The GameStop drama that has rattled US stocks reflects the growing power of individual investors to shape market events. But there are lessons for traditional, long-term investors, too. When markets ignore fundamentals, redoubling a focus on quality is the best way to produce consistent returns while reducing volatility.

The probability of more fiscal relief from Congress has risen—good news for the US economy and a boost to our growth forecast. While risks remain, and it’s too early to talk about the pandemic in the past tense, we’re optimistic the economy can return to more normal footing soon.

As inflows to sustainable equities break new records, here’s what investors should look for to identify portfolios that align with their responsible investing goals.

It may seem shocking, but a simple trip to the local store to pick up fresh produce or clothing could enable human exploitation. For investors, those same connections can exist within their portfolios—and it takes more than a passive effort to root them out.

As China begins the year of the Ox, many investors are wondering whether another bull run is possible in 2021. Given that last year’s rally was extremely narrow, we believe many parts of the market still offer pent-up recovery potential.

For European banks’ stockholders, 2020 was a year to forget. But bank bondholders enjoyed positive returns and may overcome COVID-19 challenges again in 2021, backed by solid balance sheets and supportive regulatory conditions.

Global stocks rebounded sharply from the coronavirus market crash in 2020, but the ride was rocky. With so many risks clouding the outlook, we believe that investors should focus on generating a smoother pattern of returns through the recovery from COVID-19.

Emerging-market stocks rebounded in 2020 even as the COVID-19 pandemic spread globally. As vaccines and other favorable conditions unfold, investors have good reasons to consider EM equities in 2021 while strategically considering their potential risks.

Municipal bond issuers’ financial health and resiliency—which helped in 2020—should support opportunities for active muni investors in 2021.

Small-cap US stocks rebounded sharply in the fourth quarter. Yet the recovery may still be in its early stages—particularly for smaller-cap value stocks—as pandemic risks recede and earnings drivers kick in during 2021.

Credit markets have staged an epic rebound from the depths of March 2020. But in a low-growth, low-yield world, we believe there may be more room to run in 2021.

Now’s the time to put the challenges of 2020 behind us and start the new year with a fresh perspective. While we can’t predict the future, we can break away from old behaviors and be intentional about our choices in the new year.

Emerging-market sovereign debt has rebounded sharply off the lows, but this hard-hit sector offers attractive yields and compelling growth opportunities to discerning investors.

The events of 2020 remind us that life is complicated and fragile and that being prepared really does matter. Could this inspire you to become a character of great significance in the lives of your clients because of how you comfort, lead and inspire them?

Recent SOE bond defaults signal Beijing’s willingness to let markets price risk more accurately.

Income-seeking investors have been frustrated in recent years as US dividend-paying stocks underperformed. But companies that offer strong payouts in a sustainable manner can help investors source surprisingly robust streams of income and equity returns.

Low interest rates and massive stimulus-fueled debt raise investor concerns about potential long-term fallout. But when the cost of capital is this low, it revs up funding for innovation that ultimately fills the pipeline with robust opportunities, especially in technology.

With a greater level of clarity than we’ve had since the COVID-19 pandemic, we’re getting a better sense of how the US economy might shape up over the next few months, into 2022 and beyond. We see three distinct stages over that time frame.

After a difficult winter, we expect the global economy to rebound strongly next year. But structural headwinds remain. Will the post-pandemic bounce trigger a durable and broad-based global reflation?

Healthcare stocks are once again in focus as a result of promising news of COVID-19 vaccines. But investors shouldn’t hunt for the pandemic’s panacea. Focusing on business fundamentals is a much better way to find healthcare stocks with long-term potential than searching for the next big drug.

Global investors have been watching US President-Elect Joe Biden closely for clues as to how his administration intends to conduct relations with China.

Despite lingering uncertainty about corporate earnings growth and economies around the world, global stocks have rebounded from the COVID-19-driven downfall in March. But even following that bounce back, international stocks have lagged their US counterpoints for over the last decade. Could they be reaching an important inflection point? If so, how are astute investors casting a broader net to pinpoint the right companies outside the US?

