The economic narrative last week was defined by a striking paradox. On one hand, the government shutdown has created a void in official data, leaving the Federal Reserve effectively "flying blind" as it gauges the health of the labor market and broader economy. On the other hand, the financial markets appeared entirely unfazed, with the S&P 500 shrugging off the uncertainty to post multiple record highs throughout the week.

In the absence of primary government indicators, policymakers and investors alike must turn to private sector releases to find clarity. These secondary reports, which include the latest figures on ADP employment, consumer confidence, and job openings (JOLTS), paint a picture of a cooling labor market and an increasingly cautious consumer.

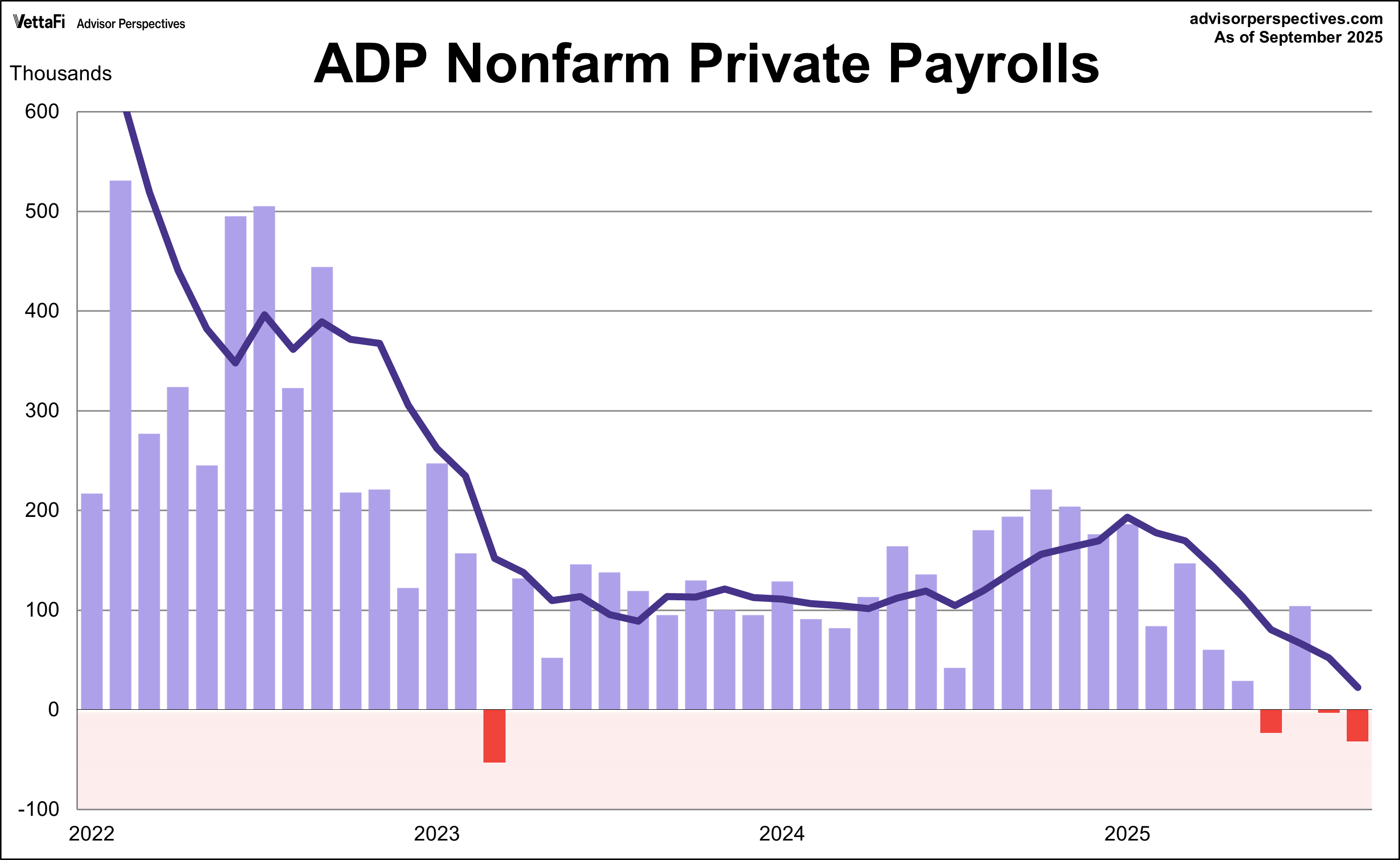

ADP Employment Report

Typically, the monthly jobs report from the Bureau of Labor Statistics (BLS) is the most anticipated economic news during the first week of a new month. However, because of the government shutdown, the September BLS report has been delayed, which shifts the spotlight to the ADP private employment report as the primary indicator for now.

The September ADP employment report continued to point to a softening labor market. According to the latest data, the private sector lost 32,000 jobs last month, following a loss of 3,000 in August. This marks the first time since the initial aftermath of the pandemic in 2020 that the private sector has experienced back-to-back months of job loss. The latest figure was also significantly lower than the expected addition of 52,000 jobs.

This slowdown was most notable in the leisure and hospitality sector, which lost 19,000 jobs and accounted for over 50% of the month’s total loss. Job losses were most apparent in small and mid-sized companies (those with fewer than 500 employees).

