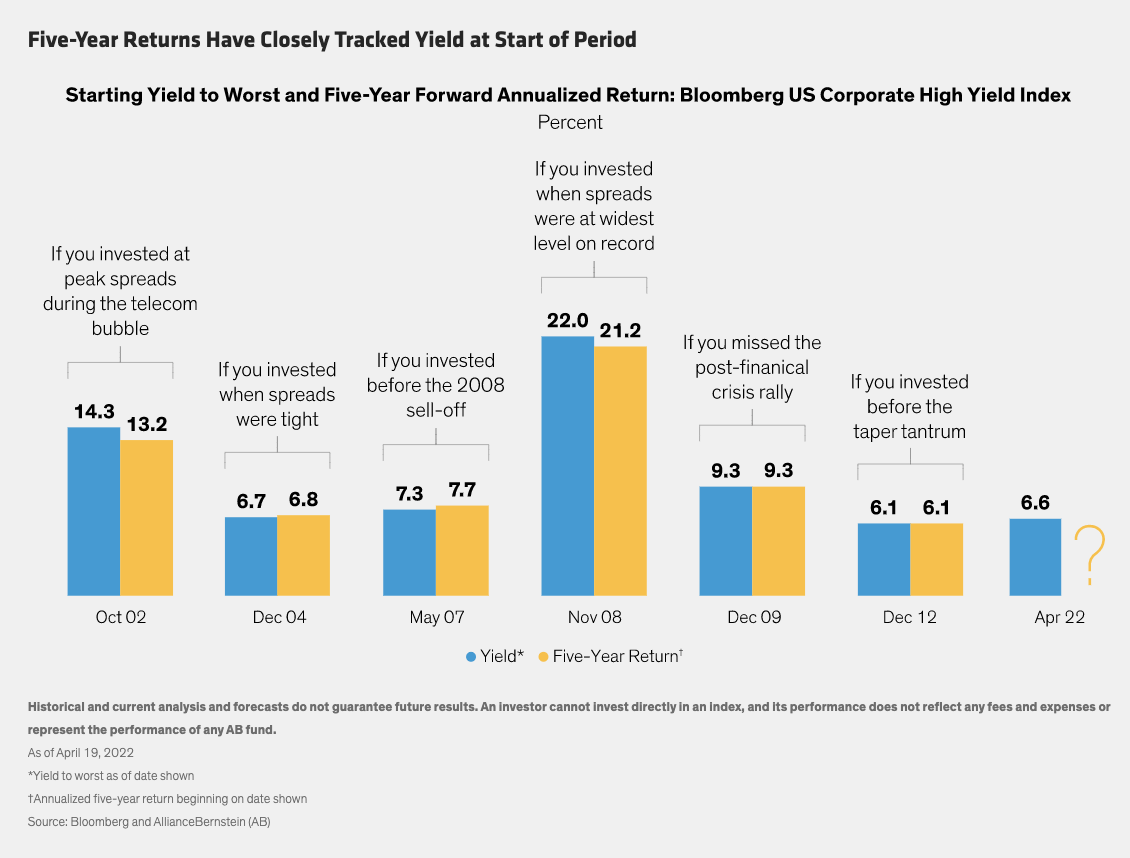

High-yield bonds have a reputation for volatility.

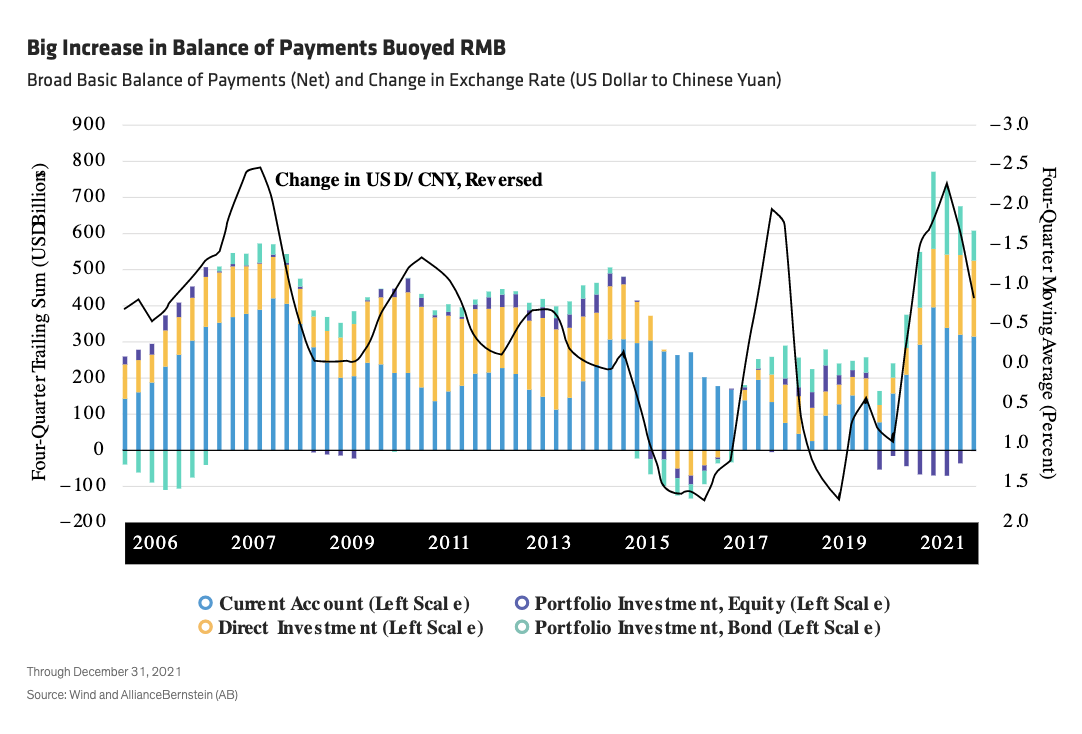

China’s currency, the renminbi (RMB), remains strong even though many of the factors that have driven its performance over the last two years have weakened.