Join us to hear from an interactive panel of investment experts from AllianceBernstein, who will cover:

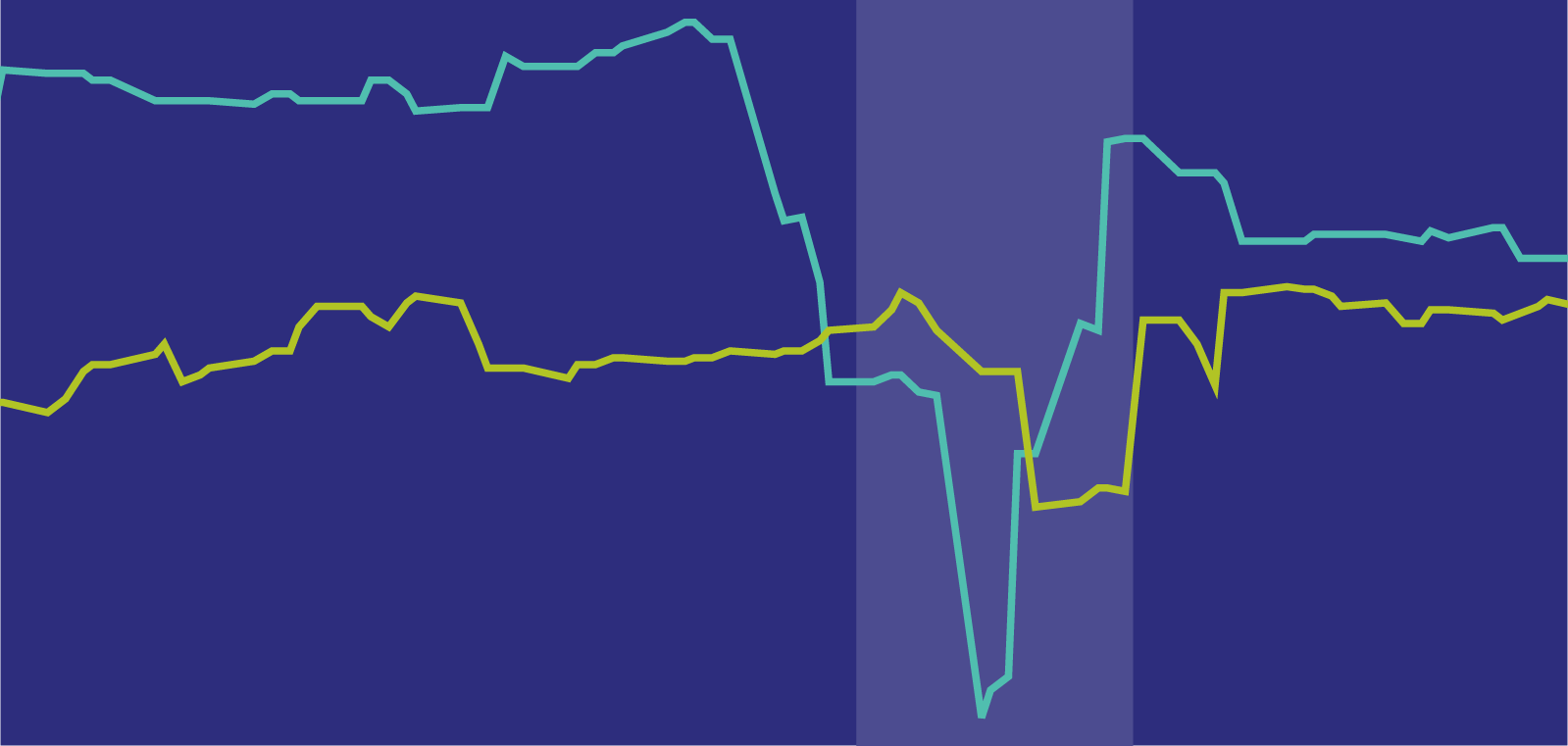

As investors look for signs of a return to normalcy from the coronavirus crisis, they have a dizzying array of indicators to choose from. We’ve assembled a group of signals, with the help of big data, that may point the way.

