Weekly Economic Snapshot: Rising Prices and Falling Confidence

Last week's economic data revealed strong economic growth running up against rising prices and falling confidence. The U.S. economy's real GDP rebounded sharply in the second quarter. However, PCE inflation reached its highest level in five months, while consumer confidence dipped for the first time in months. These conflicting trends played out in the markets, with the S&P 500 initially posting record highs before falling later in the week.

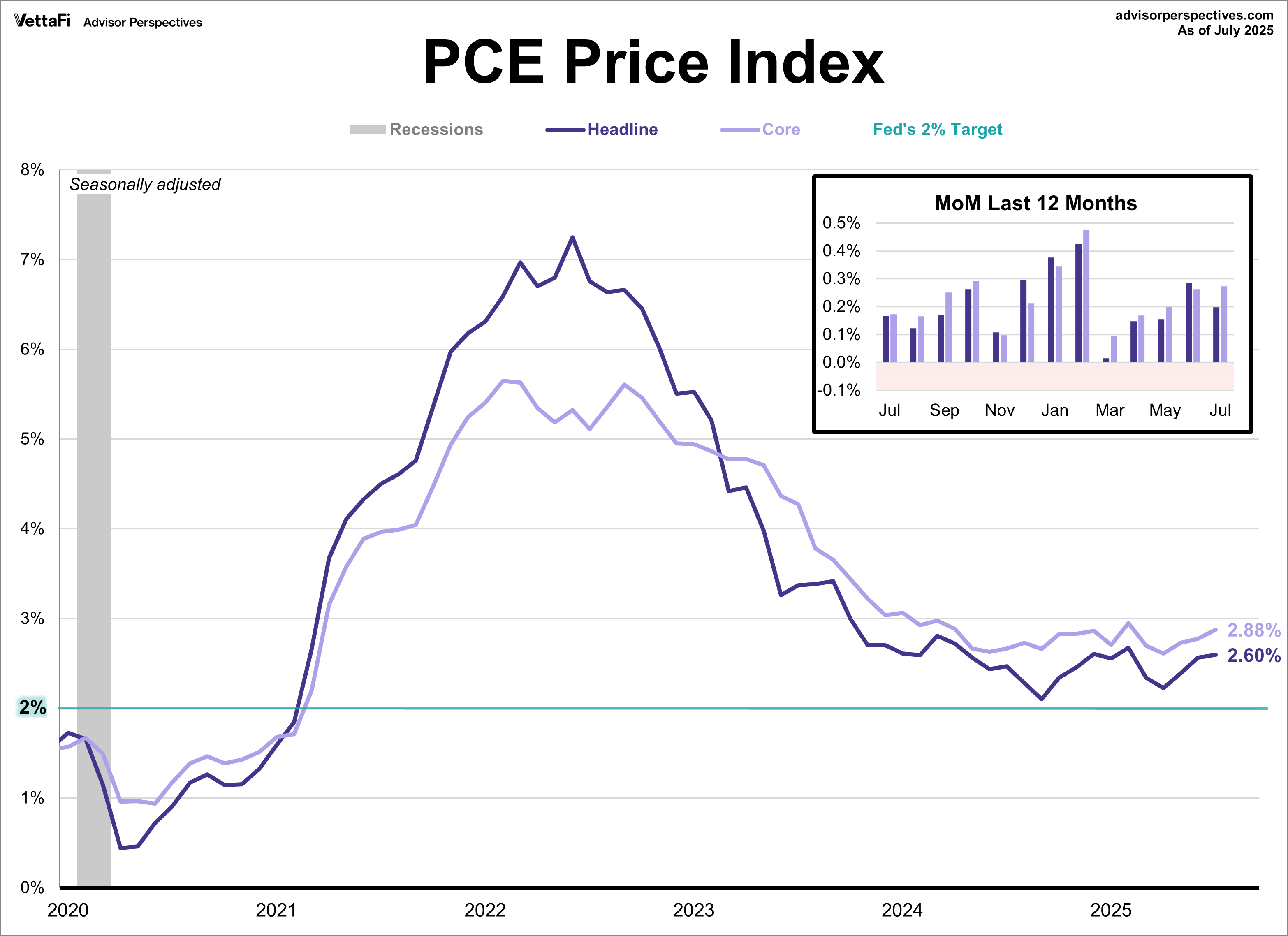

PCE Price Index

The Federal Reserve’s preferred inflation gauge reached its highest level in five months as it moved further away from the 2% target. The Core Personal Consumption Expenditures (PCE) Price Index, which excludes volatile food and energy costs, rose 2.9% year-over-year in July. This was consistent with the forecast but marked a slight pickup from June’s 2.8% reading. The headline index also hit a five-month high, rising 2.6%, as expected. On a monthly basis, both core and headline prices rose by 0.3%, as expected.