Supply-chain disruptions are testing companies around the world.

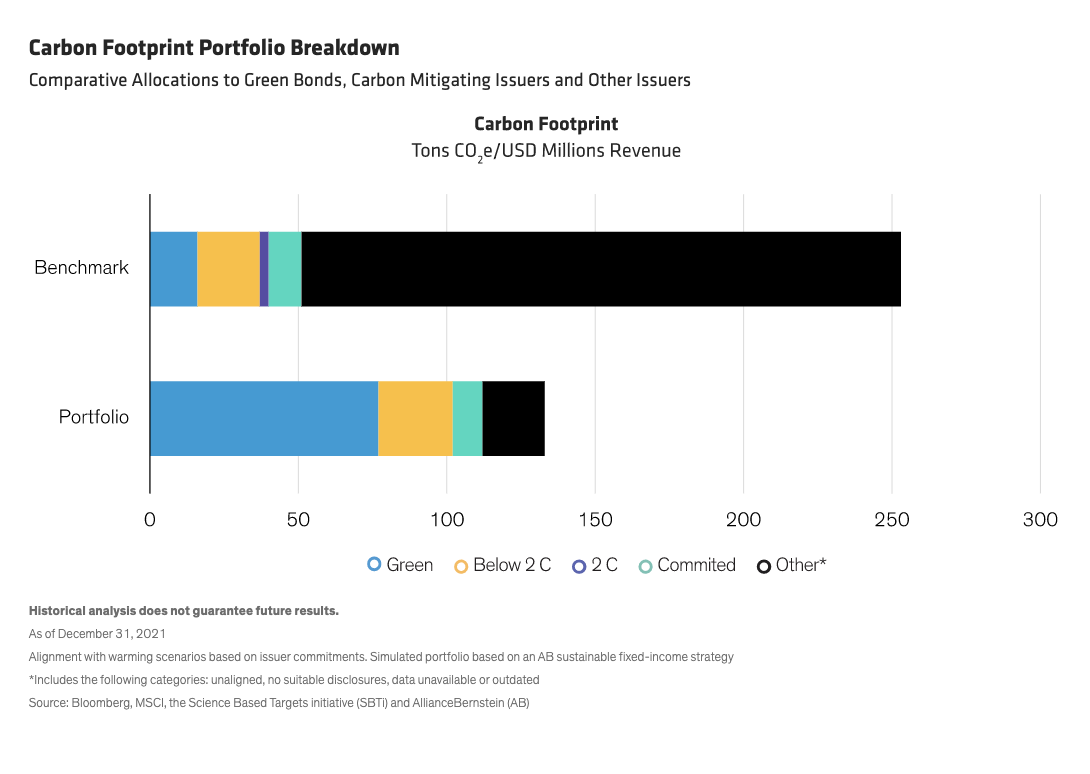

Transitioning to a net-zero carbon economy* is vitally important, and corporate bonds will play a critical role in the transition.