Two recent developments could have big implications for the US economic outlook: general elections and news of very promising progress on a COVID-19 vaccine. To understand the ramifications, we have to distinguish near term from longer term.

States face revenue shortfalls from COVID-19 costs and shutdowns. We look under the hood to assess how some of the most indebted states are faring.

Defensive equities are usually found in sectors that have withstood market shocks, such as utilities and real estate. But as COVID-19 shakes up investment conventions, companies with intangible assets are being more appreciated for their volatility cushion.

A fresh round of lockdowns means a difficult winter lies ahead for the euro area. But three factors caution against excessive pessimism.

The roller-coaster ride of 2020 still has a few twists and turns to navigate. But the massive policy response to the COVID-19 pandemic brought a quick, though incomplete, recovery. With volatility expected to continue, where can investors look for opportunities?

There have been plenty of headlines exploring what the November US elections might mean for the economy and markets. But it’s just as important to look at what they might have in store for defined contribution (DC) and other retirement vehicles, which more Americans than ever rely on.

Why is it hard to get clients to take preventative action to protect themselves from real and measurable risks?

As Prime Minister Suga begins his administration, the message is one of continuity, but Abenomics may need a reboot after COVID-19. We examine what Suganomics may mean for Japan.

Emerging-market debt has rebounded sharply off March lows, but attractive yields and compelling opportunities persist. We provide a roadmap for what may lie ahead.

Even if this US election has a bigger impact on markets than in the past, we would advise against building an investing strategy based on a potential political outcome for several reasons.

Euro-area countries were struggling to achieve growth and inflation even before the coronavirus pandemic. Now global lockdowns and trade disputes have compounded their problems. Still, we believe euro fixed-income markets offer active investors attractive opportunities and worthwhile income.

Investors should consider many angles when evaluating what active managers can offer through a global crisis and an indefinite period of uncertainty.

Escalating trade tensions between the US and China could affect Chinese corporate bonds, but not all credits are vulnerable.

It seems like ages ago that our firms closed their doors and we scrambled to set up home offices. We weren’t sure what challenges lay ahead, and the market took our breath away in those first intense weeks. But while we don’t like having to cope with a disaster, human beings tend to do well in a crisis and to adapt quickly to massive disruptions.

US third quarter GDP was better than expected, though our updated economic forecasts still show a quick but incomplete recovery. Over time, this should give way to a more gradual, lengthy path back to “normal.” But there are a lot of moving parts.

European equity markets are still struggling to overcome the effects of the pandemic. But diligent investors can find surprising investment candidates.

Can bonds continue to play defense and provide income when yields are at historic lows? We think so.

Equity markets advanced in the third quarter but pulled back during September. Market moves were dominated by a small group of giant US stocks. How should investors react?

Investing in businesses that strive for a better climate through decarbonization doesn’t necessarily assume a lower bar for performance. Just the opposite. Besides contributing to a healthier environment, low-carbon equity investing can also offer attractive return potential.

Guiding Defined Contribution (DC) plans through economic cycles is challenging enough without harsh headwinds from a global health crisis. But more plan sponsors are getting invaluable expert help to navigate through current challenges while keeping a long-term perspective.

What will a Trump or Biden win mean for munis? From taxes to infrastructure, the candidates differ—sometimes dramatically—on policy.

Recent history suggests that low—and even negative—yields don’t eliminate the offset to risk assets provided by government bonds.

Videoconferencing is becoming routine, mundane and overused. Here are tips for looking and sounding your best on a video call so that your audience stays engaged and you can rock that call.

Investors don’t often pay much attention to corporate culture. But cultural norms can make the difference between success and failure, especially for growth companies.

Investors are eager to buy bonds that help create a better, more sustainable world. Here’s how to navigate the evolving landscape.

Global stock markets seem to be defying the reality of recessions this year. Despite recent volatility, we think market gains for the year are more rational than perceived, given the powerful impact of stimulus and low rates on stock valuations.

The Brexit negotiations are growing more adversarial with no signs of agreement on key issues. The most likely outcomes are now the hardest and most disruptive Brexit scenarios—leading to further potential weakness for the UK’s currency.