Despite rising global yields and renewed inflation concerns, equities moved higher in May on the back of a strong US earnings season and continued momentum in AI-related stocks. The tech-heavy Nasdaq Composite gained 8.4% for the month, while the S&P 500 rose 5.3% and the Dow Jones Industrial Average was up 2.9%.

Despite lingering geopolitical tensions, higher oil prices, and renewed inflation concerns, equities moved higher in April, supported by a strong start to the Q1 earnings season and resilient economic growth.

Despite early volatility driven by global bond market stress, tariff-related tensions, renewed inflation concerns, and uncertainty surrounding Federal Reserve leadership, equities finished January higher, with the S&P 500 reaching new all-time highs.

Many may look at a headline performance figure like “the bond market is up 7%” and understandably feel encouraged. On paper, that appears to be a solid result. But nominal returns alone rarely tell the full story.

Despite ongoing tariff uncertainties and hawkish post FOMC meeting commentary towards the end of the month, US equities extended their rally into July amid resilient Q2 earnings, progress on trade negotiations, and improving consumer sentiment.

When the Fed increased the M2 money supply by over 40% during the COVID crisis, our instinct was that the implications would extend far beyond a temporary boost to the U.S. stock market and higher inflation. That intuition is proving accurate. We’re now seeing the long-term ripple effects play out in real time across multiple asset classes and global markets.

Despite inflation worries, fiscal deficit concerns, and continued geopolitical conflict, equity markets posted strong returns in May on the back of easing tariff tensions, lower probability of recession, and better than expected US Q1 earnings.

US markets struggled in the first half of April due to tariff-related worries. The second half saw rallies amid policy reversal.

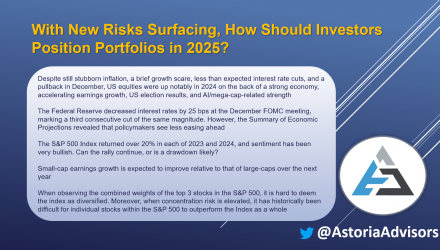

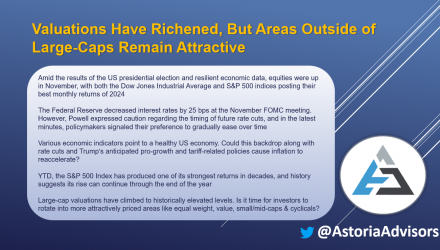

US equities were up notably in 2024, due to a strong economy, accelerating earnings growth, US election results, and AI/mega-cap strength.

There are not many attractive opportunities in the US large-cap space. History suggests the market is overdue for a correction.

Astoria rounds up its 10 ETFs for 2025, providing unique thought leadership and actionable investment ideas.

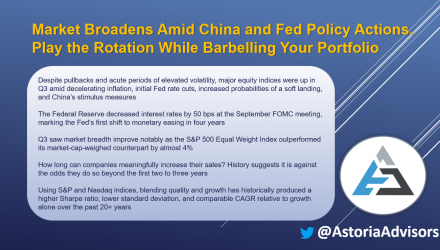

Market participation broadened beyond technology stocks during the third quarter.

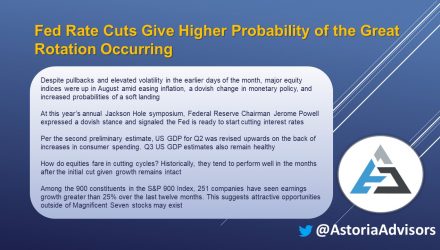

Despite pullbacks and elevated volatility in the earlier days of the month, major equity indices were up in August.

This isn't the time in the cycle to take excessive risk. The easy money has already been made. Astoria's 2019 playbook is as follows: late cycle economic forces + desynchronized global growth + a deteriorating earnings cycle = the need for more defensive posturing across stocks and bonds.