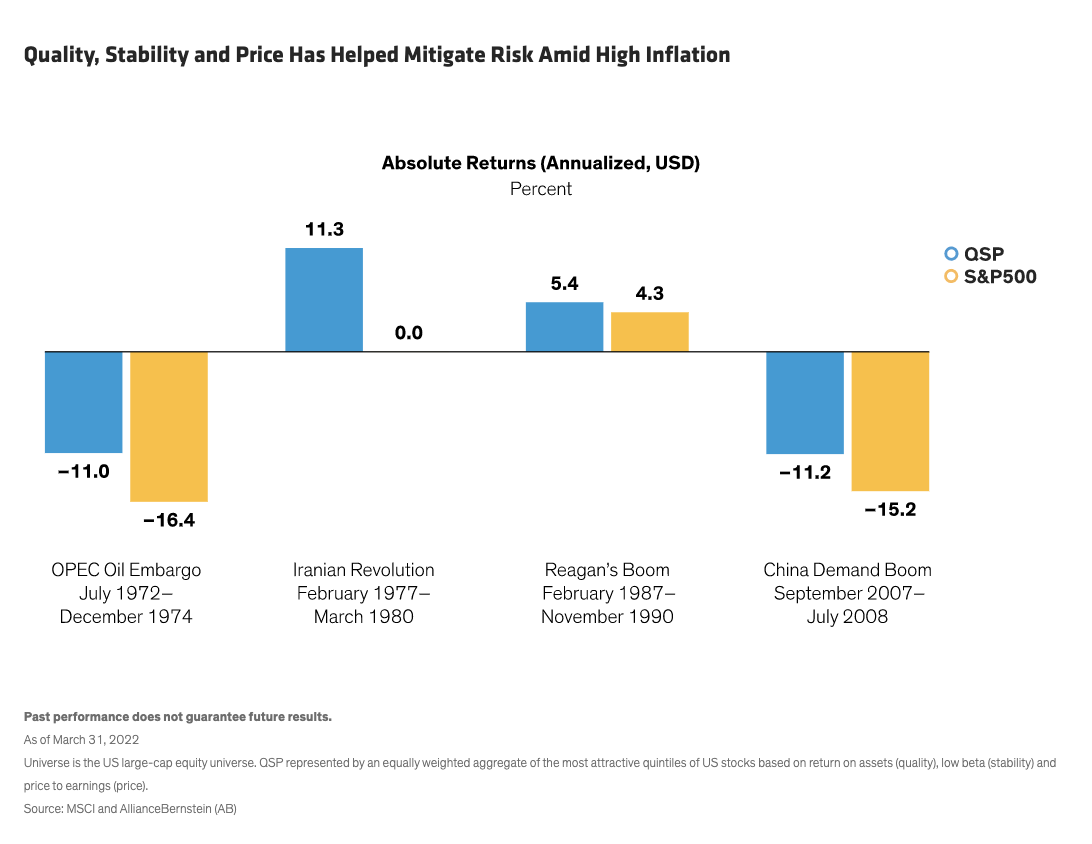

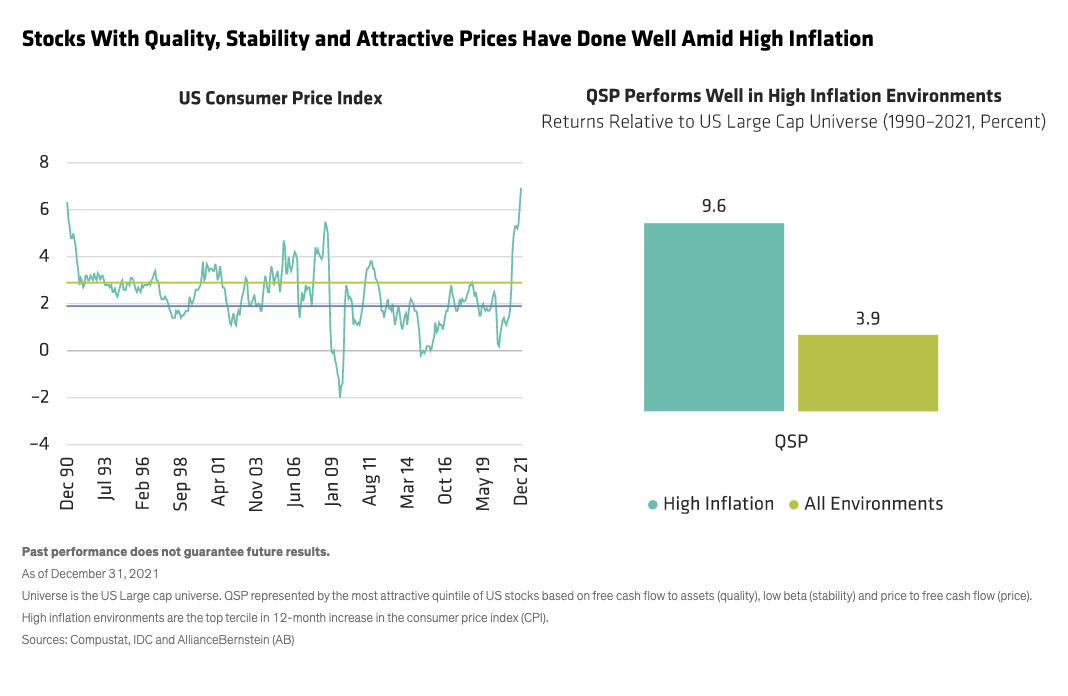

The highest inflation in 40 years has spurred more investors to search for assets that can help offset its bite.

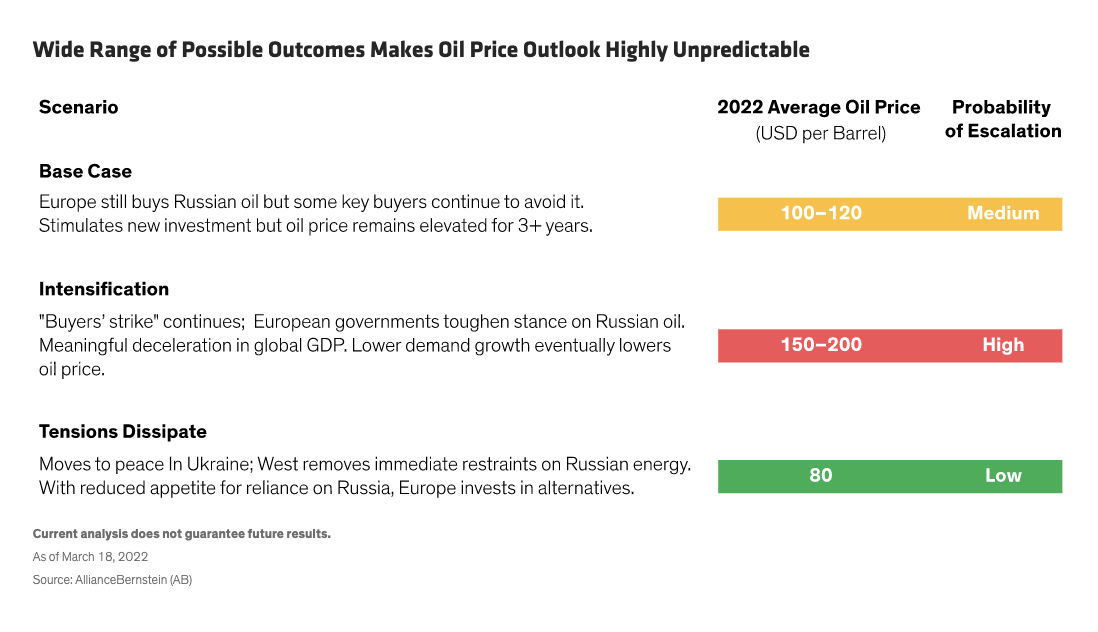

Russia’s power on the world stage is supported by its vast reserves of oil and gas.

How can investors gain confidence that an equity portfolio is invested in companies that are really helping to address climate risk? Focus on a company’s carbon handprint, which measures the positive impact, or carbon avoided, by using its products.