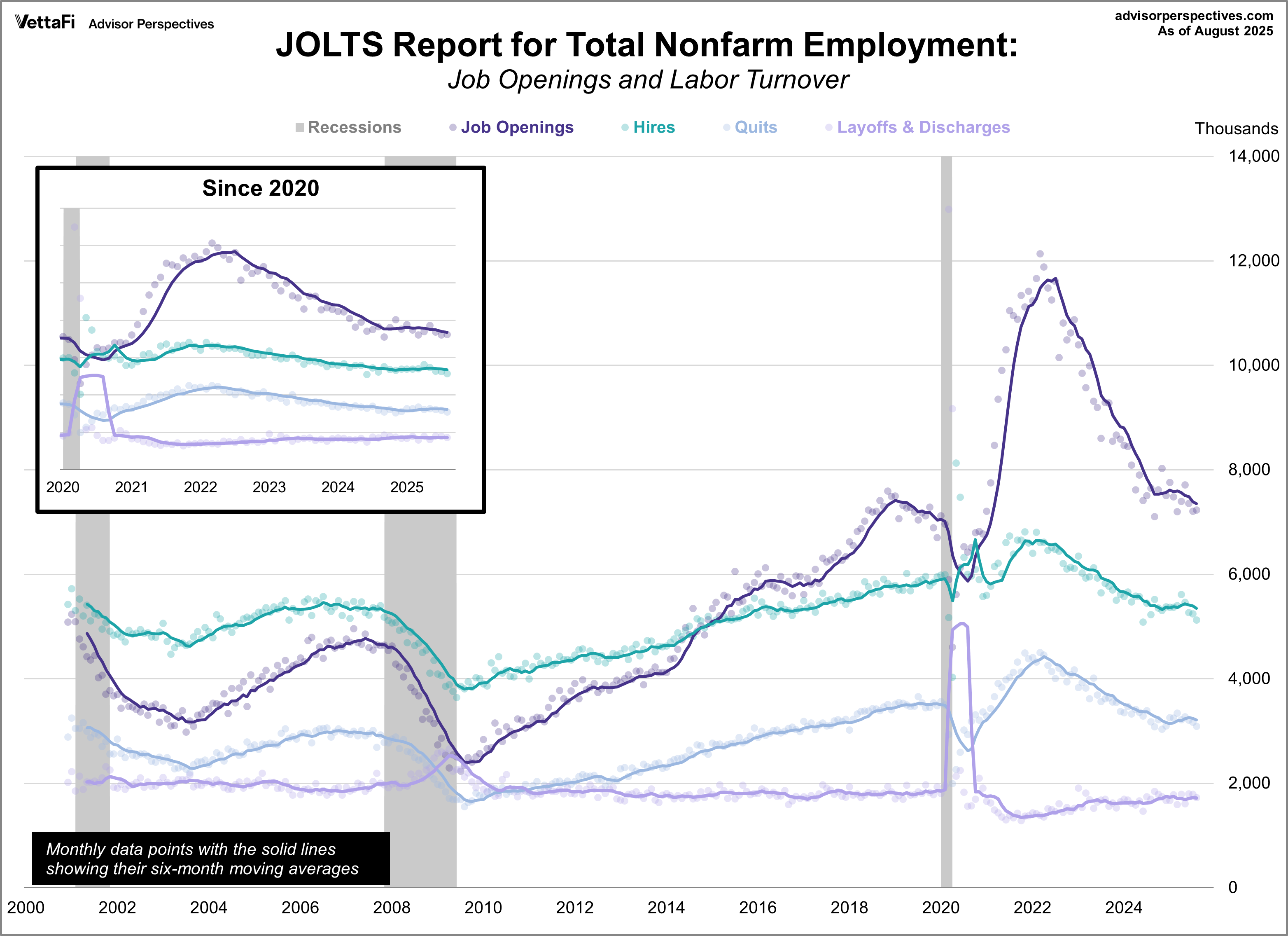

Job Openings and Labor Turnover Summary (JOLTS)

Job openings unexpectedly ticked up in August, rising for the first time in three months according to the latest JOLTS report. The number of openings rose by 19,000 to 7.227 million, coming in just above the expected 7.190 million.

Despite this modest increase, the job openings-to-unemployed-workers ratio remained below 1.0 for the second straight month. This signifies a shifting labor market where there are more unemployed people seeking work than there are available jobs, indicating a more challenging environment for job seekers.

Meanwhile, other significant labor market metrics, including the rates for hires, quits, and layoffs, continued their downward trends. The hire rate fell further, hitting its lowest level since April 2020. Similarly, the quits rate fell to its lowest level of the year, remaining well below pre-pandemic levels. Despite this broad slowing pace in hiring and movement, layoffs remain low, suggesting the "low hire, low fire" environment remains strong.

