Today’s stock market looks like the love affair between Danny and Sandy at Rydell High. Sandy is “hopelessly devoted” to Danny, even though he is the leader of a Los Angeles high school gang.

Warren Buffett’s annual letter was great in all the easy ways and disappointing in the ways that matter the most to his shareholder partners

We think this is an excellent time to ponder the thoughts of Buffett and Munger.

The object of the game was to get to the finish line first and then become the leader the next round. The stock market has its own game of “Simon says” and that is in the mall property world.

Fortunately, human behavior has a history of repeating itself at extremes. The worst buying decisions are made at the top. Just like bonds, the convexity is true when yields rise going forward. It’s a slippery slope and could be vexing.

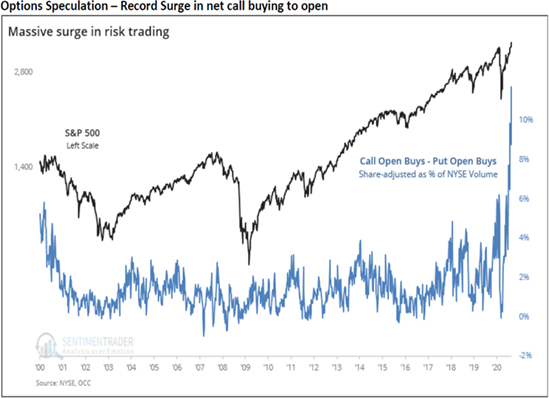

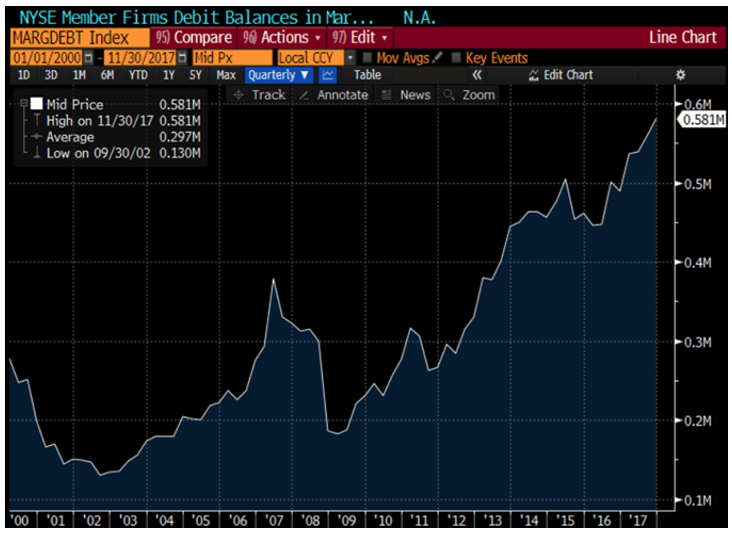

We have enjoyed watching what happens in the late stage of a financial euphoria episode play out in the escapades of millennial investors on Reddit, who seem to “rule the nation.” While politicians, regulators, the media and others try to sort this out, we thought some historical perspective might be helpful.

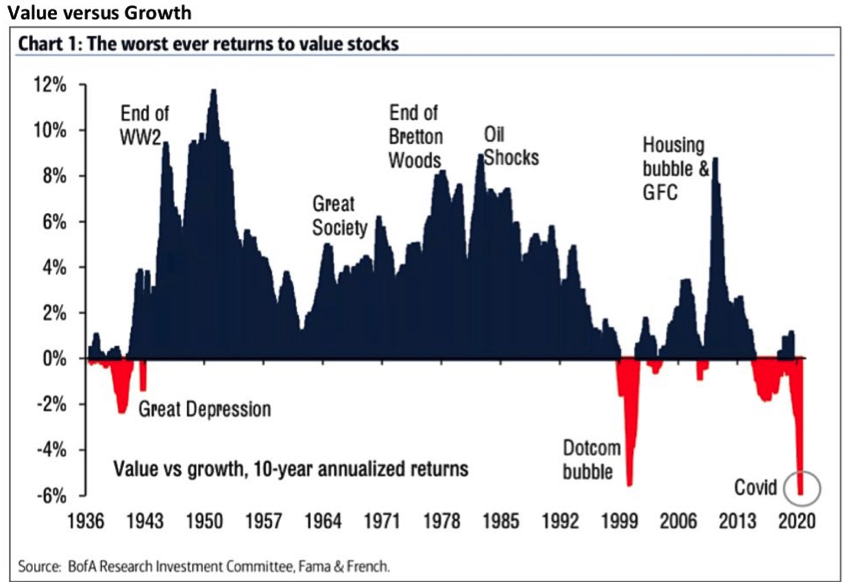

There have been a small number of consistent alpha-creating axioms in the U.S. stock market over time. Value beat growth over long time frames, tech stocks hit bottom in the summer and crowded trades separate you from your money, to name a few.