Dormant for many years, inflation has returned with a vengeance—fed by pandemic-related challenges and easy-money policies. Inflation may end up as a temporary condition or a longer-lasting issue, but in either case it’s top of mind for many investors today. Hear from AB experts as they tackle inflation in the inaugural edition of the Disruptor Series by AllianceBernstein.

European markets have been turbulent because of the region’s proximity to the war in Ukraine and economic links with Russia.

When I meet with a financial advisor in her office, I look around and think, “What do the displayed items tell me about you? Who or what is in the pictures, and why do they matter?”

At its March 10 meeting, the European Central Bank (ECB) surprised the market by announcing an acceleration of its tapering program—wrapping up securities purchases earlier than anticipated.

European investors are struggling to understand new rules designed to confirm the environmental, social and governance (ESG) credentials of portfolios.

When Russian president Vladimir Putin sent troops into Ukraine, he unraveled decades of efforts to cement peace in Europe after the Cold War.

What happens when you combine the tipping point of two deflationary forces—globalization and demographics—with a pandemic, epic supply-chain disruptions and an invasion in Europe? Inflation of a magnitude not seen since the 1970s. Some of the contributing factors may be transitory, but not all, and lingering inflation is likely to be higher than before. How should bond investors adapt?

Russia’s invasion of Ukraine has shocked the global economy, in particular by fueling further spikes in energy and commodity prices. The new inflationary catalysts will have differing effects on monetary policy moves because regional economies are starting from different places, which will determine their ability to withstand higher commodity prices.

More securities labeled as environmental, social and governance (ESG) bonds are being issued by a wider variety of companies than ever before.

Sustainable investment funds are mushrooming. Assets under management in Morningstar’s global sustainable fund universe surged to $2.75 trillion at December 31, 2021, nearly three times the pre-pandemic level, according to Morningstar.

Environmental, social and governance (ESG) factors are all important to the sustainability of an investment.

Given the dominance of inflation in today's capital markets discussion, it should be no surprise to anyone watching this video that one of the most common questions I get is, “How do I inflation-protect my portfolio?” And that's what we're going to focus on today: what to think about when you're thinking about inflation protection.

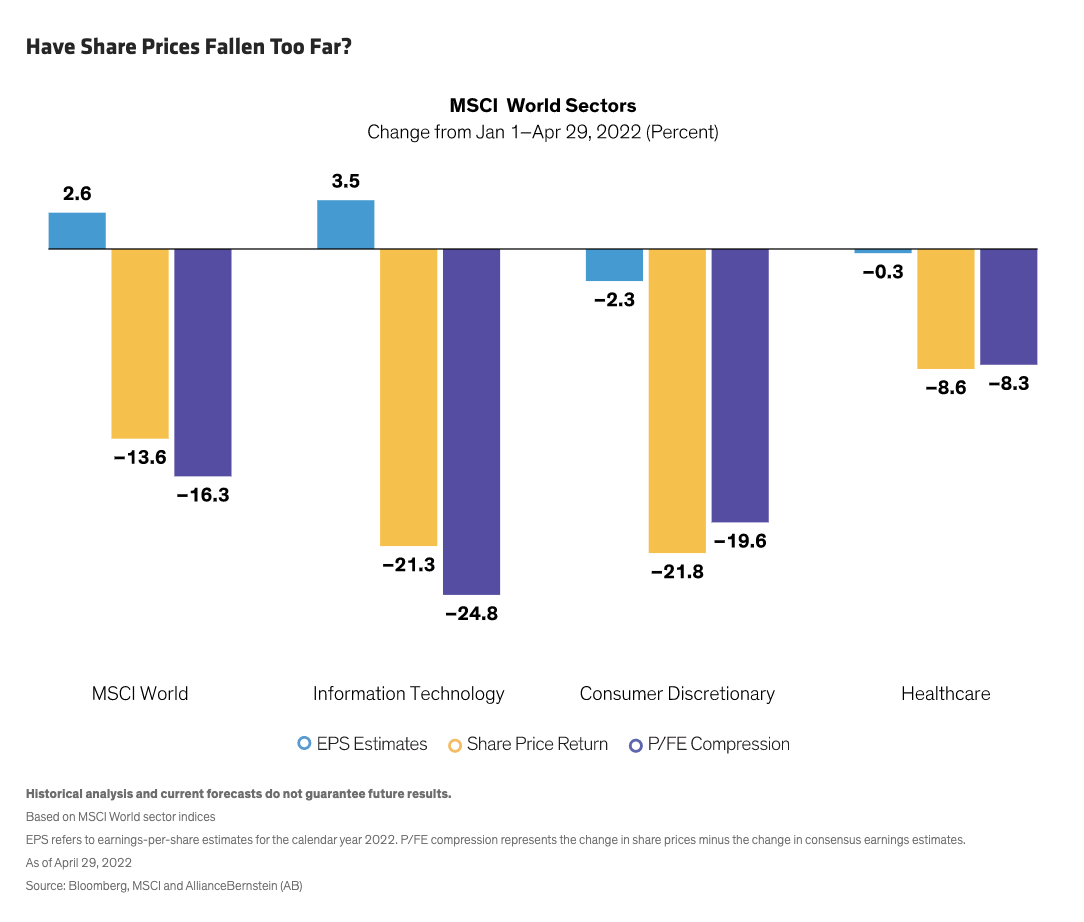

Equity markets were jolted in January amid growing concerns about macroeconomic threats.

Millennials often say their biggest challenge is being lumped into one category, as if everyone’s needs and aspirations are identical.

The prospect of rising interest rates has clouded the outlook for global bond investors in 2022, but it’s not all bad news.

