Begin with the print itself, because the headline flatters the internals only slightly. The bulk of May's gains came from leisure and hospitality, which added 70,000 jobs, nearly half of them in food services and drinking places; local government contributed 55,000, health care 35,000, and manufacturing a modest 7,000, while financial activities actually shed positions.

For the dollar-denominated investor weighing how to position for the back half of 2026, last week tightened a thesis we have been building all year.

On the surface, last week looked engineered to embarrass our positioning. The dollar index climbed to a six-week high above 99.3 by Friday and finished the week roughly flat at those levels.

Our reading is that this is a meaningful positive at the surface — a real-time confirmation that the most pessimistic recession scripts written in March can be set aside — but it is also a print that fails to alter the structural calculus we have been describing all year. The labor market is steady. The trajectory of fiscal policy, monetary credibility, and dollar reserve status is not.

The S&P 500 closed Wednesday at a fresh all-time high of 7,022.95, surpassing the late-January peak and capping a remarkable round trip from the spring selloff.

Gold has fallen roughly 21 percent from its all-time high of nearly $5,595 reached in late January to approximately $4,430 as of this writing, and the prevailing narrative in markets is that this correction reflects a genuine shift in the metal’s outlook

This week’s economic releases have once again underscored the policy dynamics we outlined in our January outlook. President Trump faces a high-stakes midterm election in November, and the incentives are clear: deliver visible growth, moderating inflation, and lower borrowing costs to strengthen the administration’s hand with voters.

The key point, in our view, is that this combination of shocks is not likely to be an isolated occurrence in 2026 or beyond.

The Federal Reserve’s September meeting may be remembered less for the modest quarter-point cut it delivered and more for what it revealed about the state of the institution itself.

The late-summer calm in financial markets shows an undercurrent of optimism. Stocks have been on a tear, with the S&P 500 rebounding strongly to notch roughly 18% gains for the year, while overseas equities are up even more.

This past week, we saw a sweeping change in U.S. trade policy come into effect with the termination of the long-standing “de minimis” exemption on small, imported parcels.

The June Consumer Price Index (CPI) report offers clear confirmation that inflation is quietly reasserting itself.

As we move into the second half of 2025, it is an opportune moment to reassess our market outlook and provide updated insights for investors.

The January Employment Situation Report reaffirmed the resilience of the U.S. labor market, with nonfarm payrolls rising by 143,000 and the unemployment rate ticking down to 4.0%.

As we step into 2025, it’s time to revisit our expectations for the markets and provide an updated perspective for investors.

The December PMI report, released on January 5, 2025, indicates that the U.S. services sector continued to grow, albeit at a measured pace, suggesting resilience in certain areas of the economy.

The Federal Reserve’s recent meeting signaled a notable shift in its monetary policy approach.

Here’s our outlook on what to expect and how investors might navigate this new phase.

The latest Employment Situation Report released on October 4, 2024, showed nonfarm payrolls increasing by 254,000 in September, with the unemployment rate holding steady at 4.1%.

On September 18, 2024, the Federal Reserve cut interest rates by 0.5%, bringing the federal funds rate down to a range of 4.75% to 5%. This move, aimed at managing inflationary pressures while addressing the gradual rise in unemployment, underscores the Fed’s balancing act between fostering economic growth and taming inflation.

As we approach the end of 2024, the latest Consumer Price Index (CPI) report from the Bureau of Labor Statistics (BLS) has provided us with critical insights into the health of the U.S. economy, particularly concerning inflation.

The current economic landscape is fraught with uncertainty, and the potential for higher inflation continues to pose a real threat to market stability.

Recent developments in the labor market triggered the Sahm Rule, an economic indicator known for predicting the onset of recessions. Developed by economist Claudia Sahm, it signals a recession when the 3-month average of the unemployment rate rises by at least 0.5 percentage points above its low from the previous 12 months.

On July 31, the U.S. Treasury released its most recent Quarterly Refunding Announcement which revealed its financing strategy, presenting both positive and restrictive elements for global liquidity.

As we approach the end of the fiscal year, investors should be focusing on the Treasury General Account as one factor of many that may impact global liquidity, and in turn, market performance in the coming two quarters.

The latest Consumer Price Index (CPI) release has brought some much-needed respite, indicating a slowdown in inflation. Yet, underlying economic conditions suggest that this reprieve may be temporary, with potential for inflationary pressures to reassert themselves in the coming months.