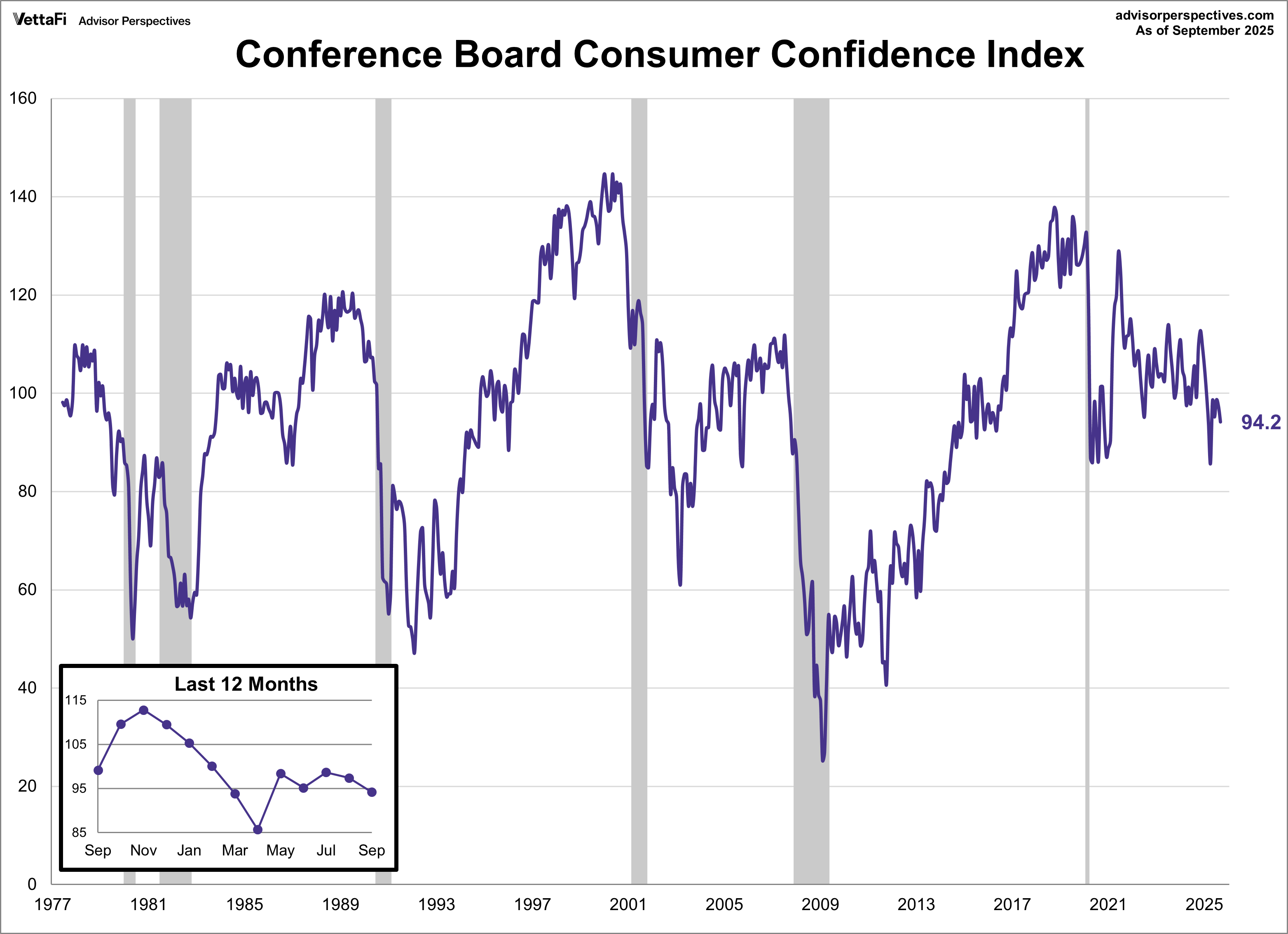

Conference Board Consumer Confidence Index

Consumer confidence fell for a second straight month in September, with the Conference Board Consumer Confidence Index® dropping 3.2 points to 94.2. This reading was below the forecast of 96.0 and marks the lowest level for the index since April.

This continued decline was driven by weakness in both present and future conditions. On the present side, consumers' views on current job availability worsened for the ninth straight month, hitting a multi-year low, and their assessments of business conditions were less positive than in recent months. Looking ahead (future conditions), consumers expressed pessimism about future job availability and business conditions, although this was somewhat offset by increased optimism about future income. Finally, the survey highlighted that inflation and higher prices were the main concerns influencing consumers' views, even as 12-month inflation expectations cooled slightly from 6.1% to 5.8%.

Market Reactions

The S&P 500 finished last week on a six-day win streak, notching three consecutive record highs to close out the week. The index ultimately posted a weekly gain of 1.1%. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 1.1% last week. Meanwhile, the S&P Equal Weight Index was up 1.4% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 1.4%.

The 10-year Treasury yield finished the week at 4.13%, while the 2-year note finished at 3.58%.

The CME FedWatch Tool currently shows a 95% likelihood that the Fed will cut rates by 25 basis points at their next meeting. Markets are also pricing in another 25 basis point cut at the December meeting and two additional cuts in 2026.

Economic Data in the Week Ahead

The economic calendar for the week ahead is relatively light, though it offers a few key indicators worth monitoring. We’ll get the latest trade balance figures for insight into the flow of goods and services, and ongoing weekly unemployment claims for a timely pulse of the labor market. The week will conclude with the University of Michigan’s preliminary report on consumer sentiment in October. Note that the September BLS employment report will be released once the government shutdown ends, likely within a few business days to a week.