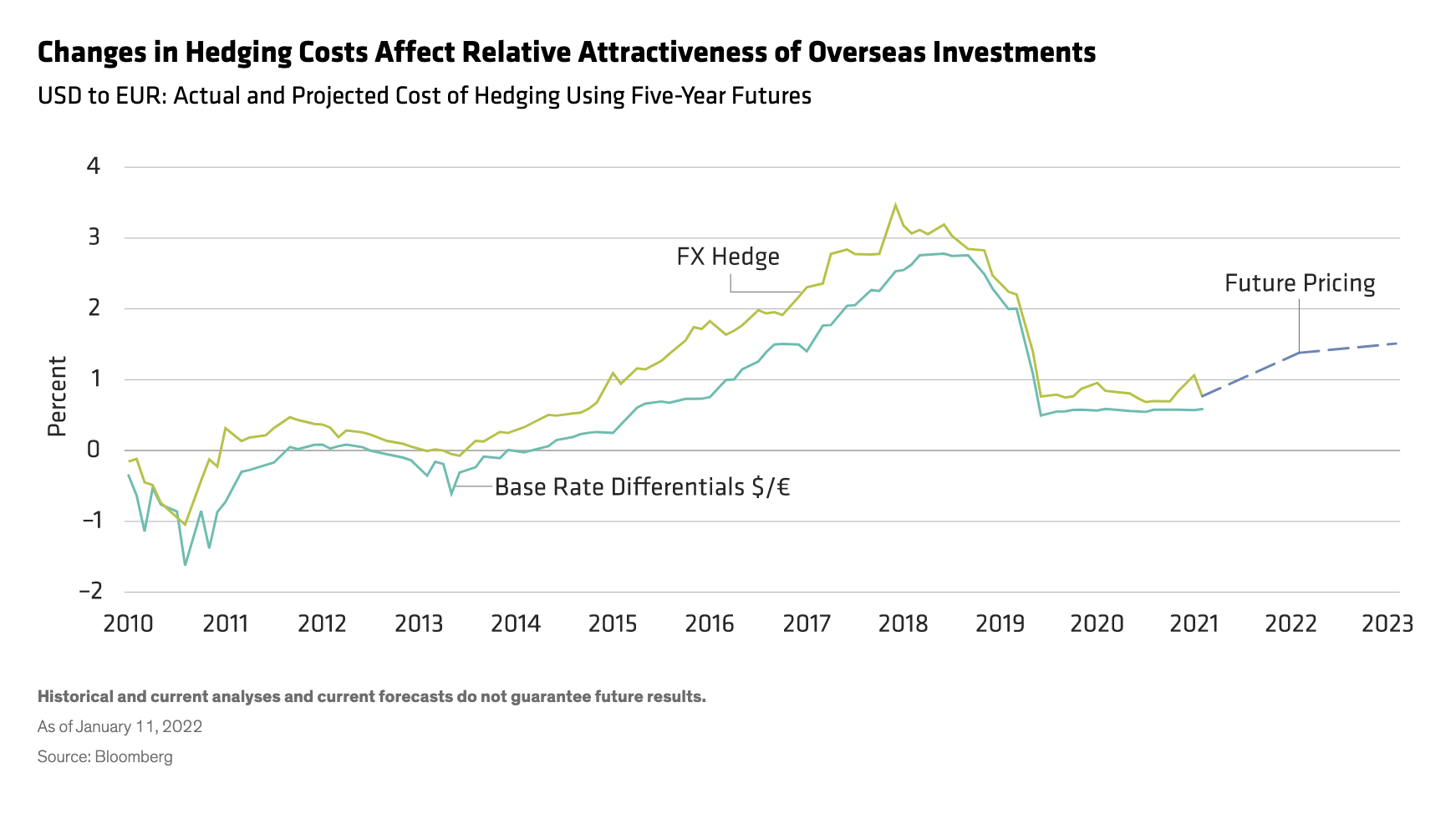

Recently, euro-based investors have been able to access higher-yielding US dollar bond markets while hedging their currency risk at low cost.

From the advent of electricity to the adoption of the internet, technology has often been a catalyst for cost reduction.