Our outlook for 2021 is formed by the need to get away from the crowd and to expect some very stormy weather in the U.S. stock market. We are not afraid of drowning. Therefore, we will review the circumstances at the bottom of the market in 2009 with today’s market to see where the crowd is and where we need to go to avoid the coming storm.

As we begin 2021, the investing public is tied up in a “frenzy,” to quote Charlie Munger from a recent interview. This “frenzy” can be captured a couple ways.

As we enter 2021, it appears that Buffett had things upside down in 2020. The things which had gone up the most by the end of 2019, went up the most in 2020.

We were fortunate to watch a recent interview Charlie Munger did with Cal Tech as a distinguished alum. We consider him to be one of the most successful contrarian investment thinkers on the planet. At 96 years of age, he has no fear of being politically incorrect. We contrast this with the mountain of writing, media and rhetoric associated with the topic of climate change.

There appears to be a few huge statistical bargains available in the stock market based on the simplified version of Benjamin Graham’s intrinsic value calculation.

My wife brought me a box of ornaments that my mother has given to us over the years. I decided to check what I could sell them for on eBay (EBAY). What a great way to look at what is going on in equity capital markets!

In all this tech euphoria and COVID-19 quarantining, investors are missing a key fact. People need people.

As Buffett said, this looks like “one helluva party” with the individual investors, professional investors and insiders all joining in the fun. As a former fraternity member in college, the best parties were always when you couldn’t find anyone missing. It wreaks of that today in the stock market.

We came up with a theory many years ago to address how important psychology is to owning common stocks. We found that the risks go up in a stock market, or in an individual stock, when a “well-known fact” (WKF) was acted on in the extreme.

When you run an equity portfolio which is concentrated in 25-30 common stock selections, there are usually three stocks which stick out as particularly attractive at any given time.

Our experience tells us that we have hope from the indignity and humiliation of the present circumstances.

David Dreman’s book, Contrarian Investment Strategies, was gospel to investors when it was first published in 1979. Investors had been decimated by markets going nowhere over the prior 10 years. Stock investors were ready for something new. Dreman had produced a lot of success as an investor and wanted to share his gospel of contrarian value investing.

We recently read Peter Doran’s book, Breaking Rockefeller, which is a fabulous economic history of the world from 1840-1920 and focuses on how the monopoly created by John D. Rockefeller was broken from 1890-1910. We also watched a documentary called, “The Social Dilemma,” which explains, through the eyes of some of the social media creators, how incredibly damaging the monopolies, created by internet technology, are to society.

Anyone who owns U.S. large cap stocks must understand what can happen from the actions of the government to enforce the laws on the books for antitrust. Contrary to popular opinion, these laws are not set up to primarily protect consumers from being gouged on price by someone with a monopoly.

We became extremely bearish on energy in 2011. At the time, we saw interest in Seattle for hybrid and electric cars. This convinced us that 10% of the cars on the road nationwide might be hybrid and electric by 2020.

I got very excited when I came across an excerpt from Jordan Ellenberg’s book, How Not to Be Wrong. His book was written to teach readers how much logic and common sense is provided by math. He tells the story of Abraham Wald during World War II, who worked for the Statistical Research Group (SRG).

An interesting contrast was drawn on September 15, 2020 between Lennar’s (LEN) earnings call and statistics on revenue per employee at Apple Corporation (AAPL). Lennar described strong growth out into the future in a measured way, because they believe that the prior decade created a home supply deficit due to underbuilding.

We hear numerous market strategists talk about stocks which are going up because “there is no alternative” to owning them. In the Wall Street vernacular, this goes by the phrase TINA.

While listening to Rob Arnott on a recent Morningstar podcast, I became enamored with something that Arnott was emphatic about. He pointed out that the structural advantage of being a contrarian isn’t being smarter. Every winning purchase in the stock market comes as an opportunity cost to the seller.

Since the inflation cocktail is closely related to value stock outperformance, we are very excited about our future value investing possibilities.

Due to the pandemic, there is a sense of permanence on Wall Street to what has transpired. This permanence focuses on the changes that we have seen in the recent five months in our daily lives. These changes include shopping online versus shopping in-person, getting takeout versus sitting in a restaurant and working from home instead of talking sports around the water cooler with our colleagues.

In the time since COVID-19 hit the economy and stock market, there has been three phases. First, the question was ‘when’ will the economy return to pre-COVID normal? Next came ‘sooner or later’? Recently, we have moved to ‘will the economy ever come back’? For long-duration investors like us, what are the investment implications in where we are now in a U.S. stock market with many securities priced for ‘never’?

When you are in a financial euphoria episode, like the one we are in currently, it is hard to visualize the impact it has when it breaks. Historically, it is the leading cause of stock market failure. We thought it would be helpful to discuss the secondary impact of the euphoria on common stocks.

The stock market is a big place with thousands of investments that you can make as an investor. It’s a frustrating place. There is a myriad of investing disciplines that you can seek out. As a millennial, my generation is learning this for the first time. Don’t kid yourself for one second: they will destroy wealth.