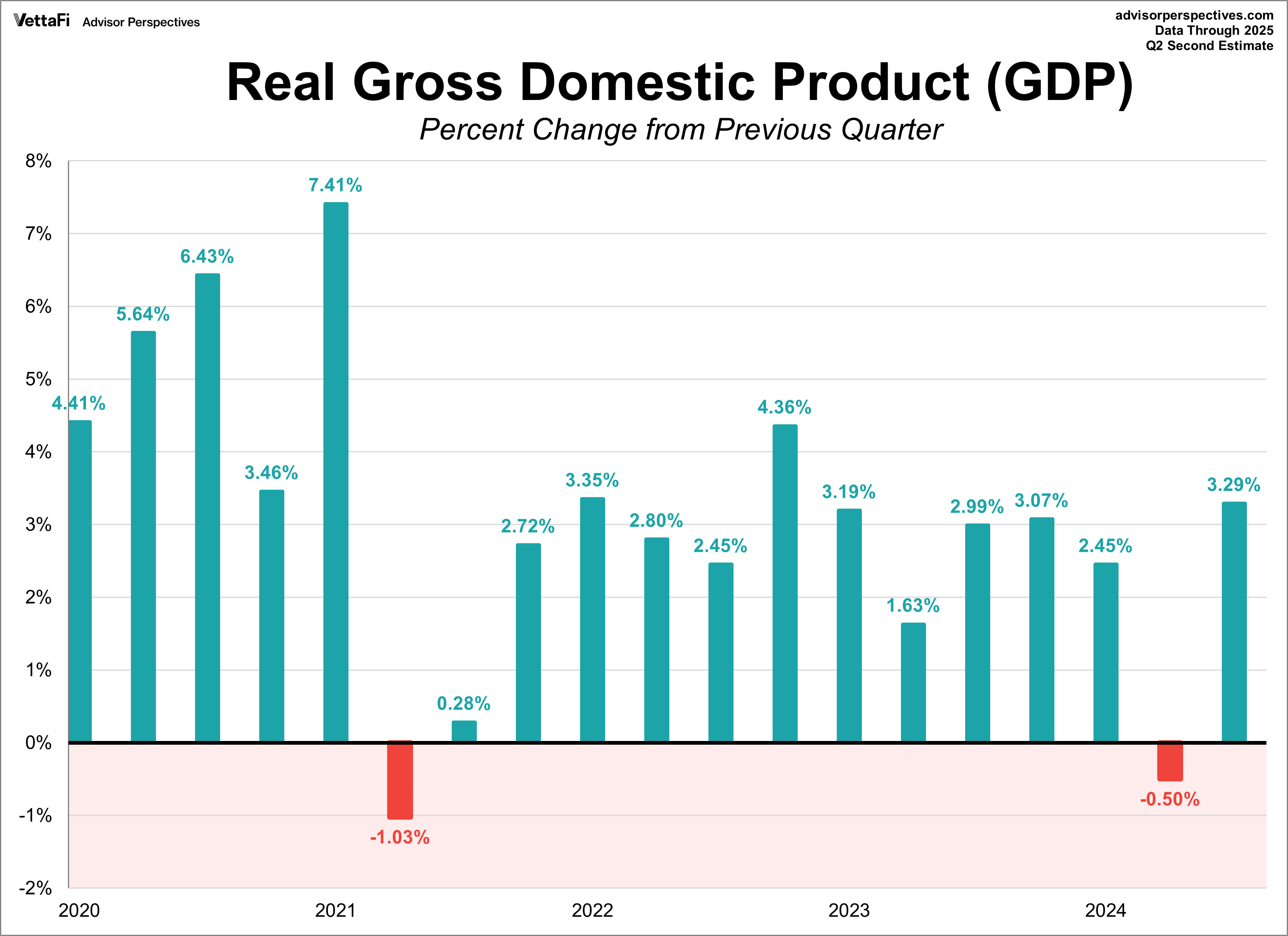

Gross Domestic Product (GDP)

According to the second estimate, the U.S. economy posted a strong rebound in the second quarter. Real GDP, the inflation-adjusted measure of all goods and services produced, increased at an annual rate of 3.3%. This marks a significant turnaround from the first quarter’s 0.5% contraction and surpassed the 3.0% forecast. The expansion was primarily driven by a decline in imports and an increase in consumer spending, although these gains were partially offset by a significant decline in business investment and a fall in exports.