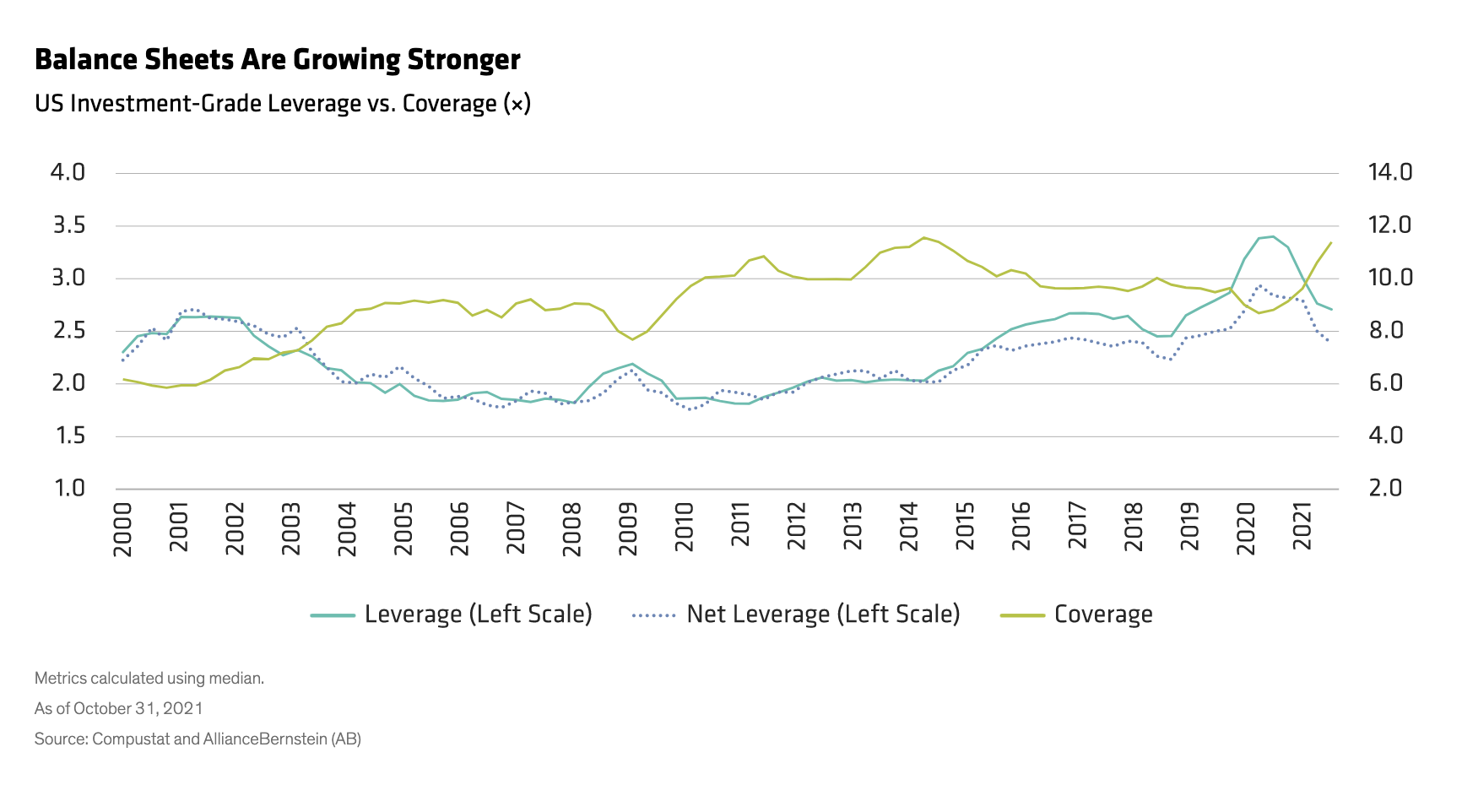

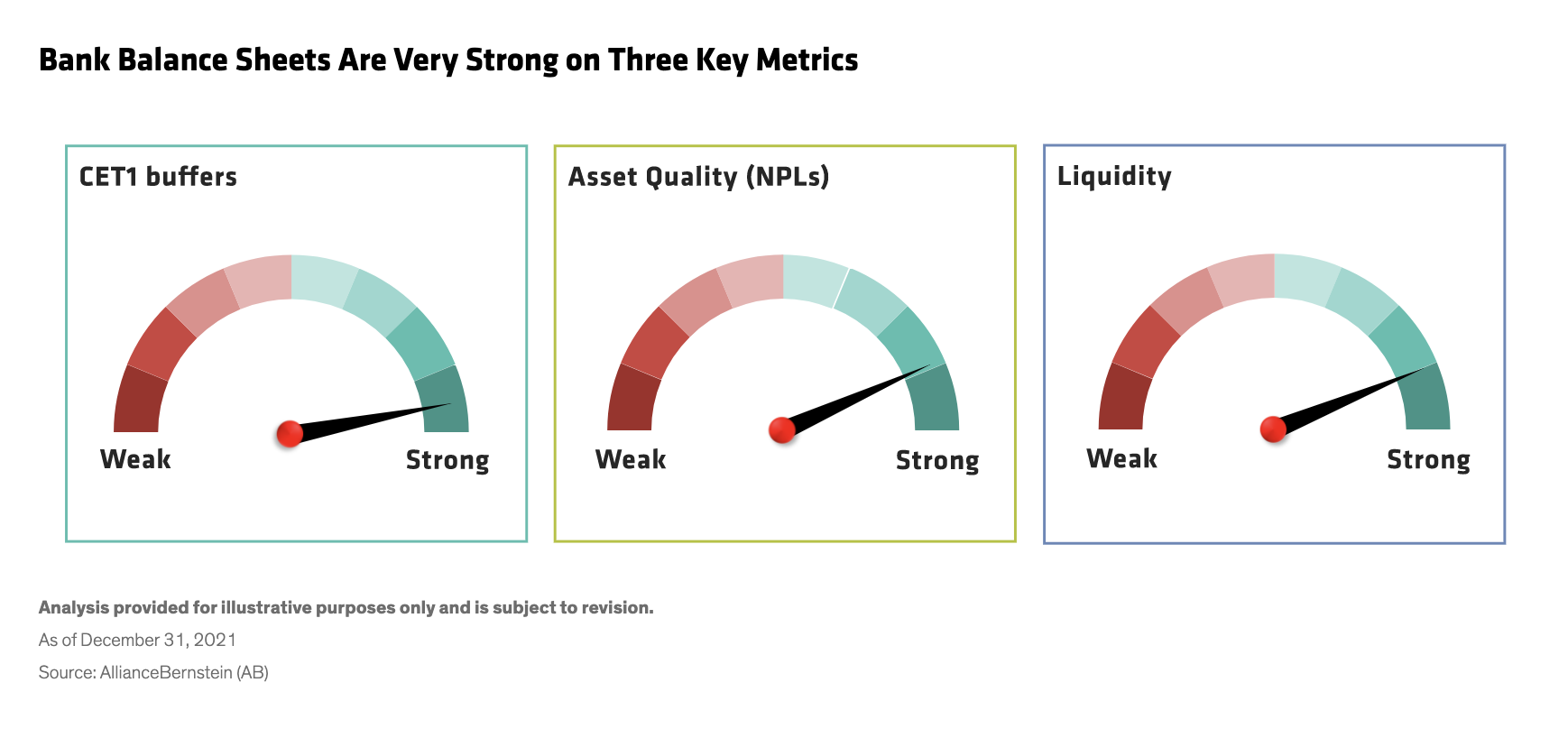

The COVID-19 pandemic looked set to batter the world’s banks—and yet banks’ balance sheets are now the strongest they’ve been since the global financial crisis (GFC).