Everyone who owned common stocks in the U.S. went through hell in the first quarter of this year. The 36% decline in the S&P 500 Index in February and March was the fastest 36% decline of my lifetime. This hell was especially damaging to those of us who have a positive view of the U.S. economy over the next ten years.

The nice thing about being the boy who cried wolf is that you look stupid before you are proven correct and you look smart when you are right, but nobody believes you until it is too late.

With markets extremely difficult and volatile as we work through COVID-19, we thought it would be good to review important parts of our investment discipline. One way to do that is to consider stocks we found via our eight criteria for stock selection and did not keep long enough to get to their ultimate rewards.

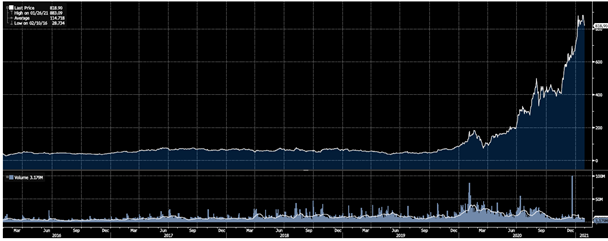

On June 4, 2020, eBay (EBAY) released a business update to make investors aware that the quarantine circumstances have caused their business to perform “significantly better than expectations,” compared to their earnings report on April 29, 2020.

The oddity of today’s stock market is exactly what any God-fearing value manager should pray for. There are very few scenarios in the last 50 years that can be used to model or forecast what is currently going on.

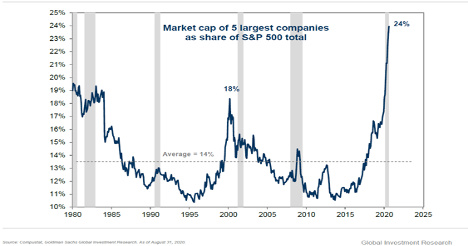

A series of charts and historical evidence exists in late May of 2020 which shows that the S&P 500 Index and the vast majority of institutional investors of all shapes and forms have concentrated their investments in the most popular stocks in the stock market.

Great investment opportunities are lonely. History shows us the crowd behaviors to avoid and the investment market circumstances to capitalize on. We believe we are at one of the great junctures, where the crowd thinks they unequivocally know the future.

We are big fans of Buffett’s theories about businesses with low capital requirements and the ability to throw off cash to owners. Unfortunately, he recently emphasized indexing and didn’t shy folks away from today’s glamour tech stocks which require more and more capital

Late last year, there were three people that we observed as optimistic about the prospects of the oil business. These people were Warren Buffett, Sam Zell and Peter Lynch. In revisiting their comments before and after the shutdown of the economy, we can see that two of the three have significantly altered their opinion.

Warren Buffett has been arguably the best asset allocator and value stock picker of the last 60 years. We are normally thrilled to sit in his classroom. Quite frankly, we were baffled by the Berkshire Hathaway Annual Meeting held on Saturday in Omaha.

The capital markets are a highly complex system, where perturbations can cause a tidal change. Every business around the world has been affected by Covid-19. For a profitable business anywhere, this is a calamity. For a business that was losing money before this, it’s a tombstone.

You have to love The Wall Street Journal writer, Jason Zweig. His extremely inciteful “Intelligent Investor” column could be called “Jason’s Wet Blanket,” because he seems to throw a wet blanket on most investment disciplines in U.S. stocks. This week’s wet blanket is designed to create even more desperation for value investors via his interview with Charlie Munger.

This smashing of economic hopes, right before one of our brightest demographic phases, could be a bonanza which only those of us who are willing to look foolish can acquire.

The year after I graduated from college, the movie Animal House debuted in 1981. With everything falling apart for the Delta fraternity, including grades and double-triple probation, all looked lost. At the point when others would give up, senior fraternity member, John Blutarsky, gave a spirited call to arms by reminding everyone that the U.S. didn’t give up when our Naval operations at Pearl Harbor were bombed on December 7, 1941.

This year feels so much like late in 1981, late in 1999 and late in 2008 to us. The first reaction by investors was to flush whatever they had left in economically sensitive stocks. Then, as if there hadn’t been enough torture for value investors today, Saudi Arabia decided to chop the knees out from under the oil industry in the U.S.

Investors have been awoken to the carnage of the last three weeks. These circumstances, while unenjoyable, may be hiding the actual problems with today’s market. The unforeseen circumstances of today are no different than the past.

Those of you who have been with us recently know that we are calling the recent decline in value stocks a capitulation in a value investing depression. The coronavirus has sucked all the economic optimism out of a market which has hugged tightly to large growth companies providing reliable sales or earnings momentum.

To us, Warren Buffett is the greatest value investor of our time. He wrote the annual letter to his Berkshire Hathaway (BRK.B) shareholders on February 22, 2020. This letter happens to coincide with some of his worst relative performance in the last year to five years.

A truly interesting contradiction is developing in stock markets around the world. A number of major corporate executives are calling for businesses to be judged by something other than the net present value of their future earnings or other conventional business/investment metrics.