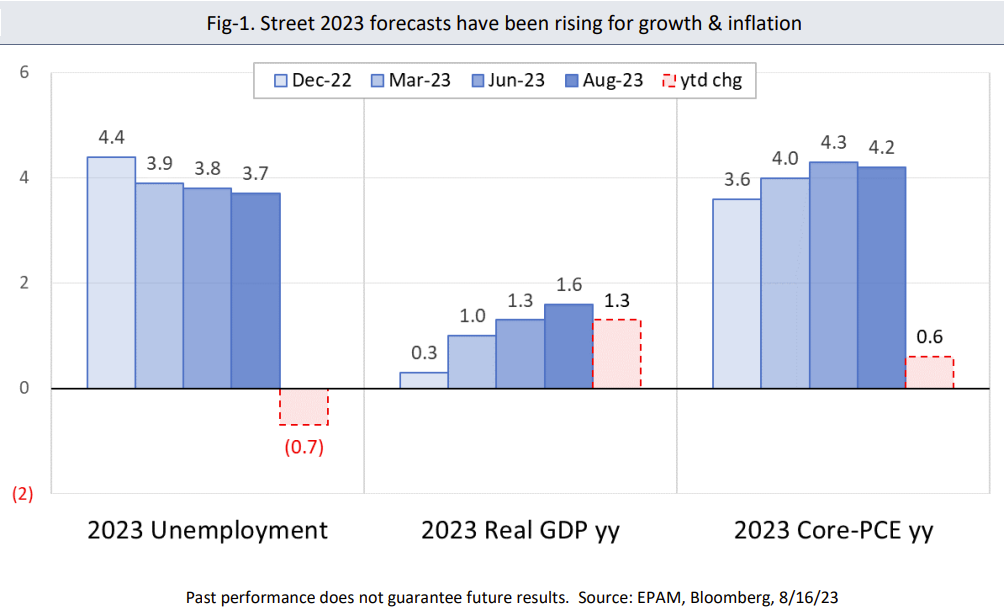

Interest rates are at 20-yr highs, yet unemployment is at 50-yr lows, core-PCE is near 30-yr highs, and Wall Street (and Fed) economic forecasts continue improving. What explains the disconnect between these unexpected outcomes and those expected by mainstream economic textbooks?

An audacious communications campaign from Democrats in Washington is currently underway that is attempting to convince the public that there is no recession, inflation has been vanquished, even if inflation is still alive, targeted new Federal legislation will kill it.

Our weekly commentaries provide Euro Pacific Capital's latest thinking on developments in the global marketplace.

There was a little March Madness on Wall Street.

2021 is now in the rear-view mirror and I believe that future financial historians may regard it as the year of peak speculation.

The inflation that we were emphatically told would be transitory and unmoored continues to persist and entrench. As the troubles gather momentum Washington is doing...

In the 50 years since Richard Nixon officially severed the dollar’s link to gold, many have claimed that the greenback’s strength rests primarily on America’s unchallenged power and prestige around the world.

The “transitory” inflation swamping the country has stubbornly persisted into July.

What exactly is “transitory?”

It’s dawning on many investors that our post-Covid financial problems may not be as easily solved as Washington claims.

Recently, a piece of collage art entitled “Everydays: The First 5000 Days,” by an artist known as Beeple, sold at a Christie’s auction for $69 million.

The rationale behind the meteoric rise of Gamestop, a chain of videogame rental stores, and AMC, one of the nation’s largest cinema operators, is too unlikely to be believed. In just one month both stocks had risen by more than 600%.

While most people generally understand that the stock market and the economy do not move in lock step, there is still an underlying belief that a strong market reflects a strong economy. But according to that logic, our current economy must be historically strong.

For years I have been warning that during the age of permanent stimulus (which began in earnest with the Federal Reserve’s reaction to the dotcom crash of 2000), each successive economic contraction would have to be met with ever larger, increasingly ineffective, doses of monetary and fiscal stimulus to keep the economy from spiraling into depression.

While the country and the stock markets reel from the impact of the Coronavirus, many economists and politicians are calling for the government to fight the pandemic as if we had to fight the Second World War all over again.

With the markets shell shocked by of the worst weeks on record, analysts are split on whether investors are simply overreacting to the coronavirus epidemic or if we are confronting an actual existential threat to the global economy.

In the decades that I have been listening to politicians clumsily trying to explain the economy there has never been a period, with the possible exception of the early Reagan years, in which major party leaders were able to present a solid grasp of economic principles.

Like particles in a super collider, opposing forces of American culture smashed together this past weekend on a historic football field in Connecticut. And like a physics experiment, the resulting impact shed light on the state of the country and provides us all with a ready framed discussion for the Thanksgiving weekend.

Early last week, the Chairman announced a new, as yet unnamed, Fed program through which the bank will now buy regular amounts of short-term U.S. government debt. Seeking to counter the rumblings that a new form of quantitative easing would be seen as an admission that the economy may be in trouble...

A dollar in secular decline may be the final piece in the puzzle that shows the insanity of our current fiscal and monetary policy. The U.S. bubble economy rests on the foundation of the dollar's status as the reserve currency. If that status is lost, the entire house of cards may just come crashing down.

After claiming to be the greatest at just about everything, Donald Trump has finally found an area where he can stake a credible claim. By negotiating a disastrous budget deal with Democrats, the President could become the greatest creator of government debt in the history of the country.

While the willingness to abandon long held beliefs for political gain has always been a common trait among public figures, the spectacle has recently taken on shocking levels of casual audacity.

While many savvy economists should have seen this coming, as late as October of last year, almost no one in the financial world thought that the Fed would so easily abandon its long-held bias without a gale force recession blowing them off course. But, in reality, all it took was a light breeze to force a 180-degree turnaround.

General George Custer met his doom charging into a battle he thought he could win, against an opponent he did not understand. Based on his views about the fast-emerging trade war with China, it looks to me that Donald Trump, is charging into an economic version of the Little Bighorn.