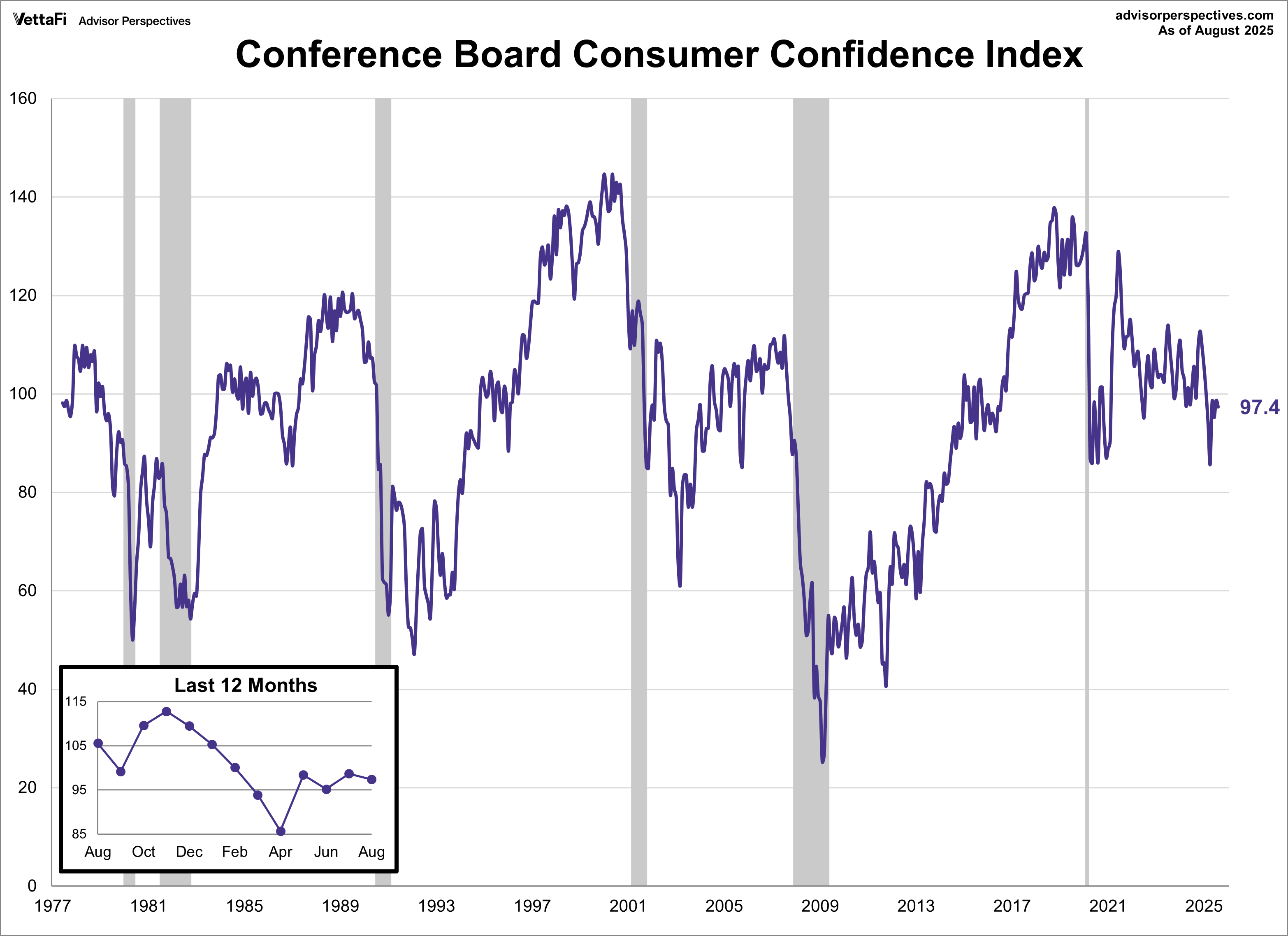

Conference Board Consumer Confidence Index

Consumer confidence dipped slightly in August, with the Conference Board Consumer Confidence Index® falling 1.3 points to 97.4. The latest reading was better than the forecast of 96.4. The index remains near a level seen over the past few months, suggesting a recent stabilization in consumer confidence, albeit at a subdued level.

The slight decline in consumer confidence was driven by weakness in both present and future conditions. On the present side, consumers' views on current job availability worsened for the eighth straight month, though this was somewhat offset by improved sentiment toward current business conditions. Looking ahead, while views on future business conditions improved, consumers were less optimistic about future job availability and income. The survey also highlighted that tariffs and inflation remain a key concern for consumers, with 12-month inflation expectations picking up for the first time in four months.