The surge of the coronavirus omicron variant has implications not only for broader asset-class allocations but also for macro exposures within asset classes.

For China, the year ahead holds special political and economic significance.

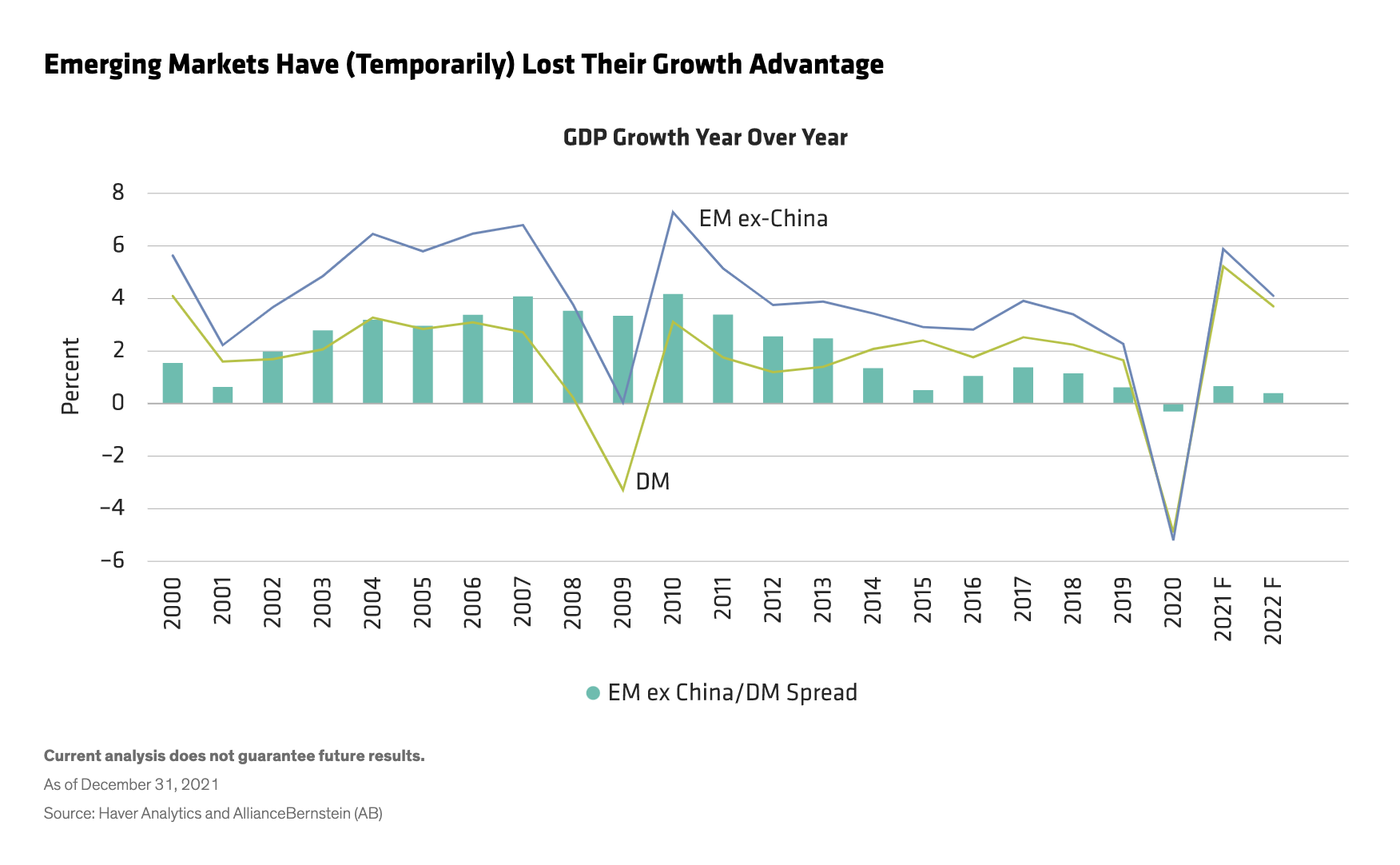

Most investors need little persuading that emerging markets offer exciting opportunities.

One of the things that we like to do is to make sure that our investments are very specific—that they have intentionality behind each investment.

As we go into 2022 and ’23, we’re going to have an economy that’s going to be quote-unquote normal.