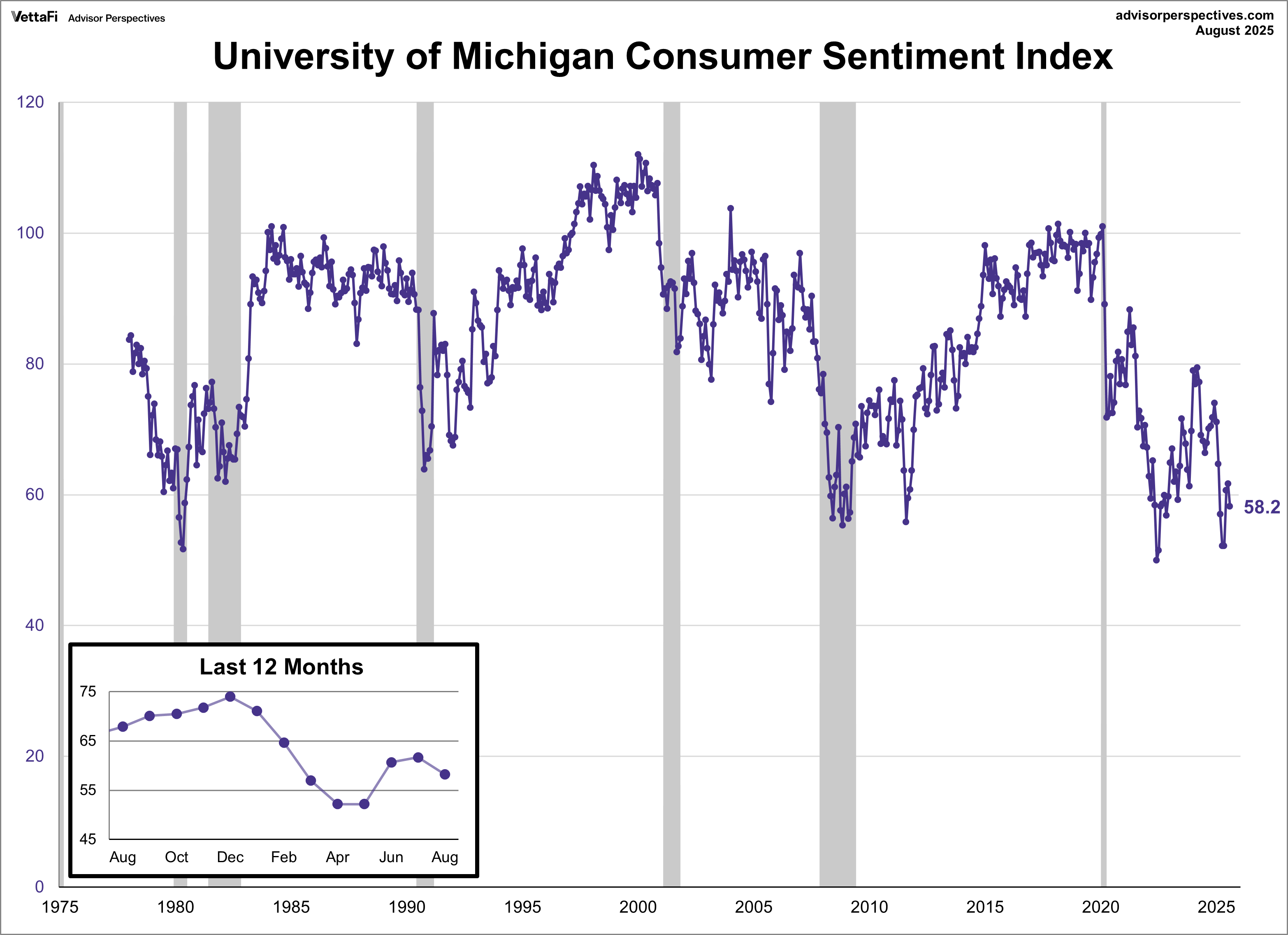

University of Michigan Consumer Sentiment Index

Consumer sentiment fell for the first time in four months, with the University of Michigan Consumer Sentiment Index falling nearly 6% to 58.2. The latest number was lower than the expected 58.6 reading.

The index’s deterioration this month was driven by worsening views across many aspects of the economy including buying conditions, personal finances, and future expectations for business conditions and the labor market. Additionally, inflation worries grew for both the near and long term. Year-ahead expectations increased from 4.5% to 4.8%, while the five-year outlook rose from 3.4% to 3.5%.

Market Reactions

The S&P 500 notched two new record highs last week but slid on Friday amid rising inflation worries. The index ultimately posted a loss of 0.1% for the week, ending its three week win streak. As a result, the SPDR S&P 500 ETF Trust (SPY) was flat compared to last week. Meanwhile, the S&P Equal Weight Index was down 0.5% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell 0.5%.

The 10-year Treasury yield finished the week at 4.23%, while the 2-year note finished at 3.59%.

The CME FedWatch Tool currently shows an 89% likelihood that the Fed will cut rates by 25 basis points at their meeting next month. Markets are pricing in another 25 basis point cut at the October meeting and four additional cuts in 2026.

Economic Data in the Week Ahead

Despite the shortened trading week, this week is packed with important economic updates, particularly concerning the labor market. All eyes will be on Friday's highly watched jobs report, but we'll get an earlier look at the labor market's health from JOLTS data, ADP's private payroll report, and weekly jobless claims. Additionally, S&P Global and the Institute for Supply Management will provide a glimpse into economic activity in the manufacturing and services sectors with the release of their August PMI readings.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.