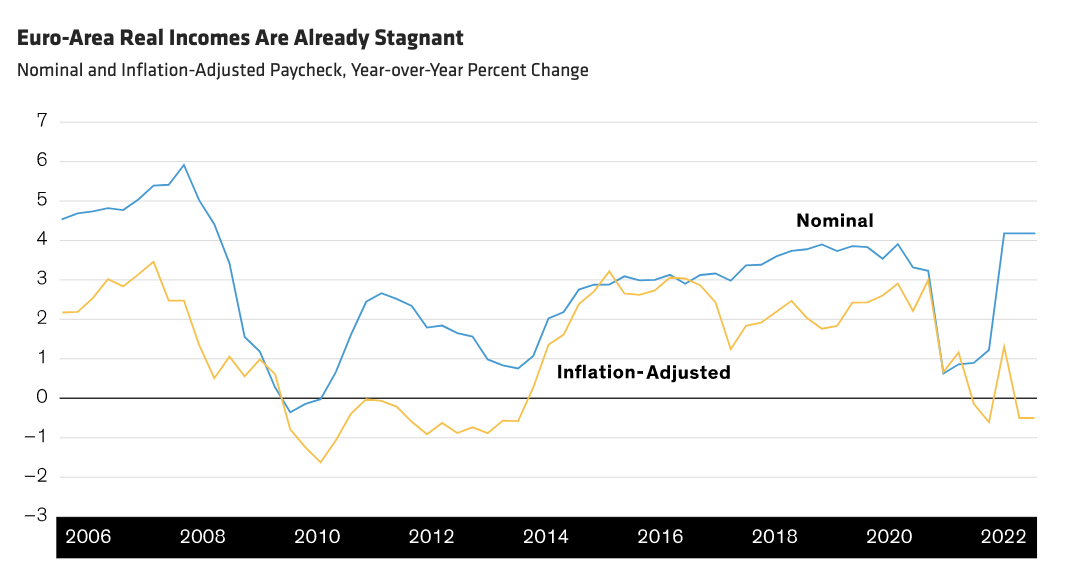

Rising inflation is troubling bond investors worldwide, but European bond markets will likely experience comparatively weaker inflation pressures and stronger central bank support.

For emerging-market debt (EMD), 2022 is shaping up to be a contest of conflicting forces.

Few investors would’ve anticipated the very strong returns we’ve seen, particularly in the US market.

Global equities surged in 2021 during a year full of surprises.

High-yield investors should actually root for rates to move higher, rather than lower. And that’s because if rates are moving higher, it means the economy is doing well and companies are generating a lot of earnings, and therefore their credit risk is actually coming down. Which is a really good thing for us as credit investors.

The Federal Reserve responded to stubborn inflation pressures in the US economy by doubling the pace at which it’s tapering its QE purchases. It also ramped up the number of rate hikes it expects will be needed to bring the economy back into equilibrium in the medium term.

The world’s central bankers have had to manage competing priorities during the COVID-19 era. Now that COVID-related threats to global economic growth look to be receding, the risks from higher inflation are becoming more prominent in their thinking.

The United Nations Glasgow Climate Change Conference, also known as COP26, concluded in November with 200 nations signing the Glasgow Climate Pact (GCP), an agreement that could accelerate climate action and drive big carbon cuts.

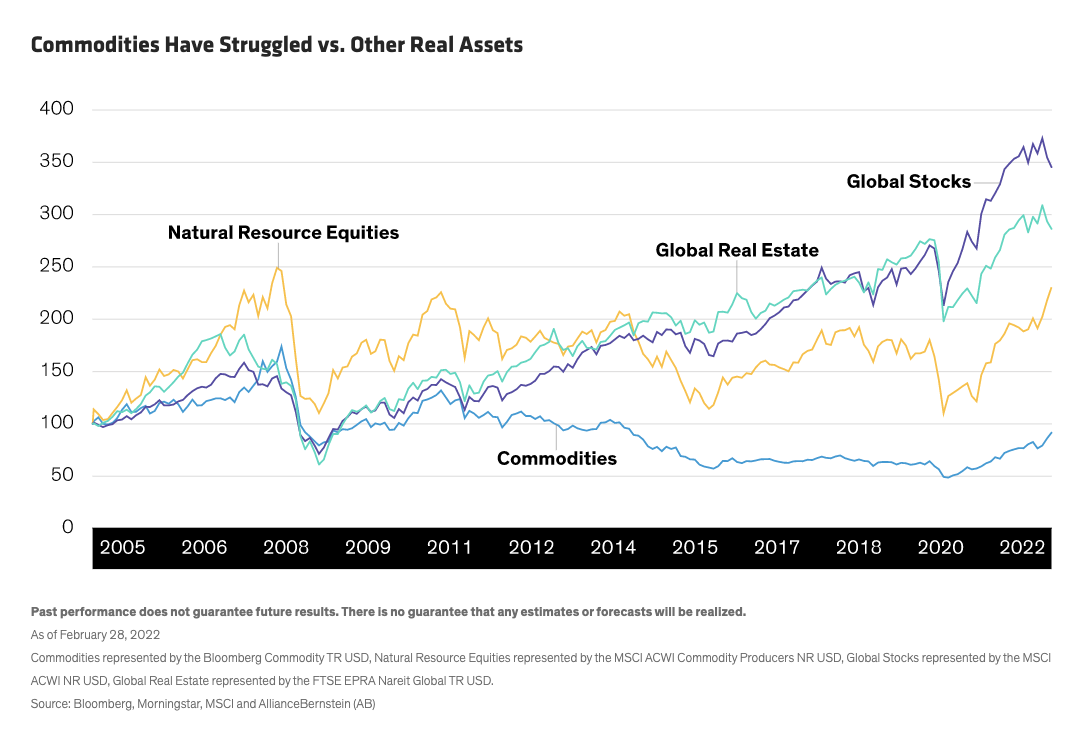

Commodities, by virtue of their fungibility and broad uses, have infiltrated nearly every facet of human life, making the world enormously reliant on their ready availability.

Real estate stocks posted a sharp recovery this year, despite disparate effects of the pandemic on different property types. Improving trends in key US market segments show how investors can gain confidence in property stocks as a diversifying source of solid long-term returns and an effective hedge against inflation.

As investors and companies increasingly seek to address the risks of climate change, there is growing debate about the use of carbon offsets in achieving net-zero emissions. We think there’s room for a measure of offsets to achieve carbon neutrality, provided best practices are followed.

So, when you think about the end of 2021, and looking forward into 2022, we’re reasonably optimistic about the backdrop. Growth should be set up pretty well for 2022.